It’s not all about resources stocks in the Australian share market, but miners, energy producers and their service providers certainly remain the centre of attention among stockbroking analysts. For the week ending Friday, 20th July 2018 many of the broker changes were inspired by commodity prices and capex intentions.

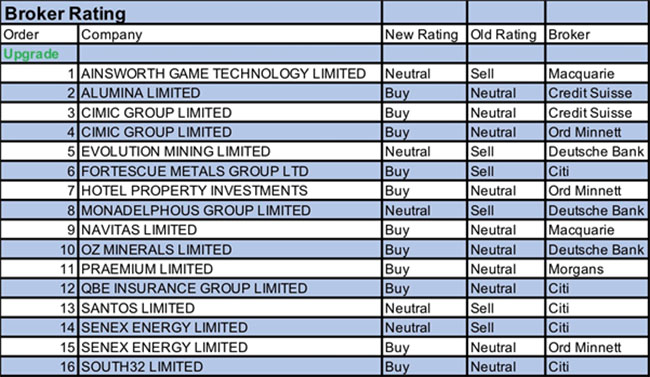

In the good books

AINSWORTH GAME TECHNOLOGY LIMITED (AGI) was upgraded to Neutral from Underperform by Macquarie. B/H/S: 0/1/1. Ainsworth has upgraded FY18 guidance by 8% thanks to increased sales to Churchill Downs in Kentucky. Further increases are possible in FY19, the broker notes, given Churchill Downs has the capacity to add 1100 more units and Ainsworth is sole supplier so far. But the broker remains concerned about underperforming new game releases and in balancing out the positives and negatives, upgrades to Neutral from Underperform, despite the stock having underperformed the ASX300 by -49% since its May profit warning. Target rises to $1.10 from 95c.

ALUMINA LIMITED (AWC) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 3/1/1. Credit Suisse analysts are of the view that the way of least resistance for aluminium prices is south, but they also anticipate margins at JV AWAC are likely to hold up and the combination of these two factors leads to an upgrade in recommendation to Outperform from Neutral. Target price gains 10c on increased estimates which pushes the price target to $3.10.

CIMIC GROUP LIMITED (CIM) was upgraded to Outperform from Neutral by Credit Suisse and Upgrade to Accumulate from Hold by Ord Minnett. B/H/S: 3/2/1. First half net profit was up 12% and ahead of Credit Suisse estimates because of stronger margins. The company has reiterated 2018 net profit guidance of $720-780m. Credit Suisse considers guidance is overly conservative and upgrades to Outperform from Neutral. Target is raised to $47.50 from $45.00. Ord Minnett increases EPS estimates by 3% for 2018 and 2% for 2019. The broker has previously argued that 2018 should be the strongest year of growth for east coast infrastructure-related stocks. With the mining business also growing strongly revenue accelerated in the June quarter. The broker suspects management’s growth estimates are conservative and assumes 12% net profit growth in the second half. Rating is upgraded to Accumulate from Hold. Target rises to $48.90 from $42.80.

EVOLUTION MINING LIMITED (EVN) was upgraded to Hold from Sell by Deutsche Bank. B/H/S: 1/5/2. Deutsche Bank has upgraded Evolution Mining to Hold from Sell, price target $3.00 (was $2.80).

HOTEL PROPERTY INVESTMENTS (HPI) was upgraded to Accumulate from Hold by Ord Minnett. B/H/S: 1/1/0. After reviewing six long WALE real estate investment trusts Ord Minnett notes a total return of 16.3% has been delivered in FY18, outperforming the S&P/ASX 200 REIT index. The broker upgrades Hotel Property Investments to Accumulate from Hold. The stock underperformed the other long WALE REITs in FY18 while offering a 6.6% dividend yield. Target is $3.30.

NAVITAS LIMITED (NVT) was upgraded to Outperform from Neutral by Macquarie B/H/S: 1/4/1/. The company has announced the rationalisation of its careers & industry division and will convert SAE Indonesia to a licensed operation and close two sub-scale SAE US colleges. The remaining six US colleges will be divested or closed because of ongoing regulatory constraints and underperformance. Target is reduced to $4.55 from $4.60.

OZ MINERALS LIMITED (OZL) was upgraded to Buy from Hold by Deutsche Bank. B/H/S: 4/2/0. Deutsche Bank has upgraded OZ Minerals to Buy from Hold while upping the price target to $10.25 from $9.10.

PRAEMIUM LIMITED (PPS) was upgraded to Add from Hold by Morgans. B/H/S: 1/0/0. Praemium reported strong June quarter inflows. Total funds on platform exceeded $8 billion for the first time while Australian funds on platform grew 45% to reach a new record of $5.6 billion. The broker notes the company’s separately managed account platform is considered one of the best platforms currently available. Morgans rolls forward its base year and increases the valuation to $1.07 from $0.69. Rating is upgraded to Add from Hold.

QBE INSURANCE GROUP LIMITED (QBE) was upgraded to Buy from Neutral by Citi. B/H/S: 5/3/0. The upgrade to Buy from Neutral comes with a slightly higher price target -$11.20 instead of $11- as further analysis suggests to Citi analysts that only a reasonable performance in H1 should now suffice to pull the share price a lot higher.

SOUTH32 LIMITED (S32) was upgraded to Buy from Neutral by Citi. B/H/S: 2/5/0. Citi’s upgrade to Buy from Neutral was inspired by higher forecasts for commodities prices. With EPS estimates receiving a boost, also from buybacks and the weakening AUD, the price target lifts to $4.30 from $3.80.

SANTOS LIMITED (STO) was upgraded to Neutral from Sell by Citi. B/H/S: 1/3/2. June quarter production was 7% above Citi’s estimates. Citi observes the Cooper Basin is staging a revival, with a sustained period of reserves and production growth. This has led to an increase in valuation and near-term earnings forecasts. The broker remains aware of the risks of over extending the expected growth in the Cooper Basin, as it has disappointed the market before, but no longer believes a Sell is the right call and upgrades to Neutral. Target is raised to $6.04 from $5.81.

SENEX ENERGY LIMITED (SXY) was upgraded to Accumulate from Hold by Ord Minnett and Upgrade to Neutral from Sell by Citi. B/H/S: 4/3/0. Ord Minnett marks to market oil price forecasts and increases its long-term Brent forecast to US$60/bbl. Ord Minnett considers the sector fully valued and, for the most part, consensus has caught up with its estimates, which indicates the upgrade cycle may now be over, but retains a preference for Senex Energy based on growth and value and upgrades its rating to Accumulate from Hold. Target is steady at $0.46. Beach Energy’s (BPT) reserve upgrade for the Cooper Basin may have positive implications for Senex. Citi has increased its target to 45c from 40c, noting spot oil would imply 55c.

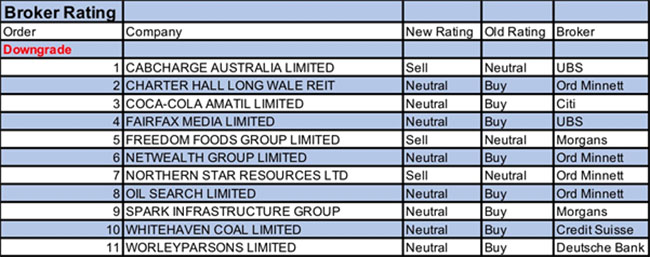

In the not-so-good books

COCA-COLA AMATIL LIMITED (CCL) was downgraded to Neutral from Buy by Citi. B/H/S: 2/4/1. On the expectation that tougher times in Indonesia and PNG will lead to weaker sales and earnings, Citi has downgraded to Neutral from Buy. EPS estimates have been reduced by -0.5% and -1.4% for 2018/19. As Indonesia is supposed to be the next growth engine for the company, the analysts (understandably) suggest investors awaiting a re-rating for the stock, will likely have to be more patient. Target loses -20c to $9.50.

CHARTER HALL LONG WALE REIT (CLW) was downgraded to Hold from Accumulate by Ord Minnett. B/H/S: 0/2/1. Charter Hall LW will divest 50% of the ATO Building in Adelaide for $135m to Charter Hall Direct Office Fund at book value. Ord Minnett considers this a good move as the transaction reduces risk and exposure to a relatively weak market, and frees up capital for another asset with a potentially higher risk-adjusted internal rate of return. The main issue the broker has is that the asset was not put to market, as this raises the question regarding whether Charter Hall LW received full value for the property. Rating is downgraded to Hold from Accumulate on valuation grounds. Target is $4.30.

FAIRFAX MEDIA LIMITED (FXJ) was downgraded to Neutral from Buy by UBS. B/H/S: 3/3/0. Fairfax has finalised agreements with News Corp (NWS) to share printing networks. Fairfax estimates this will result in annualised cost savings of around $15 million. UBS suggests upside from further deals still exists but this is less straightforward and may involve additional capital expenditure considerations. On an annualised basis, ex one-offs, the broker expects the deal to be around 8% accretive to EPS. With the stock price up 21% since February, the broker downgrades to Neutral from Buy on valuation grounds. Target is raised to $0.80 from $0.75.

NORTHERN STAR RESOURCES LTD (NST) was downgraded to Lighten from Hold by Ord Minnett. B/H/S: 1/2/3. Northern Star sustained record production of 184,000 ounces in the June quarter, 10% ahead of Ord Minnett’s estimates. FY19 guidance of 600-640,000 ounces is below expectations, with some conservatism at Kalgoorlie but also lower grades suspected. The broker remains comfortable that the company’s strategy maximises the value of the assets and extends mine life, while acknowledging it does moderate some of the growth optimism embedded in the share price. Target is reduced to $6.30 from $6.50.

OIL SEARCH LIMITED (OSH) was downgraded to Hold from Accumulate by Ord Minnett. B/H/S: 3/4/1. June quarter production was 12% below Ord Minnett estimates and reflected the residual impact from the recent earthquake. A higher proportion of spot sales also affected realised LNG prices. Nevertheless, the issues are temporary and the broker continues to like the outlook. Target is raised to $8.80 from $8.60. As the stock is now trading in line with the target, Ord Minnett downgrades to Hold from Accumulate.

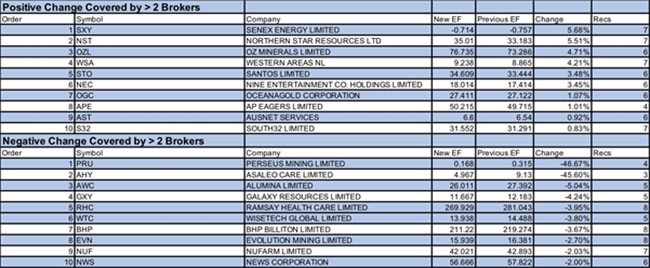

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.