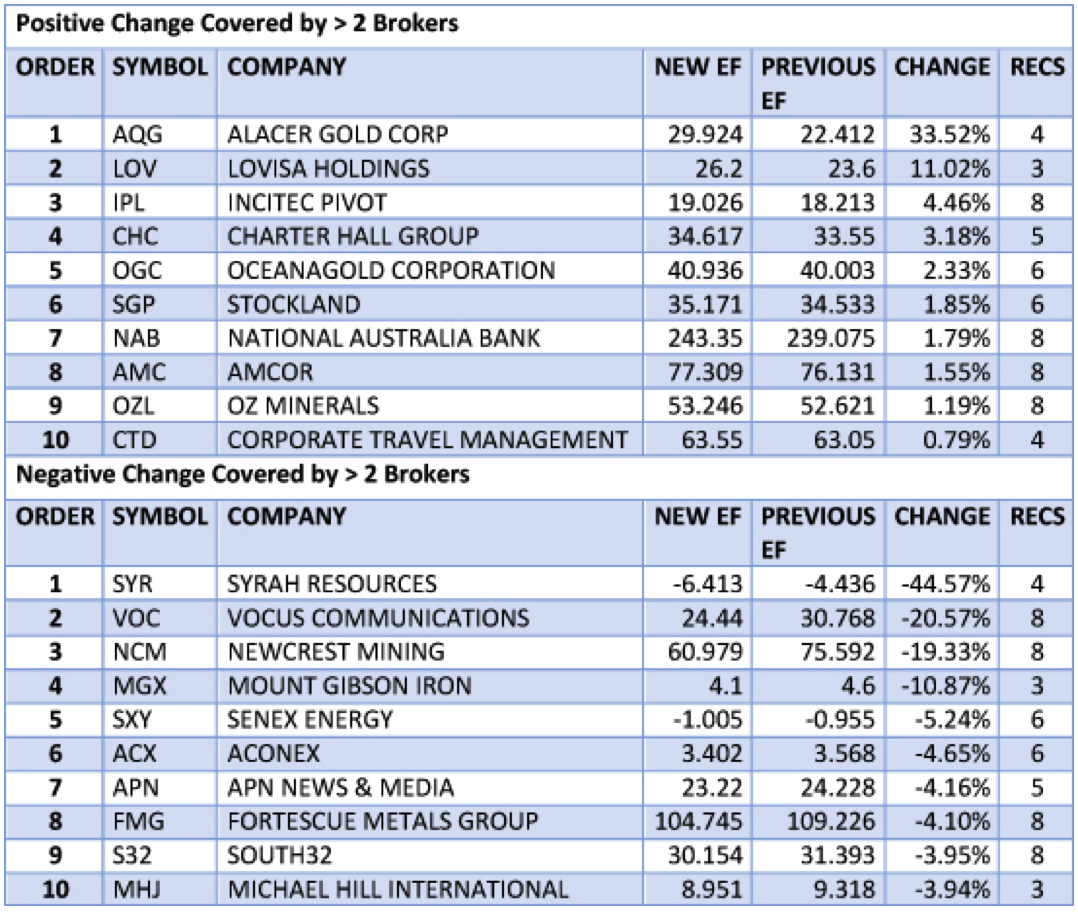

The chart below shows the buy recommendations of brokers. Companies are only displayed in this table if at least 5 of the above mentioned brokers have a current position on the stock. A broker sentiment value of +1 means all brokers have a buy recommendation. The target price upside/downside is relative to the price at the time the table was updated.

The stocks with the largest target price upside this week are Alacer Gold with 111.91% and Far Limited with 97.53%.

[table “276” not found /]

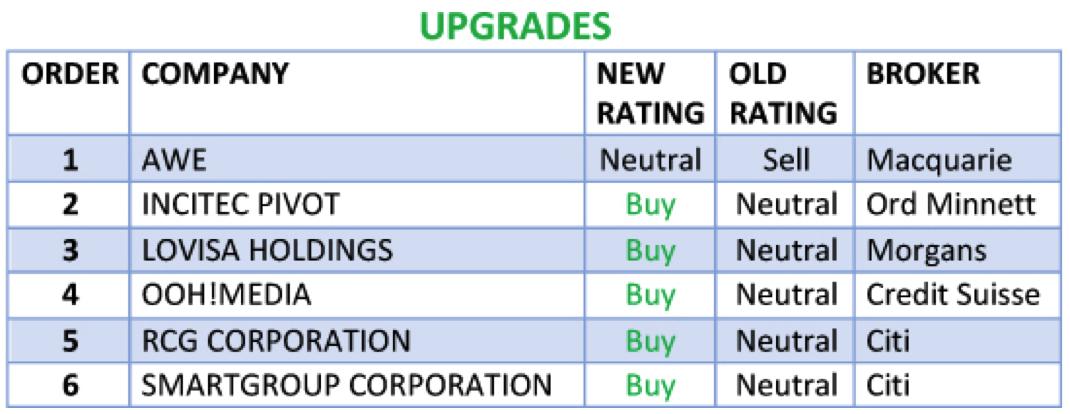

In the good books

LOVISA HOLDINGS LIMITED (LOV) Upgrade to Add from Hold by Morgans B/H/S: 2/1/0

The company has reported March quarter like-for-like sales growth of 6.7% and same-store sales growth of 10.9% in the year to date.

The company has also acquired Klines South Africa, which comprises 17 store locations. Morgans believes the stock is reasonable value at current levels and upgrades to Add from Hold. Target is raised to $4.48 from $4.37.

The broker believes the company’s low basket size and solid execution has buffered it against softer retail conditions. Further international expansion may provide more upside too.

OOH!MEDIA LIMITED (OML) Upgrade to Outperform from Neutral by Credit Suisse B/H/S: 2/0/0

The company’s overweight exposure to road and retail has served it well, in Credit Suisse’s view. The ACCC has formed a preliminary view on the company’s intended merger with APN Outdoor (APO) regarding a substantial lessening of competition if it goes ahead in the current form.

Credit Suisse observes the statement provides very little room to manoeuvre, with no obvious areas where a compromise can be reached.

The broker notes oOh!media operates in less challenged categories than does APN Outdoor and does not have the same extent of near-term contract risk.

As the stock trades at a discount to APO, the broker upgrades to Outperform from Neutral. Target is $5.05.

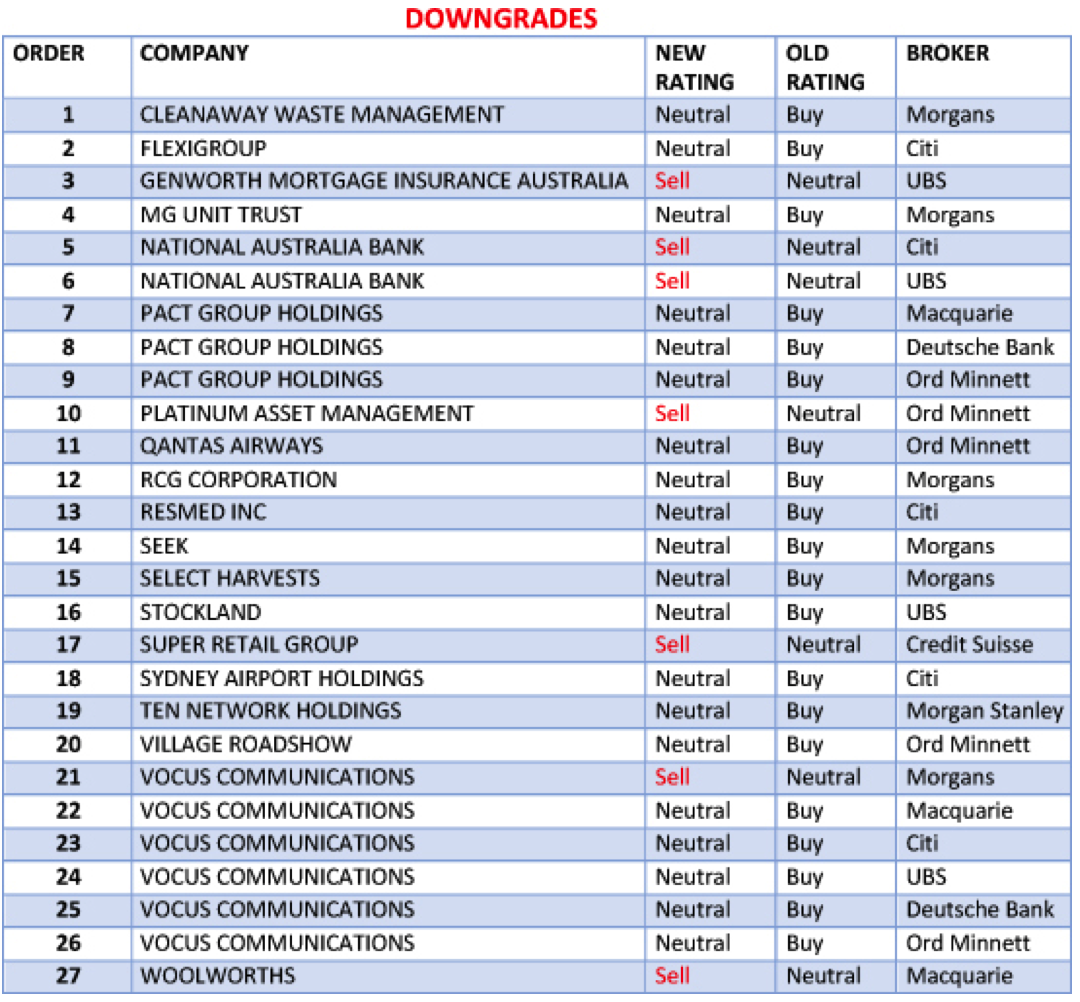

In the not-so-good books

CLEANAWAY WASTE MANAGEMENT LIMITED (CWY) Downgrade to Hold from Add by Morgans B/H/S: 2/4/0

Morgans takes the opportunity to moderate the average sales price assumed for recycled waste oils, as per movements in oil prices. This reduces the broker’s growth outlook, albeit strong growth is still assumed for FY17 via cost reductions and contract wins.

The broker downgrades FY17-19 forecasts for EBITDA by -1-2%. Target is lifted to $1.30 from $1.22. The share price has been strong and is currently trading in line with the revised target and the broker downgrades to Hold from Add.

MG UNIT TRUST (MGC) Downgrade to Hold from Add by Morgans B/H/S: 0/2/0

The company has completed its asset and footprint review. Morgans observes unit holders, as opposed to suppliers or shareholders, will bear the brunt of the company’s announcements, which are expected to lower its cost base so that it can pay a more competitive farm-gate milk price.

This highlights to the broker a mis-alignment of interests between the two. The quantum of write-downs was also larger than expected and the board has suspended the dividend.

Therefore, unit holders are no longer paid to wait for new management to turn the business around, and with no dividend yield support the broker believes the share price will trade sideways.

Rating is downgraded to Hold from Add. Target is reduced to $1.00 from $1.20.

NATIONAL AUSTRALIA BANK LIMITED (NAB) Downgrade to Sell from Neutral by Citi and Downgrade to Sell from Neutral by UBS B/H/S: 4/1/3

Citi’s title above today’s research update says it all, and not just for NAB, but for the sector overall: “Modest beat not enough to keep the stock running”. Post a slightly better than consensus financial performance, the stockbroker downgrades to Sell, price target remains $30.50.

Bad debts remain low, revenues are improving and costs remain under control. It’s just that the share price has rallied hard and the analysts do not believe current level will prove sustainable.

First half results were in line with forecasts. The highlights for UBS were revenue growth of 1.7%, a low bad debt charge, and strong asset quality. The most disappointing element was that falling revenue per share has continued.

UBS supports the bank’s strategy and envisages further opportunities in business banking but questions whether the book is big enough to matter and be a differentiator for the bank.

The broker believes NAB is caught in Australia’s trap, as a large mortgage bank with a dash of business banking. The broker envisages limited room for further appreciation in the share price and downgrades to Sell from Neutral. Target is $30.

PACT GROUP HOLDINGS LTD (PGH) Downgrade to Hold from Accumulate by Ord Minnett B/H/S: 0/6/0

The company has pointed to particularly weak trading conditions in April for the rigid packaging business. On Ord Minnett estimates, guidance implies revenue is set to decline around -6% on an organic in the second half.

While the market’s reaction to the announcement is overdone, in the broker’s opinion, given the stock is trading within 3.8% of the target, the recommendation is reduced to Hold from Accumulate. Target is reduced to $6.85 from $7.00.

QANTAS AIRWAYS LIMITED (QAN) Downgrade to Hold from Buy by Ord Minnett B/H/S: 6/1/0

Ord Minnett reports its analysis of recent operating trends suggests no significant improvement in key domestic and international air travel markets. This conclusion has led to the decision to downgrade Qantas to Hold from Buy. Target price falls to $4.05 from $4.30.

RCG CORPORATION LIMITED (RCG) Downgrade to Hold from Add by Morgans B/H/S: 1/1/0

The trading update disappointed Morgans and the recommendation is downgraded to Hold from Add.

The broker lowers FY17 sales assumptions to be in line with the company’s downgraded forecasts, as FY17 underlying EBITDA is reduced to $74-80m versus previous guidance of $85-88m.

The broker is now prepared to wait until positive momentum re-emerges in sales growth before becoming more comfortable with the stock. Target is reduced to $0.68 from $1.32.

SUPER RETAIL GROUP LIMITED (SUL) Downgrade to Underperform from Neutral by Credit Suisse B/H/S: 7/0/1

Credit Suisse reduces sales growth and gross margin assumptions to reflect increased investment in price and this results in earnings downgrades across the forecast horizon.

The broker observes the consumer environment has deteriorated, which is reflected in a marked slowing down in sales growth in the second half across all divisions.

Rating is downgraded to Underperform from Neutral. Target is reduced to $8.68 from $10.42.

VOCUS COMMUNICATIONS LIMITED (VOC) Downgrade to Neutral from Outperform by Macquarie and Downgrade to Reduce from Hold by Morgans B/H/S: 0/7/1

The company provided a disappointing update and, given the size of downgrades over a short period of time, Macquarie moves to Neutral from Outperform. This is reflecting ongoing uncertainty over the operating side of the business.

The changed accounting approach compounds the downgrade, but also highlights for the broker that the company was relying on a very significant contribution from lumpy network sales in the second half in order to meet guidance. Target is reduced to $3.00 from $5.00.

Morgans is troubled by a number of items in the company’s trading update, including an underlying decline in EBITDA, and negative free cash flow in the second half which has pushed debt levels higher.

While there is long-term upside risk and corporate appeal in the stock it seems to the broker the share price may worsen before it improves.

The broker downgrades to Reduce from Hold and lowers the target to $1.97 from $3.64.

VILLAGE ROADSHOW LIMITED (VRL) Downgrade to Hold from Buy by Ord Minnett B/H/S: 0/4/0

The admission that Gold Coast theme parks are not seeing the numbers of visitors that would have been expected pre-Dreamworld disaster has triggered yet another downgrade to forecasts. On Ord Minnett’s revised numbers this translates into a debt coverage problem. Hence asset sales now have become a must, suggest the analysts.

In addition, with theme park trading weak into the all-important May/June annual pass pre-sale period, Ord Minnett analysts see significant uncertainty overhanging the division into FY18. Downgrade to Hold from Buy. Price target tumbles to $3.53 from $4.63.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.