The chart below shows the buy recommendations of brokers. Companies are only displayed in this table if at least 5 of the above mentioned brokers have a current position on the stock. A broker sentiment value of +1 means all brokers have a buy recommendation. The target price upside/downside is relative to the price at the time the table was updated.

The stocks with the largest target price upside this week are Domino’s Pizza Enterprises with 27.07% and APN News & Media with 28.14%.

[table “266” not found /]

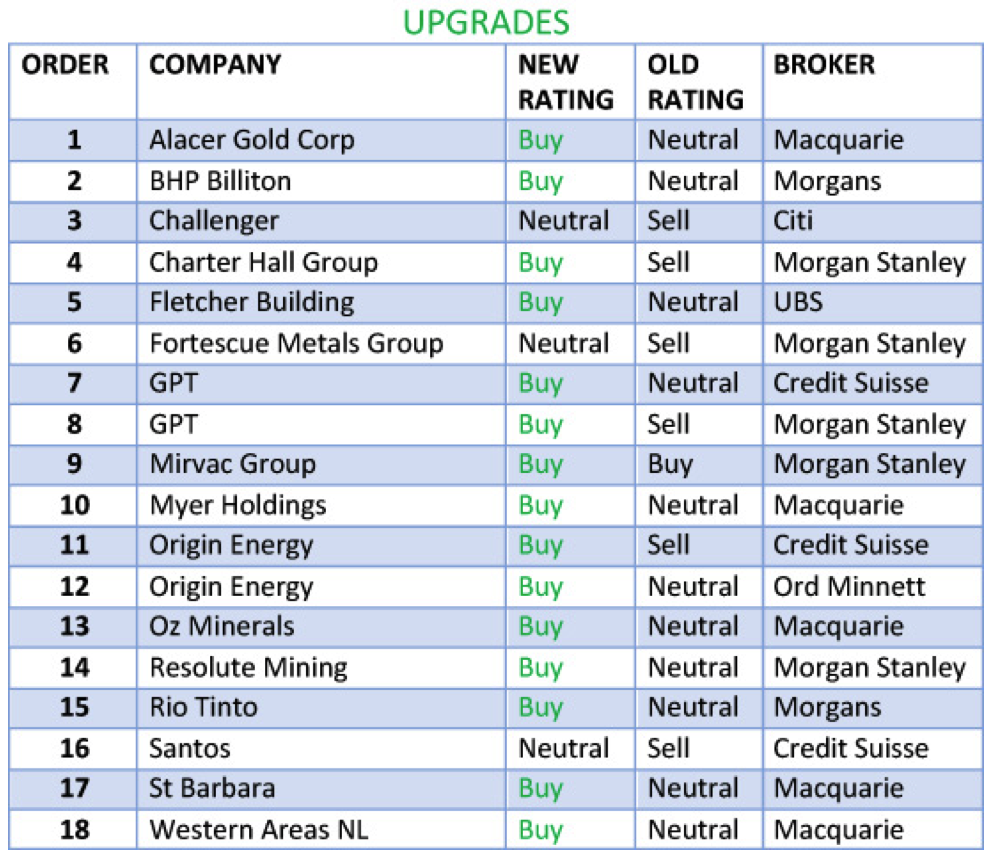

In the good books

BHP BILLITON LIMITED (BHP) Upgrade to Add from Hold by Morgans B/H/S: 3/5/0

Morgans believes the recent volatility in oil and iron ore is primarily driven by the US dollar swinging around, rather than any fundamental factors. Indeed, the broker believes the fundamentals are stronger than the market is accounting for.

The upgrade cycle for resources has a way to go, although miners are expected to remain disciplined in the short term after years of austerity. The broker does acknowledge there is room for some moderation in the iron ore price rally that may mean some additional short-term downside for share prices.

Morgans upgrades to Add from Hold, believing the share price is now back at attractive levels. Target is raised to $28.19 from $27.82.

FLETCHER BUILDING LIMITED (FBU) Upgrade to Buy from Neutral by UBS B/H/S: 4/1/1

UBS observes the stock is now trading at a larger discount to the market than historically has been the case, having been sold off by -11% since the interim result.

The broker continues to forecast peak earnings in FY18 but still expects the New Zealand construction cycle to remain elevated over the medium to longer term.

The stock is not aggressively priced, in the broker’s view, and the rating is upgraded to Buy from Neutral. Target is raised to NZ$9.85 from NZ$10.05.

MYER HOLDINGS LIMITED (MYR) Upgrade to Outperform from Neutral by Macquarie B/H/S: 3/4/0

The first half result was commendable, in Macquarie’s view, although sales were a disappointing aspect. A reduced store footprint will exacerbate the sales decline over the next year. Cost reductions were a clear positive and more is envisaged.

Macquarie upgrades to Outperform from Neutral, as valuation support has materialised and a short term trading opportunity is apparent. Target is reduced to $1.21 from $1.29.

RIO TINTO LIMITED (RIO) Upgrade to Add from Hold by Morgans B/H/S: 7/1/0

Morgans believes recent share price weakness, based on volatility in the US dollar, has created an opportunity to add the stock at lower levels.

The broker upgrades to Add from Hold following a further upward revision to its final forecasts. Strength in the iron ore and aluminium markets, and potential upside for copper, has provided exceptional earning strength for Rio Tinto at a time of low capital expenditure.

Target is raised to $65.57 from $62.85.

SANTOS LIMITED (STO) Upgrade to Neutral from Underperform by Credit Suisse B/H/S: 4/4/0

Credit Suisse suggests the risks around the share price might be more balanced now and upgrades to Neutral from Underperform. The broker acknowledges it may be too early on the call, if oil prices continue to slide.

The broker awaits resolutions on the east coast gas market, as the company is clearly at the epicentre. Nevertheless, Credit Suisse continues to wonder where GLNG sits in the debate, as the argument is being made that new gas is expensive to bring to the market.

Credit Suisse continues to have concerns regarding the long-term structural challenges for the company but notes the stock could move both ways, depending largely on the trajectory of the oil price. Target is $3.80.

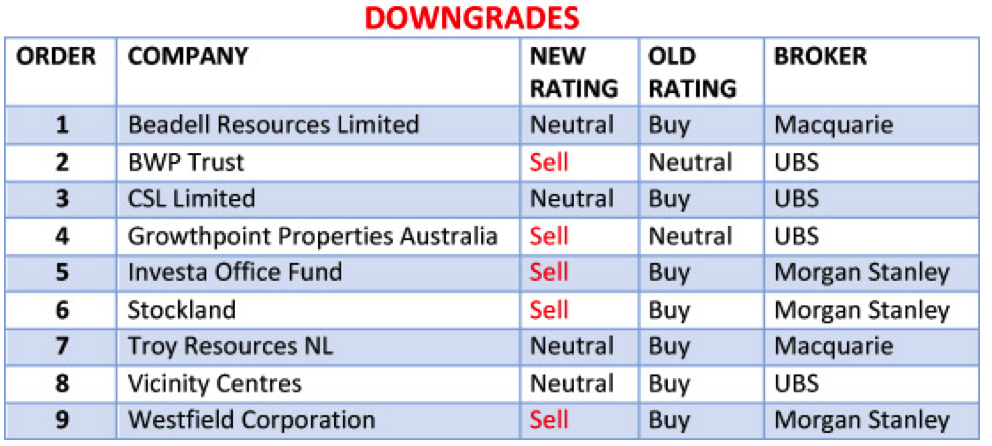

In the not-so-good books

CSL LIMITED (CSL) Downgrade to Neutral from Buy by UBS B/H/S: 4/2/0

CSL is benefiting from plasma supply bottlenecks elsewhere, plus it is in a position to increase its own supply, thus maximising benefits. Did anyone mention Steven Bradbury?

UBS analysts decided to touch base with the industry at a major conference, to get a grip on how long/how much this story has to play out further. Their fresh conclusion: these structurally positive industry conditions support CSL’s market volume expansion well into the medium term.

Price target lifted to $132.15 from $122 as future years estimates increase. Alas, recent price gains have also triggered a downgrade to Neutral from Buy.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.