This year’s August reporting season has been as much about falling share prices as it has been about financial performances. The persistent trend that sees stockbroking analysts issue far more rating upgrades than downgrades is causing the gap between Neutral ratings and Buy recommendations to consistently widen. Total Buy and equivalent ratings for the eight stockbrokers monitored daily by FNArena now stands at nearly 45% against 41.67% on Neutral, and still widening.

In the good books

AIR NEW ZEALAND LIMITED (AIZ) was upgraded to Neutral from Underperform by Credit Suisse. Buy/Hold/Sell: 3/1/0 Operating revenue exceeded forecasts but earnings were below Credit Suisse’s estimates, primarily because of higher maintenance expenses.

AMCOR LIMITED (AMC) was upgraded to Buy from Neutral by Citi and Upgrade to Outperform from Neutral by Credit Suisse. Buy/Hold/Sell: 4/3/0 Citi upgrades to Buy from Neutral, given the robust fundamentals with enhanced returns. Credit Suisse considers the stock undervalued and upgrades, given the share price has fallen 5.0% since early July.

APA GROUP (APA) was upgraded to Neutral from Underperform by Credit Suisse. Buy/Hold/Sell: 5/3/0 Credit Suisse upgrades to Neutral from Underperform ahead of the Northern Territory link approval, which is a significant positive catalyst.

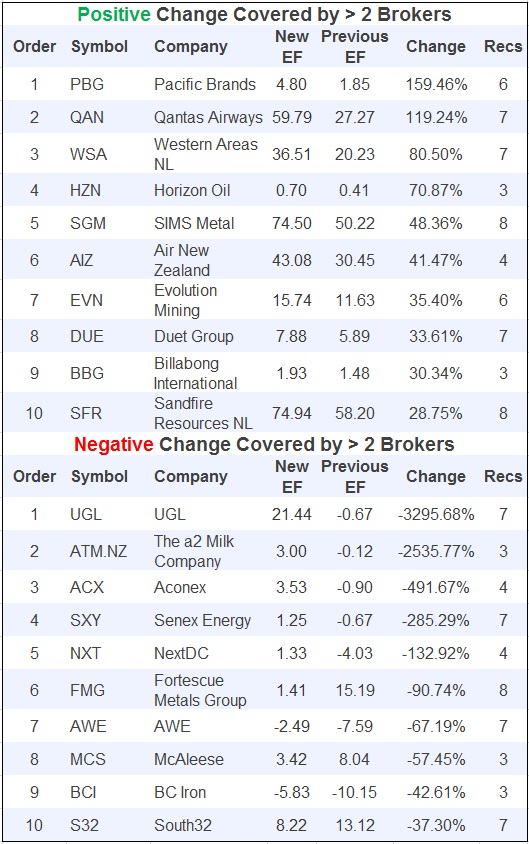

BC IRON LIMITED (BCI) was upgraded to Neutral from Sell by UBS and Upgrade to Outperform from Neutral by Macquarie. Buy/Hold/Sell: 1/2/0 UBS upgrades BC Iron to Neutral from Sell given recent share-price weakness and the potential of option value from the Koodaideri royalty. The potential to restructure the ownership of Iron Valley presents a positive catalyst, Macquarie believes, particularly if cash can be realised from the mine gate sales agreement.

DRILLSEARCH ENERGY LIMITED (DLS) was upgraded to Buy from Neutral by UBS. Buy/Hold/Sell: 3/3/0 Drillsearch’s FY15 result outpaced UBS’s forecast despite an 11% fall in production and 35% slump in revenue, as hedging gains and tax benefits conspired to lift earnings. UBS bumps up its near-term production outlook on the back of planned wet gas field connections.

FANTASTIC HOLDINGS LIMITED (FAN) was upgraded to Outperform from Neutral by Macquarie. Buy/Hold/Sell: 1/2/1 Fantastic’s second half built on a solid first half to provide a much better FY15 result, roughly in line with Macquarie’s forecast.

FLIGHT CENTRE LIMITED (FLT) was upgraded to Add from Hold by Morgans. Buy/Hold/Sell: 3/2/1 FY15 results and FY16 guidance were better than Morgans expected. Importantly the company is witnessing positive momentum in leisure travel.

HEALTHSCOPE LIMITED (HSO) was upgraded to Neutral from Sell by Citi. Buy/Hold/Sell: 3/4/0 Healthscope’s full-year result met Citi’s estimates and consensus. Margins outpaced expectations and Citi says the sale of the domestic pathology business for $105 million in July will remove a drag on margins going into FY16 and free up funds for expansion.

INSURANCE AUSTRALIA GROUP LIMITED (IAG) was upgraded to Neutral from Underperform by Macquarie. Buy/Hold/Sell: 0/7/1 The broker notes incorporating the lower margin Wesfarmers insurance business dragged down group margins, but believes acquisition synergies will kick in in FY16.

NINE ENTERTAINMENT CO. HOLDINGS LIMITED (NEC) was upgraded to Outperform from Neutral by Credit Suisse. Buy/Hold/Sell: 5/2/1 Credit Suisse says Nine’s earnings are starting to stabilise as monetisation of online viewing supports TV advertising, and given the supportive sport and news platforms. The broker upgrades believing the stock looks cheap on an earnings multiple of 5.9x and yield of 9%.

PACIFIC BRANDS LIMITED (PBG) was upgraded to Neutral from Underperform by Macquarie and to Overweight from Neutral by JP Morgan. Buy/Hold/Sell: 2/4/0 Pacific Brands’ result delivered on recently upgraded guidance, which had surprised Macquarie at the time. JP Morgan analysts believe a bottom has now been reached in terms of earnings before interest and taxes, EBIT. Despite ongoing challenges, the future should once again offer prospects for “growth”, in the analysts’ view.

PERPETUAL LIMITED (PPT) was upgraded to Buy from Neutral by UBS. Buy/Hold/Sell: 2/6/0 FY15 profit was ahead of UBS expectations. Net flows are in positive territory and wins on clients are delivering more meaningful funds growth.

RAMSAY HEALTH CARE LIMITED (RHC) was upgraded to Outperform from Neutral by Credit Suisse and to Outperform from Neutral by Macquarie. Buy/Hold/Sell: 4/2/2 Credit Suisse found Ramsay Health Care’s full-year result hard to fault as revenue grew, margins expanded and cost-outs mitigated pricing risk. Weakness in Ramsay’s French business had been weighing on Macquarie, given there seemed little respite ahead, and with Ramsay valuation is always an issue. But following an in-line result and management commentary, the broker has upgraded to Outperform.

SOUTHERN CROSS MEDIA GROUP (SXL) was upgraded to Neutral from Underperform by Credit Suisse. Buy/Hold/Sell: 2/4/2 The broker lifts earnings forecasts about 3% to 4% across FY16 and FY17 to reflect higher market shares in radio and TV.

TRANSFIELD SERVICES LIMITED (TSE) was upgraded to Outperform from Neutral by Credit Suisse and Upgrade to Buy from Neutral by Citi. Buy/Hold/Sell: 3/2/1 Transfield’s full-year result was in line with Credit Suisse at an operational level but net profit fell shy as depreciation, amortisation and interest took a toll. The broker believes valuation is compelling and upgrades to Outperform from Neutral. Although much depends on the immigration outcome, Citi believes the risk are being more than discounted, given the defensive nature of the company’s business.

UGL LIMITED (UGL) was upgraded to Neutral from Sell by UBS. Buy/Hold/Sell: 0/2/5 UGL’s profit fell short of consensus but earnings were in line with UBS’ forecast. The balance sheet is in a better position than feared but there remain risks around certain projects but UBS is attracted to UGL’s exposure to recurring maintenance work.

VIRTUS HEALTH LIMITED (VRT) was upgraded to Buy from Neutral by UBS. Buy/Hold/Sell: 3/1/0 FY15 results were in line and held few surprises for UBS after the June downgrade. The broker observes the company held its market share.

WESTFIELD CORPORATION (WFD) was upgraded to Buy from Neutral by UBS and Upgrade to Neutral from Sell by Citi. Buy/Hold/Sell: 2/3/2 First half cash flow was ahead of UBS estimates. Portfolio metrics continue to be attractive. Net property income was below expectations because of the timing of asset sales and FX. Citi maintains the company has a good business, with near-term headwinds and medium-term tailwinds, and the stock is now more attractively priced.

In the not-so-good books

BORAL LIMITED (BLD) was downgraded to Sell from Neutral by Citi. Buy/Hold/Sell: 3/4/1 FY15 fell short of Citi’s forecasts and the FY16 outlook is disappointing. The analysts suggest many things need to go right to maintain earnings at a steady rate.

NIB HOLDINGS LIMITED (NHF) was downgraded to Underperform from Neutral by Credit Suisse. Buy/Hold/Sell: 1/4/1 FY15 results were slightly below Credit Suisse’s forecasts. The broker had recently upgraded to Neutral on an expected recovery in the Australian resident health insurance business. This has occurred but other divisions are now expected to be a drag on earnings in the near term.

Webjet Limited (WEB) was downgraded to Neutral from Outperform by Credit Suisse. Buy/Hold/Sell: 2/3/0 The FY15 result was largely pre-released and the main focus is on transaction value. Year to date growth is positive and Credit Suisse is pleased with the core business. With the stock trading close to a market multiple and limited near-term catalysts the broker downgrades to Neutral from Outperform.

Earnings Forecast

FNArena tabulates the views of eight major Australian and international stock brokers: BA-Merrill Lynch, CIMB, Citi, Credit Suisse, Deutsche Bank, JP Morgan, Macquarie and UBS.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.