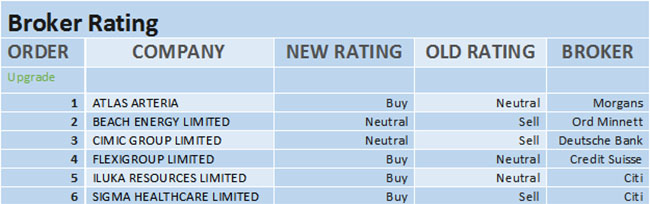

Unsurprisingly, the positive momentum in the Australian share market has triggered more downgrades than upgrades for ASX-listed stocks from stockbroking analysts. For the week ending Friday, 6 July 2018, FNArena registered six upgrades versus 10 downgrades.

Four of the six moved to Buy with Atlas Arteria, FlexiGroup, Iluka Resources and Sigma Healthcare all enjoying an extra Buy rating. Four of the downgrades shifted to Sell, with Domino’s Pizza receiving two of those. The other receivers of a fresh Sell rating were ASX and Magellan Financial Group.

Plenty of positive movements in consensus price targets with Reliance Worldwide grabbing the lead for the week (+6.8%), followed by FlexiGroup, Iluka Resources, and Western Areas. The negative side only contains a small number of stocks, but the negative adjustments are huge. Sigma Healthcare – hardly a surprise – suffered the heaviest blow post loss of a major distribution contract, followed by Aveo Group, then Galaxy Resources.

The table for positive revisions to earnings forecasts is pretty much an all-resources affair with Syrah Resources on top, followed by Western Areas, Newcrest Mining, Orocobre, Santos, and Alumina ltd. The flipside has Perseus Mining receiving the biggest negative adjustment, followed by Sigma Healthcare, Atlas Arteria, and Galaxy Resources.

The local corporate calendar remains thin, but confession season continues to draw out bomb shells in the local share market, predominantly among small caps, with macroeconomic matters dominating in a global risk off environment that ironically has benefited Australian equities over the past two months or so.

Any sector updates on energy or mining should provide ongoing positive momentum to most stocks involved.

In the good books

BEACH ENERGY LIMITED (BPT) Upgrade to Hold from Lighten by Ord Minnett. B/H/S: 1/4/1

Beach Energy has reported a “material increase” in its oil and gas reserves and Ord Minnett has taken the view this event clarifies the medium-term production growth profile; hence an upgrade to Hold from Lighten. From this moment onwards, the company’s production volumes are expected to remain around current levels, explain the analysts. Target price lifts to $1.80 from $1.40.

CIMIC GROUP LIMITED (CIM) Upgrade to Hold from Sell by Deutsche Bank. B/H/S: 1/3/1

Deutsche believes CIMIC’s market valuation has moved to a more realistic level and, given the stock’s more balanced risk-reward profile, upgrades to Hold from Sell. CIMIC’s 12-month price-earnings multiple has fallen from 22x to 18x and the stock’s previous close was $41.68 – just above the broker’s target of $40.50, which is unchanged.

SIGMA HEALTHCARE LIMITED (SIG) Upgrade to Buy from Sell by Citi. B/H/S: 1/1/2

Citi upgrades Sigma Healthcare to Buy from Sell, after confirmation the Chemist Warehouse contract will not be renewed.

The broker cuts earnings per share estimates across FY19-FY21 (-15%, -34% and -17% respectively) to reflect new guidance arising from the news. Target price falls to 55c from 70c.

Downgrade

ASX LIMITED (ASX) Downgrade to Sell from Neutral by Citi. B/H/S: 0/2/6

Even though they see the risk for any disappointments as low in the short term, Citi analysts cannot get past the fact ASX shares seem expensively priced. For this reason, the rating has been downgraded to Sell from Neutral. Target price lifts to $58.40 from $57.85.

COSTA GROUP HOLDINGS LIMITED (CGC) Downgrade to Neutral from Buy by UBS. B/H/S: 2/2/0

UBS downgrades Costa Group to Neutral from Buy on a valuation basis, noting the stock is trading at roughly 27 times the broker’s FY19 earnings-per-share estimate. Triggers to the upside would include a surprisingly strong FY18 result, an upgrade to China guidance or further M&A activity in the avocado business. UBS reduces near-term earnings-per-share forecasts by -2-3%, noting the positive tailwinds of FY18 are likely to wane in 2019. Target price rises to $8.40 from $7.50 to reflect a higher return on investment capital in the international business and a one-year roll forward of the broker’s discounted cash flow valuation.

DOMINO’S PIZZA ENTERPRISES LIMITED (DMP) Downgraded to Underperform from Neutral by Credit Suisse. B/H/S: 3/2/3

Credit Suisse has downgraded Domino’s Pizza Enterprises to Underperform from Neutral, citing structural risks. The broker believes the negatives: the franchise industry inquiry, rising labour costs, aggregator expansion, franchisee attrition, huge growth needs in Europe and uncertainty in Japan; make it difficult to back the market’s sentiment on the stock. Credit Suisse lowers network forecasts yet again and observes organic store openings appear to be lagging guidance. Target Price falls to $36.76 from $42.47.

INGHAMS GROUP LIMITED (ING) Downgrade to Neutral from Outperform by Credit Suisse. B/H/S: 1/5/0

Credit Suisse downgrades to Neutral from Outperform while maintaining a constructive long-term view. However, in the short-term input price pressures (predominately feed) challenging market conditions in New Zealand and a one-off taxation charge point to a muted FY19 EPS outlook. Of the -11% reduction to forecast FY19 EPS, operational changes account for 6% and a higher tax rate 5%. Target reduced to $4.10 from $4.30.

NANOSONICS LIMITED (NAN) Downgrade to Hold from Add by Morgans. B/H/S: 0/1/0

Nanosonics has hit Morgans target price so the broker downgrades to Hold from Add, remaining a long-term fan of the stock. The $3.12 target price is retained. Meanwhile, Canadian and European clearances have been received for the second generation Trophon2 device and the broker expects a launch in early FY19, although a lag would drag on the share price.

VIVA ENERGY REIT (VVR) Downgrade to Accumulate from Buy by Ord Minnett. B/H/S: 3/0/0

Ord Minnett downgrades Viva Energy Reit to Accumulate from Buy on valuation grounds. The target prices is steady at $2.35, the broker noting news on the capital management front (two institutional 8-10-year term loans totalling $60m and delayed-start interest rate swaps totalling $368m) has done little to change valuations.

WOOLWORTHS LIMITED (WOW) Downgrade to Neutral from Buy by Citi. B/H/S: 3/3/2

Citi sees the renewed distribution agreement with Caltex (CTX) as a positive; it explains why the price target moves by 8% to $32.90. Operationally, the analysts continue to forecast Woolworths will outperform peer Coles (WES). Alas, the recent share price rally cannot be ignored, and thus the recommendation is being pulled back to Neutral from Buy. A better pricing in the new agreement means the JV with Caltex will lead to higher profits from petrol sales.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.