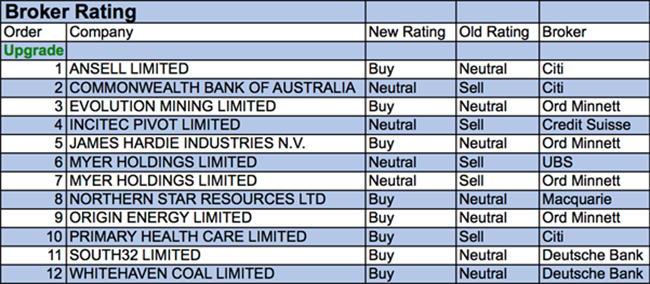

Persistent weakness for the local share market has finally triggered a switch towards recommendation upgrades for individual ASX-listed stocks. For the week ending Friday, 14th September 2018, FNArena registered no less than twelve upgrades versus only three downgrades (see our Thursday report) with troubled department store operator Myer the sole recipient of two upgrades during the week; both to Neutral.

In the good books

ANSELL LIMITED (ANN) was upgraded to Buy from Neutral by Citi. B/H/S: 2/5/1. Citi notes the balance sheet is ungeared post the sale of the sexual wellness business and now explicitly forecasts acquisitions. Management has noted numerous acquisition opportunities and believes it has the capacity to make a transaction worth US$1-1.4 billion. The broker estimates an acquisition worth US$600 million would be accretive to earnings by around 24% in FY21. The broker continues to forecast a progressive US$600 million buyback over FY19-22. Target is raised to $28.50 from $25.50.

EVOLUTION MINING LIMITED (EVN) was upgraded to Accumulate from Hold by Ord Minnett. B/H/S: 4/4/0. Ord Minnett upgrades and raises the target to $3.20 from $3.00. The broker believes the time is right for ASX-listed gold companies to create value through M&A opportunities in North America. A disparity between the ASX gold sector and the Canadian-listed sector creates the opportunity, despite the challenging operating environment, as North America hosts many large high-grade gold systems. The broker estimates its ASX gold coverage will generate US$4 billion in excess capital over the next three years and flags Newcrest Mining (NCM), Evolution Mining and Northern Star (NST) as the most likely to make potential acquisitions in the next 12 months.

MYER HOLDINGS LIMITED (MYR) was upgraded to Neutral from Sell by UBS and to Hold from Lighten by Ord Minnett. B/H/S: 0/3/3. UBS observes the focus of the FY18 result was how the new CEO, John King, will do things differently, given the business has been in a turnaround mode for the past five years. UBS notes some key positives, such as improvement in like-for-like sales and FY19 tracking in line with the fourth quarter of FY18. FY19-21 estimates for EBIT are revised up 6-9%. Target is raised to $0.41 from $0.37.

FY18 results were ahead of Ord Minnett’s forecasts because of higher gross margins and lower tax. The broker has confidence in the new strategy, despite the weakness in sales over the near term. The target is raised to $0.43 from $0.37. Ord Minnett believes the new CEO has announced a credible strategy, with a focus on online sales growth, a smaller store network and improved organisational structure. This is a strategy that appears more willing to engage with the “discount value” customer and less with the more “aspirational” customer.

In the not-so-good books

Earnings forecast

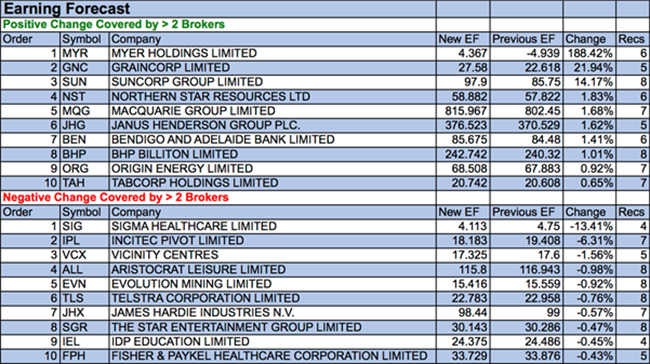

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.