In the good books

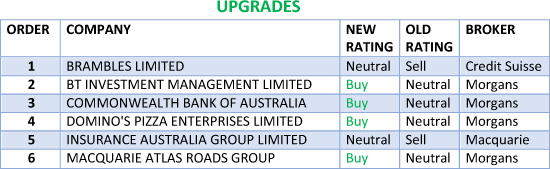

BT INVESTMENT MANAGEMENT LIMITED (BTT) Upgrade to Add from Hold by Morgans B/H/S: 3/3/0

The company has announced it expects direct costs of GBP5m for external research services. The cost will be directly absorbed by JO Hambro.

Factoring in these costs, and reviewing underlying assumptions, leads Morgans to downgrade forecasts for earnings per share by -4-7% in the outer years. Nevertheless, the broker considers the outlook solid and JO Hambro should continue to deliver solid performance fees over the medium term.

Rating is upgraded to Add from Hold. Target is reduced to $11.96 from $12.54.

COMMONWEALTH BANK OF AUSTRALIA (CBA) Upgrade to Add from Hold by Morgans B/H/S: 1/5/2

Morgans believes the agreement to sell the life businesses in Australasia is a positive for shareholders. The broker calculates it will provide a 30 basis points uplift to the group return on tangible equity. The transaction is also expected to result in a pro–forma uplift to the FY17 CET1 capital ratio of around 70 basis points.

Morgans adjusts forecasts for the expected sale, assuming a completion date of September 2018. Given the increased risk of a loss of market share following the announcement of APRA’s prudential inquiry into the bank the broker factors in a higher risk premium to valuation.

This results in a lowering of the target to $80 from $83. Rating is upgraded to Add from Hold.

INSURANCE AUSTRALIA GROUP LIMITED (IAG) Upgrade to Neutral from Underperform by Macquarie B/H/S: 2/6/0

Macquarie upgrades to Neutral from Underperform as management has signalled an intention to participate in further quota share reinsurance deals.

Macquarie notes being more of a distributor means that, while earnings per share may decrease slightly, this should be more than offset by any multiple re-rating and thus deliver value to investors. Target increases to $5.90 from $5.50.

In the not-so-good books

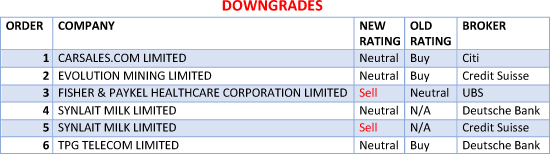

EVOLUTION MINING LIMITED (EVN) Downgrade to Neutral from Outperform by Credit Suisse B/H/S: 4/3/0

The company will sell Edna May for $40m plus a contingent future payment of up to $50m. Credit Suisse observes the transaction structure demonstrates the differential pricing that is applied to mature and challenging assets versus high-quality assets.

The divestment is consistent with the company’s articulated strategy to improve the quality of its portfolio. The broker downgrades to Neutral from Outperform. Target is reduced to $2.22 from $2.30.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.