According to ATO data, SMSFs are underweight offshore investments compared to their institutional counterparts and to the exposures recommended by traditional asset allocation models. With global stock markets up by around 18% over the last 12 months and trading near record highs, and the Aussie dollar establishing a very strong base around 75 US cents, many might believe that the boat has already sailed on offshore investment and it is prudent to keep the focus back in Australia. So, is it too late to invest offshore?

My answer to this question depends on your exposure and investment objectives, and is founded on the premise that “time in the market”, rather than “timing”, will work better for most investors. Hence, if you are a long-term investor and have no or limited offshore exposure, then “no”. Rather than broad market exposure, you might want to increase your exposure with a conviction style manager, who might be less impacted by a market downturn.

If you are positioned close to your recommended weight, or want to play it more from a trading perspective, I think you can afford to be patient and wait for better opportunities.

More on this later. First, let’s do a quick re-cap on the “why”, “where” and “how”.

Why invest offshore?

There are three very strong reasons to invest offshore. Firstly, the Australian market is small – less than 2% of global stock markets by capitalisation. This means that 98% of opportunities are outside Australia.

Secondly, our market is dominated by financial and resources stocks. The financials sector makes up 38.8% of the Australian market, compared to 14.4% in the USA. For materials, it is 15.7%, compared to 2.8%. Conversely, information technology stocks make up 22.1% of the US market, compared to a trifling 1.1% in Australia. Our market simply doesn’t have the Apples, Alphabets, Amazons, Microsofts or Facebooks, or in the healthcare sector, pharmaceutical giants like Pfizer, or industrial giants like General Electric.

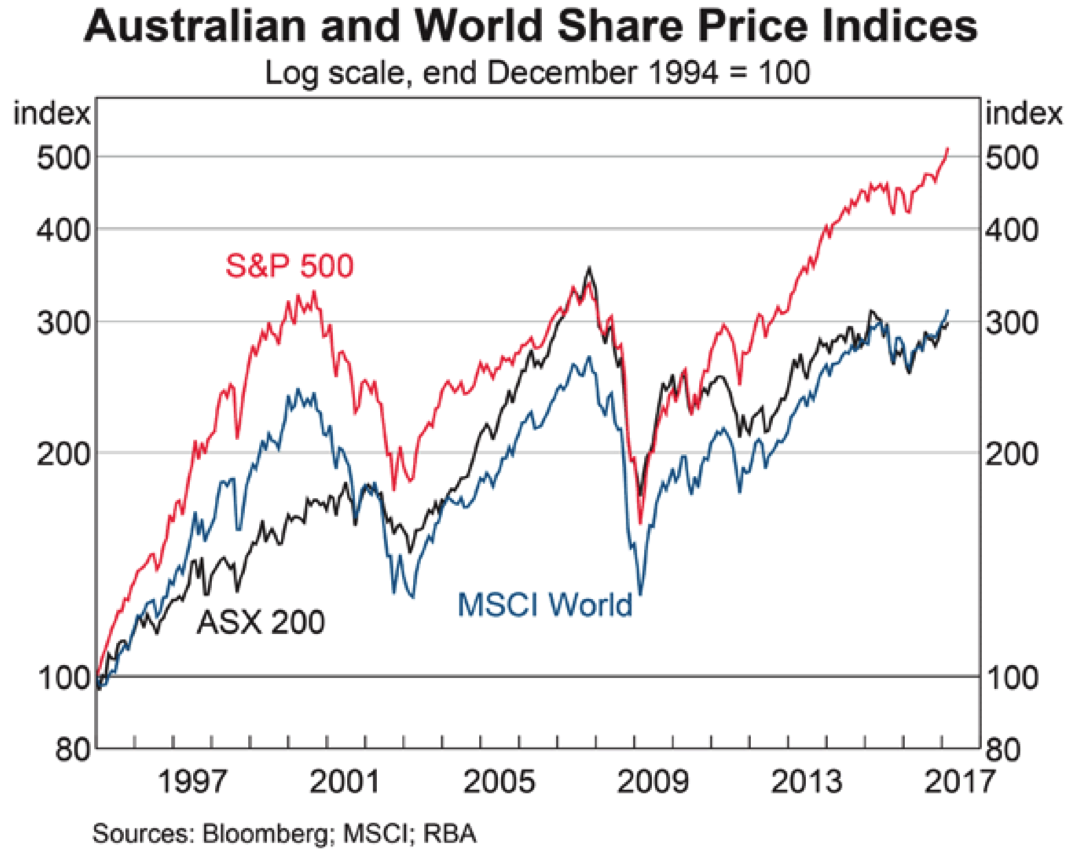

Thirdly, international share markets will often outperform the Australian market. While this can be true over any short-term period, it is also true over a longer period. The following graph from the RBA shows the Australian (black), US (red) and World (developed markets, blue) over a 22-year period, using a common base and logarithmic scale. Over this longer period, the US market has outperformed the Australian market.

Where to invest?

The MSCI ACWI Index, a leading global share index, captures almost 2,480 large and mid-cap stocks from 23 developed markets and 23 emerging markets. In this index, stocks from the USA account for 53% by market weight, with Japan coming in second at 7.6% and the UK third at 5.8%.

In a relative sense, emerging markets, such as India, Brazil or Thailand are very small. In aggregate, less than 11%.

Further, the US market is the lead market for most others. If the US market catches a cold, it is very hard for other markets to sustainably move in the other direction.

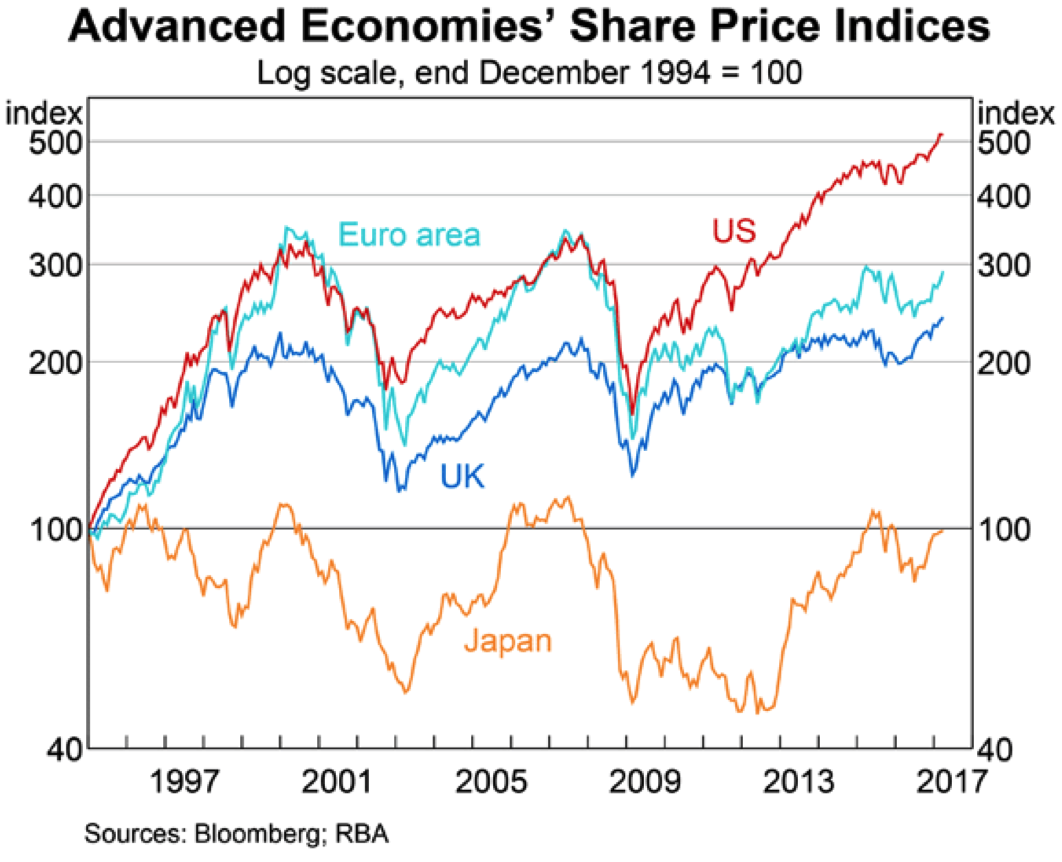

So, investing offshore for many investors is firstly about whether to invest in the USA or not. While you can just invest in emerging markets or Europe, it is higher risk not to have some exposure to the USA. Over the last 22 years, the US market has outperformed the other major markets, as the following graph from the RBA shows (US in red, Euro area light blue, UK dark blue and Japan brown).

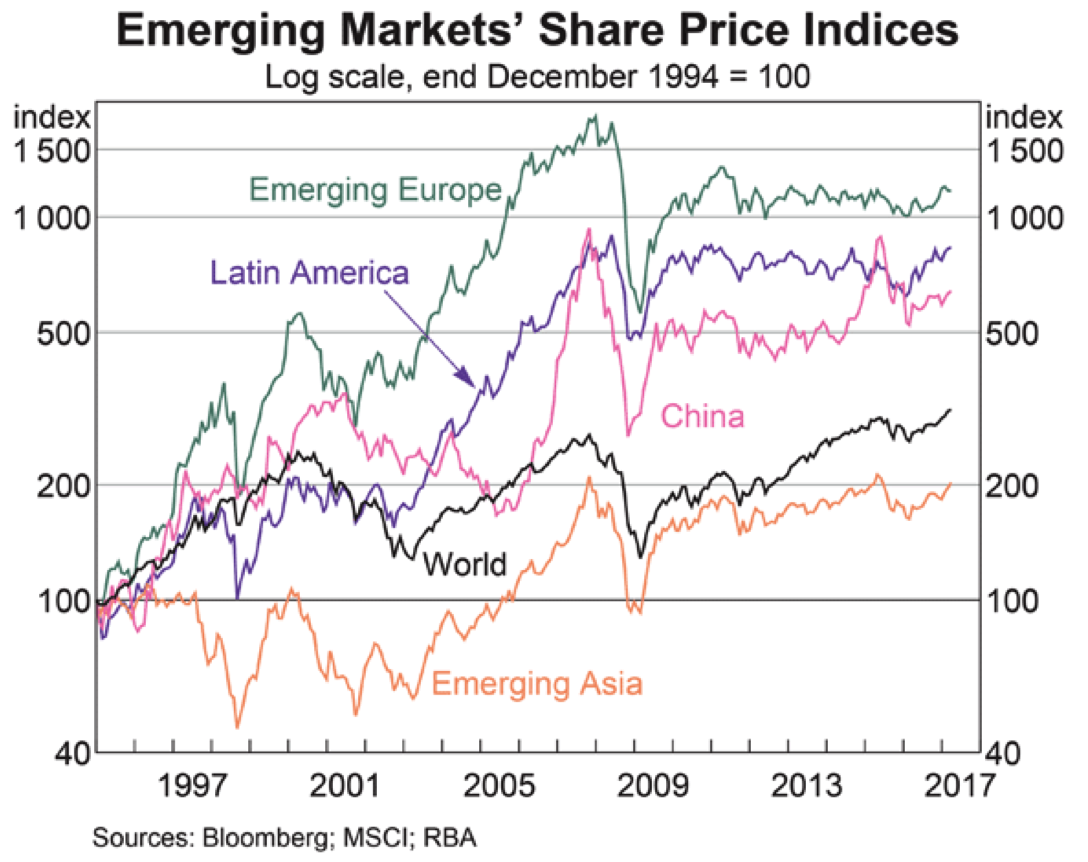

Since the GFC, the USA and most developed markets have outperformed emerging markets. The following graph shows the Developed World (in black), Emerging Europe (green), Latin America (blue), China (purple) and Emerging Asia (red).

More recently, the European markets have started to narrow the gap, as “quantitative easing European style” starts to take effect.

Source Bloomberg, to COB 7 April 17

With quantitative easing in Europe still going, an overweight position in Europe is probably still the way to go. However, you simply can’t ignore the USA.

With a stronger US dollar, emerging markets just won’t attract investor flows. So a position in both Europe and the USA is probably the call.

How do you do it?

Many of the major brokers (CommSec, E*Ttrade and nabtrade) provide facilities to invest directly in individual shares or other securities that trade on the major exchanges. You might, for example, be interested in the MAFIA stocks (Microsoft, Alphabet, Facebook, IBM & Amazon) that Charlie Aitken discussed a few weeks back (see here).

For the occasional offshore investor, nabtrade offers an excellent service. $19.95 brokerage on a trade between $5,000 and $20,000, with no custody fee, provided you do at least one trade annually. There is however a spread on the currency conversion, which applies to both buys and sells.

Many investors will probably prefer exposure through a broader based, managed investment. The question then becomes whether to have that managed passively or actively.

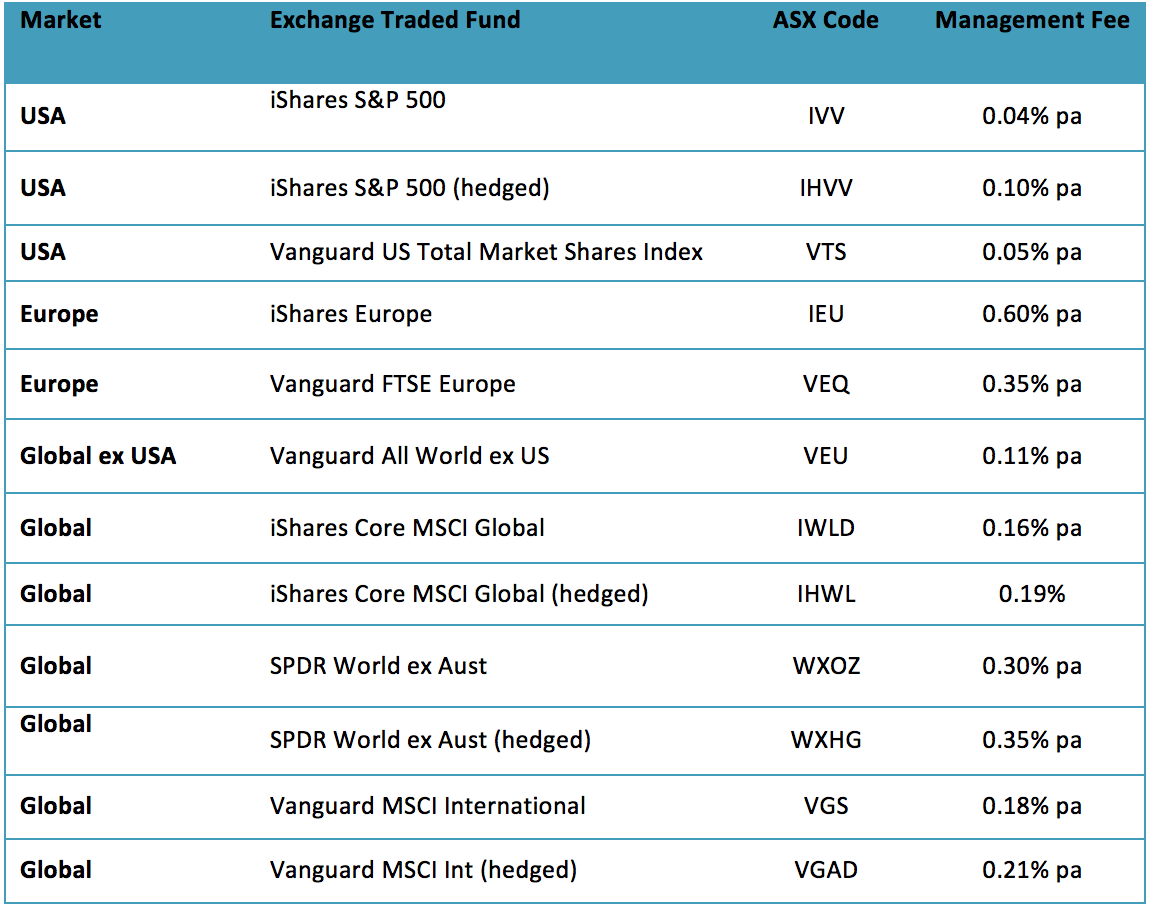

Exchange traded funds (ETFs) are passively managed investments designed to track a major index such as the S&P500. Traded on the ASX, ETFs generally have very low management fees because they are effectively on “auto-pilot”. Your return will be the same as how the index performs less the management fee – nothing more, nothing less.

These are the ETFs to use:

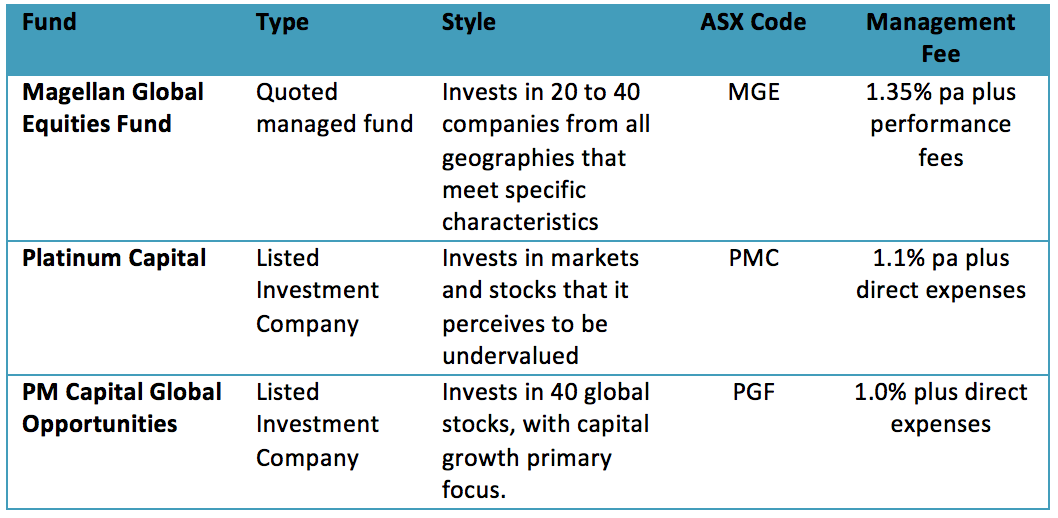

For an active manager, you may wish to consider some of the listed investment companies and ASX-quoted managed funds. Investment styles and areas of interest vary. These are the major funds to consider.

There are also a large number of global funds that are available on platforms, and in several cases, can be purchased on the ASX’s m-funds service through a broker. An example of a high conviction manager available on m-funds is the Peters MacGregor Global Fund, which uses a ‘bottom-up’ approach to develop a high conviction portfolio of 15 to 30 business listed around the world that it believes are trading at material discounts to assessed valuation. The management fee is 1.35% pa.

Hedged or unhedged?

One of the considerations about investing offshore is the direction of the Australian dollar.. Active managers will often prefer to manage the currency risk dynamically, hedging when they believe it is appropriate. Some active managers will hedge all exposures, while others will run an unhedged exposure.

Many ETFs now give investors the option of taking a hedged or unhedged currency exposure. For example, iShares IVV tracks the US S&P500 index and exposures are unhedged, while IHVV tracks the same index but exposures are hedged back into Australian dollars. The hedged version is typically a little more expensive.

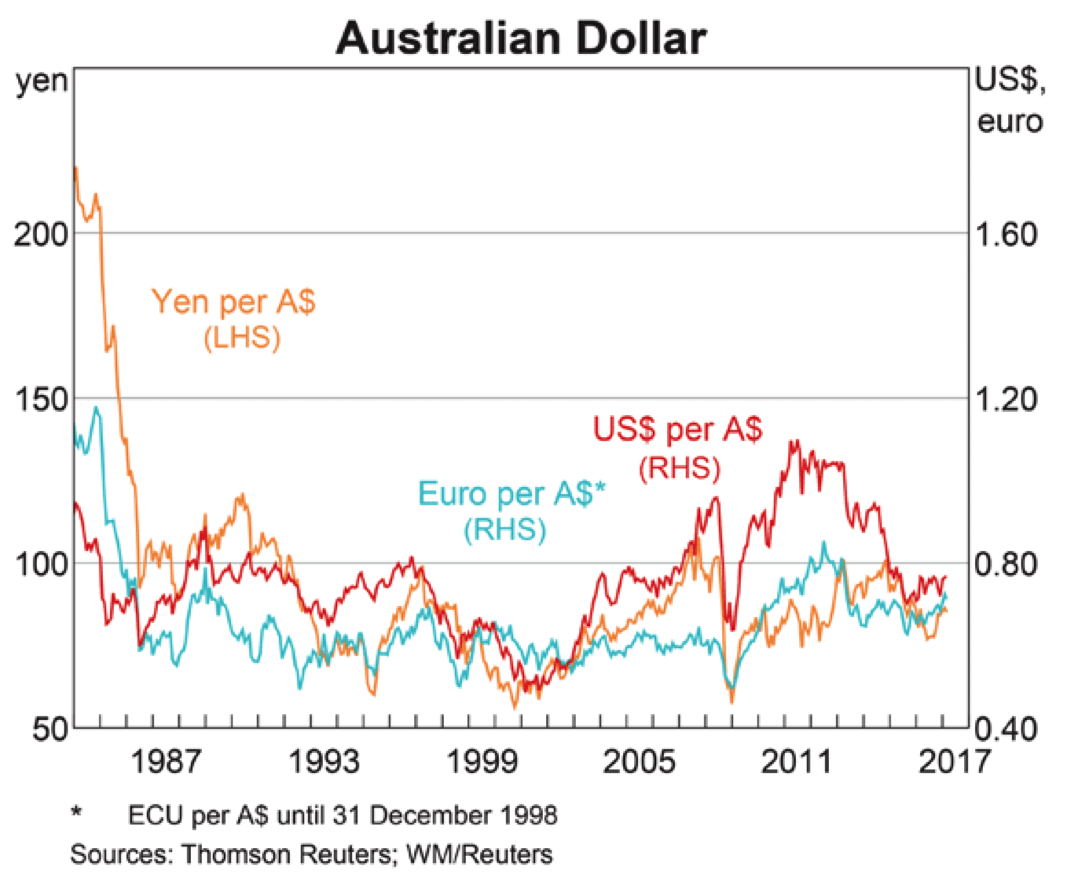

Where is the Australian dollar heading? Many commentators expect the Aussie to weaken in the medium term, feeling that a subdued economy, low interest rates and the end of the commodities boom will exert downward pressure. The RBA has also not hidden its view about our dollar being overvalued.

On a longer-term basis, the Aussie looks to be close to what many would consider to be fair value (around 0.75 US cents), but overvalued compared to the YEN and EURO. The following chart from the RBA provides a 32-year perspective (USD red, YEN brown, EURO blue).

While the Aussie dollar always looks vulnerable to a sudden downward move (historically, it goes down a lot harder than it goes up), it seems to have found a remarkable base of support in the low 70s. Like many economists, I’d like to see it in the 60s, but note that despite all the bearishness, it’s not going down. My 50/50 bet on the Aussie dollar is that we are more likely to be testing 80 cents rather than 70 cents before the year is out.

I think that the risk adverse call, given also the benefit of interest rate differentials, is that if you have the option to do so, invest on a currency hedged basis.

Is it too late?

And offshore markets? As Peter has discussed, we don’t see any immediate threat to the bull market continuing in 2017, although 2018 might be a more difficult proposition. And of course, that doesn’t mean that there won’t be a pullback, however there’s no reason, yet, to suggest that the trend has changed.

Bottom line – for a long-term investor with limited or no exposure to offshore markets, I don’t think it’s too late. If you’re already invested, perhaps wait for a bit of a pullback in both the equity and currency markets. Alternatively, look at manager(s) who offers a high conviction style approach to stock selection and, potentially, might be better placed to ride out any general market downturn.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.