As expected, overall activity among stockbroking analysts has nosedived post the August reporting season.

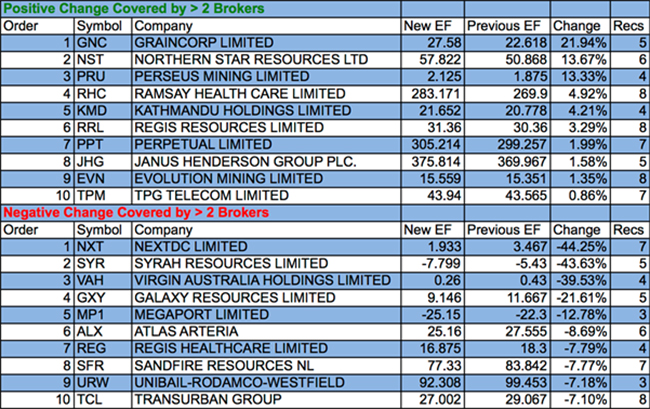

Only three stocks received positive revisions to valuations and price targets during the week with TPG Telecom enjoying the most explosive boost – up 19.98% – followed by Northern Star and an almost undetectable gain for Evolution Mining.

All in all, more (and larger) reductions to earnings estimates, even if this mostly involves mid- and small cap stocks outside the Top50, leaves the Australian share market with a little bit of a sour taste post a moderately positive August reporting season.

However, this is not the reason why September has already revealed its seasonally tough character. For this we can blame global, macro-economic dynamics combined with elevated valuations and a sudden pick-up in investor anxiety.

In the good books

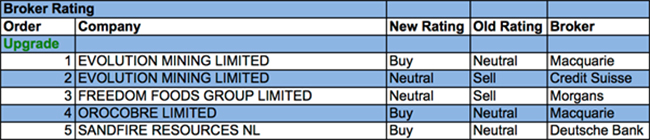

OROCOBRE LIMITED (ORE) was upgraded to Outperform from Neutral by Macquarie. B/H/S: 7/0/1. Operating in Argentina always has its risks, Macquarie notes, hence the announcement of temporary export taxes (or tariffs, or royalties — the broker uses all three in its report), imposed in order to help the country’s foundering economy and appease the IMF, should come as no shock. Even in this case Macquarie sees value, particularly given talk around a buyback and of possible suitors sniffing around. Target falls to $4.40 from $5.00.

In the not-so-good books

AGL ENERGY LIMITED (AGL) was downgraded to Underperform from Neutral by Credit Suisse. B/H/S: 2/4/2. Credit Suisse has reviewed FY18 results and finds the realised wholesale price is higher than previously believed. The broker has modelled a more substantial decline in FY20 and beyond. In the absence of earnings growth the focus is on cash flow and what level of capital return can be supported. The broker’s rating is downgraded to Underperform from Neutral as apparent value is far less compelling now. Target is reduced to $17.70 from $20.60.

THE STAR ENTERTAINMENT GROUP LIMITED (SGR) was downgraded to Neutral from Outperform by Credit Suisse. B/H/S: 7/1/0. Credit Suisse believes the company has managed the migration of its Sydney premium mass customers to an interim facility well. The broker downgrades to Neutral from Outperform because of share price appreciation. Target is steady at $5.60. The next catalyst is considered to be the potential for Chou Tai Fook and Far East to increase their combined holding to 20% from 10%.

SIGMA HEALTHCARE LIMITED (SIG) was downgraded to Underperform from Neutral by Credit Suisse. B/H/S: 0/1/3. First half results were weaker than Credit Suisse expected. Management continues to expect underlying EBIT of $75 million in FY19 before it falls to $40-50 million in FY20 as a result of losing the Chemist Warehouse contract. FY19 guidance implies a strong second half skew of 54%. Credit Suisse considers the short term outlook challenging. The company has appointed Accenture to execute restructuring initiatives but future business strategies remain unclear. The broker considers any restructuring would involve substantial costs and weigh on reported earnings. Target is reduced to $0.48 from $0.52.

SYRAH RESOURCES LIMITED (SYR) was downgraded to Hold from Buy by Deutsche Bank. B/H/S: 3/2/0. The company’s dilutive capital raising should be sufficient to fund commercial production, at which point Deutsche Bank expects guidance on realised basket prices. The graphite market is opaque and the broker believes it is up to Syrah Resources to set clear expectations. On this basis, the broker downgrades long-term realised price expectations to US$800/t from US$920/t, leading to a 20% fall in valuation. Target is reduced to $2.70 from $4.20.

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.