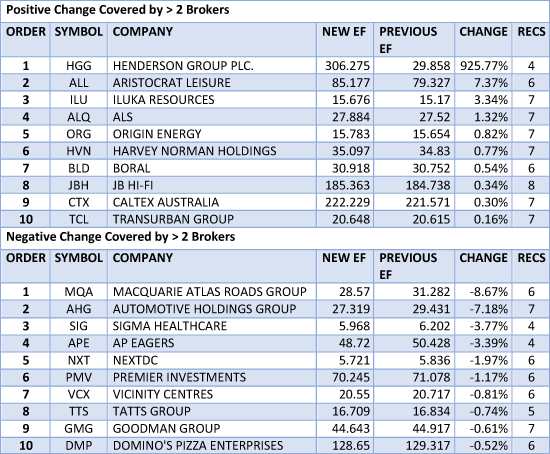

The chart below shows the buy recommendations of brokers. Companies are only displayed in this table if at least 5 of the above mentioned brokers have a current position on the stock. A broker sentiment value of +1 means all brokers have a buy recommendation. The target price upside/downside is relative to the price at the time the table was updated.

The stocks with the largest target price upside this week are HT&E with 35.44% and Super Retail Group with 33.1%.

[table “281” not found /]

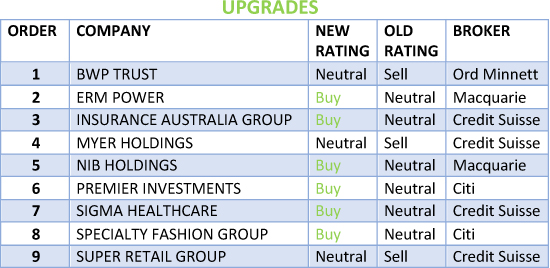

In the good books

ERM POWER LIMITED (EPW) Upgrade to Outperform from Neutral by Macquarie B/H/S: 2/1/0

Macquarie suggests the option the company acquired by purchasing the penalty REC will pay off, with the recent collapse in the Cal 19 REC price.

In the last 18 months the broker notes 15.4TWh of renewable commitments have been made and, while it does not appear these have exceeded the REC target yet, with development times of solar dropping to 12 months and construction costs falling, the signal is to build renewables with limited REC support.

Macquarie upgrades FY20 earnings estimates to reflect the one-off benefit associated with falling REC forward prices. The broker upgrades to Outperform from Neutral and raises the target to $1.30 from $1.24.

PREMIER INVESTMENTS LIMITED (PMV) Upgrade to Buy from Neutral by Citi B/H/S: 5/1/0

Citi believes investors are too bearish, arguing the current weakness in sales is transitory. The analysts do acknowledge there is downside to market consensus forecasts. Citi’s advice to investors is: pick your moment.

Upgrade to Buy from Neutral. While the analysts also believe market concerns around discounting are being overplayed, their new target of $13.80 compares with $15.10 previously.

SPECIALTY FASHION GROUP LIMITED (SFH) Upgrade to Buy from Neutral by Citi B/H/S: 1/0/0

Citi believes investors are too bearish, arguing the current weakness in sales is transitory. The analysts do acknowledge there is downside to market consensus forecasts. Citi’s advice to investors is: pick your moment.

Upgrade to Buy/High Risk from Neutral. While the analysts also believe market concerns around discounting are being overplayed, their new target of $0.55 compares with $0.70 previously.

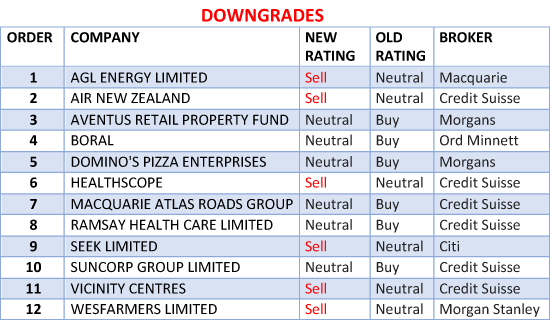

In the not-so-good books

AGL ENERGY LIMITED (AGL) Downgrade to Underperform from Neutral by Macquarie B/H/S: 2/3/2

Macquarie observes renewable investment continues to ramp up strongly. The stock is an attractive business but the fundamental commodity, electricity, appears to have peaked and incremental additions like the REC pricing are unwinding limited wholesale growth.

While the broker believes there is still a mild upgrade cycle for the company’s earnings in the near term, technology threats continue to challenge the structure of the market and core volume growth. Rating is downgraded to Underperform from Neutral. Target is reduced to $24.30 from $25.00.

AIR NEW ZEALAND LIMITED (AIZ) Downgrade to Underperform from Neutral by Credit Suisse B/H/S: 0/3/1

The airline has updated FY17 guidance for earnings to likely exceed NZ$525m. The increase is attributed to better-than-expected revenue from what was observed at the first half and lower-than-forecast fuel costs.

As a result of changes to forecasts, Credit Suisse increases its target to NZ$2.50 from NZ$2.10. Reflecting the updated valuation in the current share price the rating is downgraded to Underperform from Neutral.

AVENTUS RETAIL PROPERTY FUND (AVN) Downgrade to Hold from Add by Morgans B/H/S: 0/2/0

The company has announced the acquisition of two assets for $436m, to be funded via a $215m entitlement issue at $2.32 per security plus $250m in debt.

The company expects to pay a fourth quarter distribution of around 4c, bringing the total FY17 distribution to around 15.9c.

Morgans believes the company is well placed to navigate challenges in the broader retail sector and adjusts forecasts for the capital raising and acquisitions as well as updating on preliminary revaluations on the existing portfolio.

Rating is downgraded to Hold from Add. Target is reduced to $2.45 from $2.53.

BORAL LIMITED (BLD) Downgrade to Hold from Accumulate by Ord Minnett B/H/S: 4/2/0

Ord Minnett envisages the company entering a period of robust earnings growth, underpinned by the consolidation of the acquisition of US-based Headwaters and the realisation of synergies from Meridian Bricks and the USG joint venture.

Nevertheless, the broker believes the growth profile is now factored into the share price. Rating is downgraded to Hold from Accumulate. Target is raised to $6.65 from $6.50.

VICINITY CENTRES (VCX) Downgrade to Underperform from Neutral by Credit Suisse B/H/S: 2/2/2

A new analyst assumes coverage of the stock and, having undertaken a thorough assessment of the company’s regional and sub- regional assets, includes a more subdued view on the long-term viability and downside risks of the tier 3 centres.

The broker no longer envisages valuation support for the stock at current levels and downgrades to Underperform from Neutral. Target is reduced to $2.65 from $3.03.

WESFARMERS LIMITED (WES) Downgrade to Underweight from Equal-weight by Morgan Stanley B/H/S: 1/4/3

Morgan Stanley believes the market is misconstruing the impact of Amazon’s entry into Australia by selling category killers rather than conglomerate Wesfarmers.

The broker suspects that as Amazon rolls out its 1P business in Australia, especially apparel – a huge success in the US, earnings from Kmart will fall considerably. Bunnings should be relatively insulated, in the broker’s opinion, while Kmart and Target are vulnerable.

The broker reduces valuations for the latter two and downgrades to Underweight from Equal-weight. Target is reduced to $36 from $41. Industry view is moved to Cautious from In-line

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.