The chart below shows the buy recommendations of brokers. Companies are only displayed in this table if at least 5 of the above mentioned brokers have a current position on the stock. A broker sentiment value of +1 means all brokers have a buy recommendation. The target price upside/downside is relative to the price at the time the table was updated.

The stocks with the largest target price upside this week are Vocus Communications with 42.4% and NextDC with 45.17%.

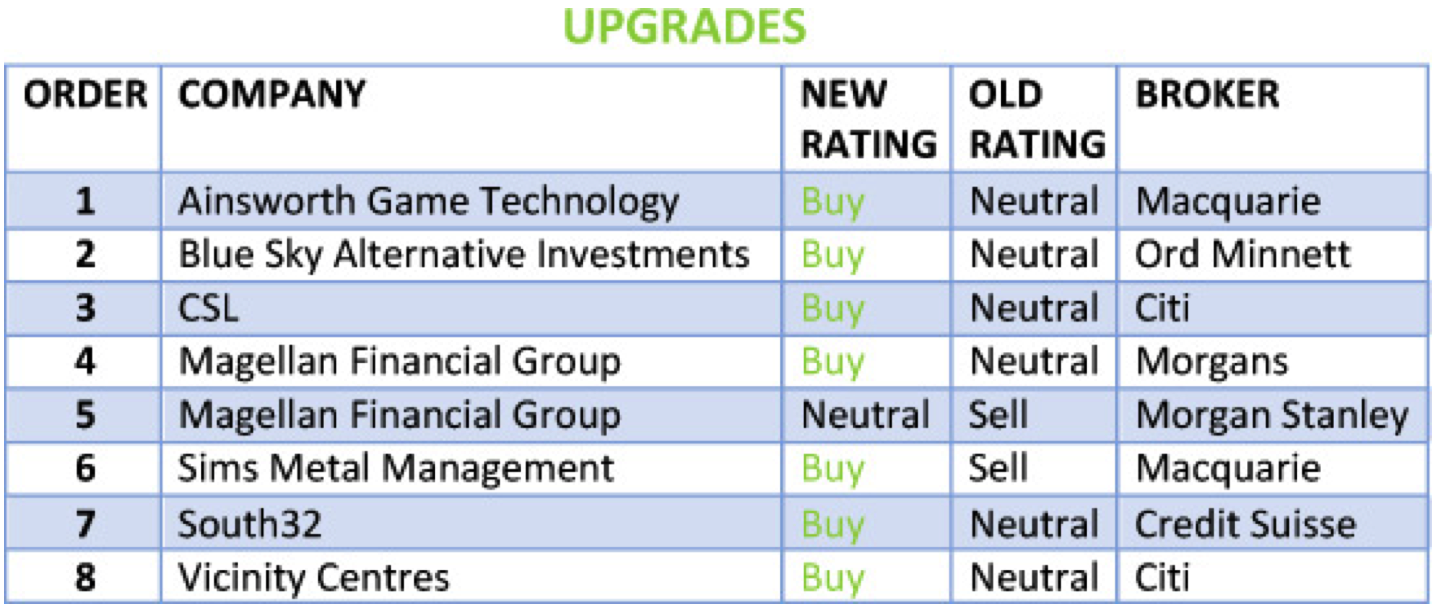

[table “257” not found /]In the good books

CSL LIMITED (CSL) Upgrade to Buy from Neutral by Citi B/H/S: 6/1/0

Post the formal release of CSL’s interim financials, Citi analysts have become a lot more comfortable with the growth outlook. Their projections now imply 21% EPS CAGR for FY16-FY19.

Citi believes this outlook, in combination with the reliability that continues to be on display, warrants a premium valuation. The analysts have increased their price target to $136.40 (was $113.75). Upgrade to Buy from Neutral.

SOUTH32 LIMITED (S32) Upgrade to Outperform from Neutral by Credit Suisse B/H/S: 5/2/0

First half results were slightly better than the broker’s estimates, FY17 guidance for D&A has been revised upward by $40m to $$760m.

FY17 production guidance remains unchanged, but cost guidance has been increased across most divisions, reflecting FX moves and price linked royalty payments. The broker forecasts cash of $1.6bn at the end of FY17 and assumes $800m of buy-backs in each of FY18 and FY19.

The broker upgrades the stock to Outperform from Neutral and raises the target price to $2.95 from $2.80.

SIMS METAL MANAGEMENT LIMITED (SGM) Upgrade to Outperform from Underperform by Macquarie B/H/S: 4/2/1

First half results were in the middle of the guidance range. Macquarie finds the market environment far from clear but believes the company has done well to mitigate downside risks.

The company believes further self-help could add more than 50% to EBIT. On the strength of such potential, Macquarie upgrades to Outperform from Underperform. Target is raised to $13.60 from $11.20.

VICINITY CENTRES (VCX) Upgrade to Buy from Neutral by Citi B/H/S: 3/0/2

At face value, the H1 financial performance was in-line, but Citi analysts highlight the result also put the limelight on the broader benefits of capital recycling.

Upgrade to Buy from Neutral. Target price loses 2c to $3.22. The analysts point out the shares are now offering circa 6% yield plus 10% upside to the price target for the year ahead.

Estimates have changed little. Citi analysts encourage investors to look through the earnings impact of asset sales. They expect growth to accelerate from FY18.

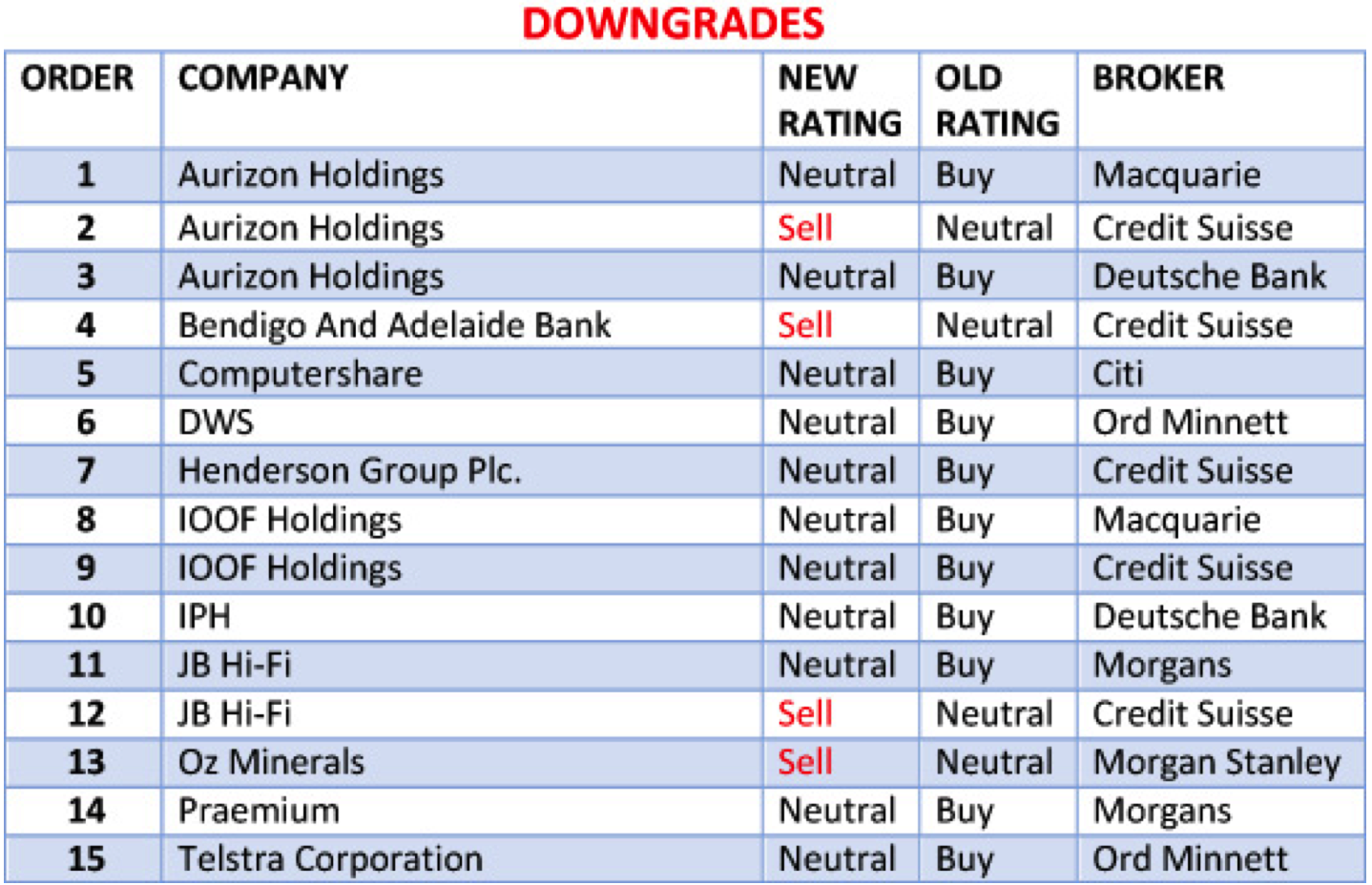

In the not-so-good books

COMPUTERSHARE LIMITED (CPU) Downgrade to Neutral from Buy by Citi B/H/S: 4/3/1

Computershare’s growth outlook has changed dramatically, and for the better, comment analysts at Citi. They have made only small positive adjustments to estimates.

However, the analysts also note the share price has rallied hard. On this basis, they downgrade to Neutral from Buy. Target jumps to $13.80 from $11.

IOOF HOLDINGS LIMITED (IFL) Downgrade to Neutral from Outperform by Macquarie and Downgrade to Neutral from Outperform by Credit Suisse B/H/S: 0/4/1

First half underlying profit missed Macquarie’s expectations. Gross margin pressure flowed through to net margins. The dividend payout of 98% was ahead of forecasts, backed by strong cash flow, but the broker expects this to return to 90%.

Macquarie downgrades to Neutral from Outperform as operating headwinds are expected to remain despite the prospect of some moderation in the second half. Target is reduced to $8.50 from $9.60.

First half earnings were disappointing for the broker, despite a small increase in net profit. Credit Suisse has downgraded FY17 forecasts by -6%, primarily driven by business divestments.

The broker notes cost savings have largely come through, but the unexpected divestments raise questions around the earnings outlook. The broker has downgraded the stock to Neutral from Outperform and reduced the target price to $8.60 from $9.50.

IPH LIMITED (IPH) Downgrade to Hold from Buy by Deutsche Bank B/H/S: 1/2/0

Adjusting for unrealised FX gains, first half results were broadly in line with Deutsche Bank forecasts. The broker downgrades to Hold from Buy on valuation grounds.

Medium-term earnings estimates are reduced to better capture the risks around national phase entries being conducted electronically and potential margin compression from increasing competition.

Target is reduced to $5.40 from $6.60.

TELSTRA CORPORATION LIMITED (TLS) Downgrade to Hold from Accumulate by Ord Minnett B/H/S: 0/5/3

Ord Minnett has downgraded to Hold from Accumulate upon Telstra’s release of what turned out a weak interim report. The analysts highlight both top line and bottom line were well off what the market was expecting.

There’s sector dominance and an attractive looking yield, but Ord Minnett is taking a medium-term view and sees potential structural changes and downward pressure. Target falls to $5.35 from $5.45.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.