I am getting genuinely concerned about the outlook for the Australian economy in the second half of this year.

It seems clear that Australian households are starting to tighten the purse strings. We have seen retail sales fall for three consecutive months, which has absolutely nothing to do with the pending arrival of Amazon in Australia.

What appears to be happening is the burden of record household mortgage debt, falling real wages, underemployment, and rising living costs are leaving households with little discretionary spending ability.

Then you add in peaking residential property prices, rising mortgage costs (switching from interest only loans), rising Medicare levy and falling Australian bank share prices, and you can understand why Australians seem to be hunkering down and saving instead of spending.

As I wrote last week, Australia simply has too much debt at the government and household level. This is at the low point of interest rates, where further interest rate cuts would simply be ineffective, like pushing on a string as such.

We have seen profit warning after profit warning in Australian retailers so far this year, which I think is a very concerning sign for the broader Australian economy and the domestic share market.

It’s pretty clear that Australian consumers are losing their “animal spirits” and I am starting to believe this is the start of a multi-year down cycle for Australian retailers and Australian shopping centre landlords. I stress this is BEFORE Amazing starts operating in Australia.

Interestingly, this may well be a global trend.

In recent months, US discretionary retailers have been smashed as have mall owners. Part of this is the Amazon effect in the US, but there appears also to be something much bigger going on here because the damage in US retailers and US mall owners is so widespread. Quite frankly bricks and mortar retailers are crumbling before our eyes.

Below is the Bloomberg US Shopping Centre Index, down -33%

Followed by the Bloomberg Regional Shopping Mall Index, down -40%

The large US retailer, Urban Outfitters, summarised the situation very well when delivering an earnings disappointment this week. “The sales shortfall in Q1 was wholly attributable to weaker than expected store channel performance in North America where all three brands encountered sluggish consumer traffic and sales. This issue is impacting virtually all US brick and mortar retailers. There are simply too many stores and too many malls in North America. We expect to see more closures and more brands disappear until a healthier balance is reached.”

Amazon chart..+35%

None of this is good news for ASX listed Westfield Group (WFD).

Fitch has projected a 9% year-end retail sector loan-default rate. Combined with Rue21, the expected forthcoming Chapter 11 petition from children’s retailer Gymboree would triple the 12-month trailing US institutional leverage loan retail default rate for May to 3%, from April’s 1%, thanks to the bankruptcy filing of shoe-store chain Payless.

No surprise then that U.S. Mall REITS continue to get hit hard, with big cap names Simpson Property, General Growth and Macerich hitting three-year lows in the U.S. overnight and extending the sell off to c40% from recent highs. Shorts have been building across the sector this year, as investors position for the fallout across the department store sector as a repercussion from the runaway success of the Amazon business model and the prospect of consumer spending habits changing forever.

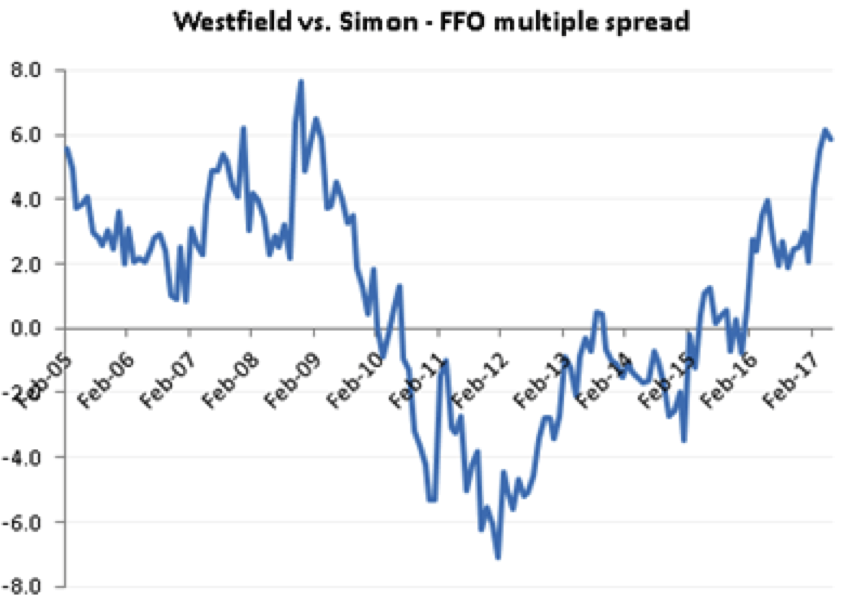

If the capitulation of the U.S. comps is not enough to pique your interest, then WFD’s valuation premium vs Simon Property at-or-near decade wides will almost stir the emotions, not to mention the sun setting on the great bond market bull run of our lifetime. WFD premium multiple (below) is purely a function of its Australian listing, and both generalist and REIT accounts crowded in stocks with US$ exposure. I am concerned WFD shares will de-rate further as Australian investors start to realise the problems US landlords have.

Around 75% of Westfield’s portfolio is in the United States. Relative to the US market, Westfield’s assets would be a very small percentage. They have about 20m square feet of higher quality “flagship” centres in the US, and one of their peers estimates there is about 500m square feet of that type of space (c. 4% share). Including the UK, the number is around US$725psf. Last year we estimated that the figure ex UK was $635psf. In terms of space, the biggest tenants are the big US department store operators, including Macy’s (18.7%) and JCPenney (7.2%).

The department stores often either own their own stores or pay very low rent, though, so the income contribution would be much smaller. WFD’s biggest tenant by income (not identified) contributes 3.0% of rent. The specialty retailers pay much higher rents psf, with the larger ones being Forever 21 (1.6% of space), H&M (1.3%) and The Gap (1.2%).

WFD trading on an FFO (P/E) multiple of 20x versus 14-17x for US peers and 15-18x for Australian retail REITs. US Mall Peers trade at ~25% discount to NAV vs WFD @ 17%

I am also concerned about “Westfield Australia”, or Scentre Group (SCG) as it’s now known.

An analyst report from Macquarie this week suggested that vacancy rates were rising in one of SCG’s premium Sydney assets, Westfield Bondi Junction.

To quote directly from the Macquarie research report:

- We completed a walk-through of SCG’s flagship Bondi Junction asset and were surprised at the extent of non-operational (i.e. hoarded up) tenancies.

- Our walk through highlighted a material ~21 hoarded up tenancies, or ~4% by number. The extent of remixing at this flagship asset is surprising.

- This leasing activity would no doubt be resulting in additional incentives, elevated downtime impacting the passing yield and potentially lower rent.

Remember, the mall owner model generally charges rent AND a percentage of retail sales. If vacancy rates are rising and retail sales falling, this is a nasty combination for earnings and potentially distributions to shareholders.

I believe what you’re seeing is US landlords coming to Australia. I think it’s time to be very cautious on the entire ASX listed retail landlord space. That includes WFD, SCG, GPT, SGP, VCX, etc.

There is genuine structural change happening in retailing, both globally and locally with a lag. The bricks & mortar model is under genuine structural pressure, and change is happening at a very rapid pace.

This is coming to Australia exactly at the time that Australians are reigning in their discretionary spending to pay for a rising cost of everyday living and rising debt servicing requirements.

The outlook for retailers and retail landlords looks negative to me for the next few years. I can’t see how this structural change reverses. Similarly, I can’t see Australian consumers regaining their “animal spirits” anytime soon.

I think this again reminds you of the DANGERS of passive investing. If you own the ASX200, you own all the retailers and retail landlords. That is and will continue to prove a bad decision.

The AIM Global High Conviction Fund, which I run, is long Amazon and JD.COM, yet we are running short positions in WFD, SCG, GPT and SGP on the theme above. We are also short Wesfarmers (WES), feeling they will not be immune to these structural sectorial pressures. I’ll write about my caution on Wesfarmers next week.

All in all, I want to reaffirm that I am getting increasingly bearish on the outlook for Australia. I told you last week the bank tax was a major mistake and banks have continued to fall. In fact, the falls are accelerating.

When bad policy meets a highly indebted nation and fast moving technological change, the results can negatively surprise in quick time.

The final point to remember is the retail sector is the biggest employer in Australia. The sector is going to shed more jobs and there’s no doubt in my mind the Australian unemployment rate is going to rise.

The question we all have to ask ourselves is has the ASX200 peaked for the year? I think it probably has and it’s time to be far more selective in your Australian investments.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.