Back in mid-February, bank dividends looked very secure. The Commonwealth Bank had emphatically confirmed that not only was it going to maintain its interim dividend of $2 per share, but it was prepared to maintain a dividend payout ratio above its target. CEO Matt Comyn said, when announcing the Bank’s half year profit, that “We are targeting a gradual return to our full year payout ratio range of 70% to 80%”. I wrote at the time words to the effect that “the biggest take to come out of the result is that CBA is going to do everything it can to maintain its full year dividend of $4.31 per share”.

Of the major banks, the only anticipated cut then was by Westpac, which would reduce its full year dividend to around $1.60 per share, in line with the ANZ and NAB.

How things have changed in the space of five weeks as the Coronavirus became the “black swan”.

It will impact bank earnings (and the ability to pay dividends in) three areas. Firstly, lower net interest margins following the Reserve Bank’s cut to the cash rate and lower lending rates to businesses. Secondly, the cost of customer support packages, which include the waiving of fees and other assistance measures. And thirdly, the big one and the hardest to estimate – an increase in bad debts as businesses (and households) struggle in the new environment. Offsetting these will be market share gains from the minor banks (although possibly no net volume increase), the Reserve Bank’s very accommodating 3 year fixed rate borrowing facility and higher treasury markets income.

Most brokers have cut their earnings forecasts for the major banks. Macquarie has downgraded FY20 earnings by between 2% and 10%, Citi between 0% and 7%, Credit Suisse by around 10% and Morgan Stanley between 10% and 18%. Target prices and dividend forecasts have also been reduced.

There are probably more downgrades to come, and decisions in other jurisdictions are adding to the pressure on dividends. Last Thursday, the European Central Bank asked Eurozone banks not to pay dividends or conduct share buybacks during the COVID-19 pandemic. It said: “to boost banks’ capacity to absorb losses and support lending to households, small businesses and corporates during the Coronavirus pandemic, they should not pay dividends for the financial years 2019 and 2020 until at least 1 October 2020”.

Australian banks are much better capitalized and considerably stronger than their European colleagues, so a similar directive is not expected from APRA. Among large listed commercial banks, CBA has the highest capital ratio on an internationally comparable basis, ANZ comes in third, Westpac in fifth and NAB is eleventh.

The table below shows the latest dividend forecasts from the brokers (source FN Arena):

Forecast Dividends – Broker Consensus Estimates

ANZ, NAB and Westpac are due to announce their March half year results in early May, and their interim dividends to be paid in June and July. This period will only have a couple months’ worth of “Coronavirus impact”, and it will be way too early to see any noticeable pick up in bad debts.

While bank boards traditionally aim to pay sustainable dividends (which also means minimizing changes from one period to the next), they will probably be conservative and go to the bottom (if not below the bottom) of their target payout ratios. These are shown in the table below.

Bank Dividend Payout Targets

Putting a number on this is almost impossible – but my hunch is that the interim dividends will more likely be in the sixties rather than the seventies that the brokers are currently forecasting.

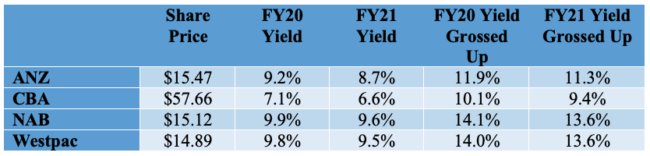

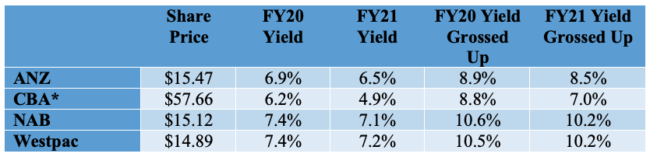

Yields

Let’s assume that the current broker consensus forecasts for dividends are the best guide (Scenario 1). Let’s take a second scenario and factor a further cut of 25% to the broker estimates for FY20 and FY21. The tables below show the forecast yields and the grossed up equivalents, which take into account the benefit of franking credits.(Note: ANZ is only 70% franked). The share prices are as per the close on Friday.

Scenario 1 – Implied Yields based on Current Broker Forecasts

Scenario 2 – Implied Yields based on further 25% cut to Broker Forecasts

* As CBA FY20 interim already paid, 25% cut only applied to implied FY20 final

On paper at least, these implied yields look attractive and income seekers who have sufficient cash should consider. The unknown question of course is the severity of the recession and its impact on bank bad debts.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.