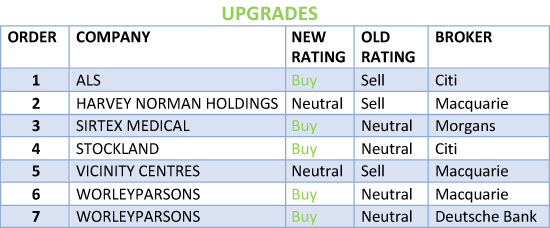

In the good books

STOCKLAND (SGP) Upgrade to Buy from Neutral by Citi B/H/S: 2/3/1

Citi suggests Stockland is benefitting from a favourable residential mix shift which is enabling earnings to grow while land sales moderate. The broker believes retail net operating income growth could exceed current expectations.

Valuation looks attractive on a 5.5% yield and modest PE, Citi suggests. Upgrade to Buy. Target rises to $5.08 from $4.91.

SIRTEX MEDICAL LIMITED (SRX) Upgrade to Add from Hold by Morgans B/H/S: 4/0/0

Two recent trials have both failed to show a survival advantage in primary liver and colon cancer, Morgans notes. The broker is not surprised, citing poor study designs and prior failed studies, although the lack of utility in liver-only colon cancer patients is disappointing and relegates the therapy to salvage.

Nevertheless, Morgans believes the core business is viable and unlikely to be detrimentally affected by these results. The broker lowers FY18-19 dose sales expectations and reduces the target to $13.63 from $15.60.

With more than 10% upside envisaged to the target, the rating is upgraded to Add from Hold.

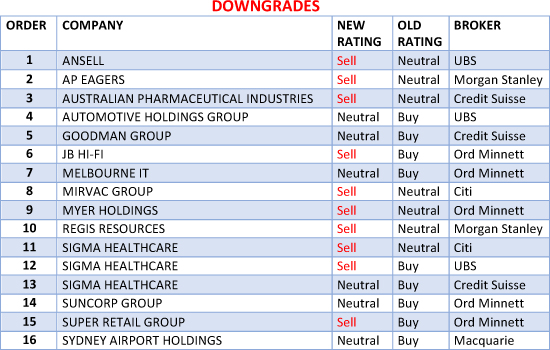

In the not-so-good books

AUTOMOTIVE HOLDINGS GROUP LIMITED (AHG) Downgrade to Neutral from Buy by UBS B/H/S: 4/2/1

The company has downgraded FY17 net profit guidance to a range of $87-89m, down -8.4-10.5% versus FY16. The company has also flagged -$35m in restructuring costs, which will be taken below the line. The refrigerated logistics division is expected to report a materially improved second half.

The weaker performance is driven by continued weak new car sales in Western Australia and a softening on the east coast, UBS observes. The broker believes, given an apparent plateauing of house prices and subsequent wealth effect, there is a risk that the weaker household cash flow that is forecast will impact on new car sales data in FY18.

Rating is downgraded to Neutral from Buy. Target is reduced to $3.05 from $4.95.

ANSELL LIMITED (ANN) Downgrade to Sell from Neutral by UBS B/H/S: 0/4/2

The company will sell its sexual wellness business for US$600m. This has been the fastest growth asset for the company, UBS observes. On a three-year outlook, the broker estimates the continuing business will grow operating earnings at 2% to 4%.

The broker believes valuation is not supporting the current stock price and downgrades to Sell from Neutral. The company will commence a buyback on market for up to 10% of issued stock.

The broker suspects the growth outlook may improve with industrial recovery. The company continues to examine acquisitions but has conceded there is a lack of opportunities that satisfy its valuation metrics. Target is raised to $24 from $22.

AUSTRALIAN PHARMACEUTICAL INDUSTRIES (API) Downgrade to Underperform from Neutral by Credit Suisse B/H/S: 0/0/2

Following Sigma’s (SIG) trading update, Credit Suisse revises assumptions for earnings for Australian Pharmaceutical industries.

Credit Suisse lowers revenue growth assumptions for the company’s retail division and this results in earnings downgrades of -3% to 5% over the forecast period.

Target is reduced to $1.90 from $2.05 and the rating is downgraded to Underperform from Neutral. A slower shopfront trading environment and a more competitive wholesaling dynamic suggests the sector will be challenged over the short to medium term.

JB HI-FI LIMITED (JBH) Downgrade to Lighten from Accumulate by Ord Minnett B/H/S: 2/3/2

Ord Minnett believes the outlook for the Australian consumer discretionary business is deteriorating and the pending entry of Amazon into the local market is a negative for multiples and forecasts for earnings per share.

JB Hi-Fi’s rating is downgraded to Lighten from Accumulate. Target is reduced to $20.50 from $32.00.

MELBOURNE IT LIMITED (MLB) Downgrade to Hold from Buy by Ord Minnett B/H/S: 0/1/0

The company has now completed the acquisition of WME and the associated capital raising. Nevertheless, given a strong recent share performance Ord Minnett is downgrading to Hold from Buy. Target is $2.59.

Management expects 12% to 18% accretion for earnings in 2017 on an underlying basis, which assumes WME is owned for a full year. The company has updated FY17 guidance to $37.5-41.5m.

MYER HOLDINGS LIMITED (MYR) Downgrade to Lighten from Hold by Ord Minnett B/H/S: 1/4/1

Ord Minnett believes the outlook for the Australian consumer discretionary business is deteriorating and the pending entry of Amazon into the local market is a negative for multiples and forecasts for earnings per share.

Myer’s rating is downgraded to Lighten from Hold and the target cut to $0.80 from $1.15.

SIGMA HEALTHCARE LIMITED (SIG) Downgrade to Sell from Neutral by Citi B/H/S: 0/1/3

Yesterday, in a first response post bad news announcement from the company, Citi analysts had elected not to make any changes to their $1.20 price target, forecasts or Neutral rating. This has all changed 24 hours later. Citi has downgraded to Sell.

Behind the downgrade hides a significant change in view and that is now that Sigma is likely to lose its major customer Chemist Warehouse (CW) once the current agreement expires in 2019.

This, the analysts explain, will translate in the loss of 33% of revenues in H2 FY20. Target price tumbles to 65c from $1.20. Estimates have been culled.

SUPER RETAIL GROUP LIMITED (SUL) Downgrade to Lighten from Accumulate by Ord Minnett B/H/S: 6/0/1

Ord Minnett believes the outlook for the Australian consumer discretionary business is deteriorating and the pending entry of Amazon into the local market is a negative for multiples and forecasts for earnings per share.

The risks include a heavily indebted consumer, rising energy prices and low wages growth. The broker remains downbeat on the retail sector and very downbeat on retail inflation.

Super Retail’s recommendation is downgraded to Lighten from Accumulate and the target to $7.25 from $11.50.

SUNCORP GROUP LIMITED (SUN) Downgrade to Hold from Accumulate by Ord Minnett B/H/S: 3/4/1

The latest disclosures on the company’s banking arm show weak lending growth in retail in the March quarter, although Ord Minnett observes this was offset by very low loan losses and a strong capital position.

The broker remains cautious about the stock and the potential divergence in general insurance margin trends between Suncorp and Insurance Australia Group (IAG). The fact that the stock is also trading around the broker’s steady target price of $14.11 leads to a lowering of the recommendation to Hold from Accumulate.

SYDNEY AIRPORT HOLDINGS LIMITED (SYD) Downgrade to Neutral from Outperform by Macquarie B/H/S: 1/5/1

The company has reported traffic for April, with the boost from Easter clearly evident in the numbers as international was up 12.1% and domestic up 0.7%.

The fundamentals remain robust, in Macquarie’s view, as the near-term traffic growth outlook is strong. Nevertheless, the broker believes value is already captured in the current share price.

Rating is downgraded to Neutral from Outperform. Target is $7.15.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.