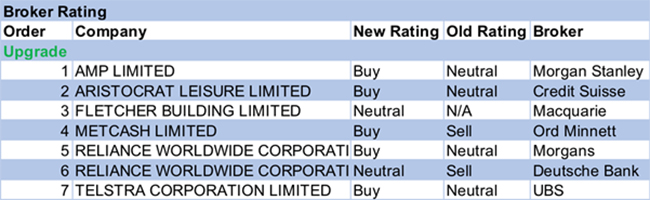

Local plumbers’ favourite Reliance Worldwide made a big acquisition in the UK, in what could prove a transformative event in the company’s development, and two stockbroking analysts responded by upgrading their ratings for the shares. This proved sufficient to keep upgrades and downgrades in perfect balance for the week ending Friday, 25th May 2018.

In the good books

ARISTOCRAT LEISURE LIMITED (ALL) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 7/1/0. Credit Suisse’ response to Aristocrat’s result is to increase forecast earnings by 13%, up its target to $35 from $28, and upgrade its rating to Outperform. The standout performance was posted by digital. The broker sees the potential for the company to scope out a much bigger position in the US mobile games industry from a current 2% market share.

METCASH LIMITED (MTS) was upgraded to Accumulate from Lighten by Ord Minnett. B/H/S: 3/3/1. Ord Minnett reviews the investment thesis and recognises it may have been too hasty in downgrading Metcash. Estimates for EPS are raised by 2.7% for FY19 and 7.4% for FY20 because of forecasts for higher sales and margin in food and grocery and stronger hardware earnings. The broker is more confident that food deflation is easing, while the independent retailer network appears in better shape. Target rises to $3.75 from $2.65.

RELIANCE WORLDWIDE CORPORATION LIMITED (RWC) was upgraded to Add from Hold by Morgans and to Hold from Sell by Deutsche Bank. B/H/S: 2/1/0. The company will acquire John Guest for GBP687.5 million. Morgans believes the acquisition makes strategic sense, providing product, geographic and customer diversification. Morgan’s says the acquisition is expected to complement the company’s existing portfolio and if management can execute well then there are multiple long-term growth opportunities. The target is raised to $5.46 from $4.33. The acquisition also makes strategic sense to Deutsche Bank, given John Guest’s strong PTC offering in Europe. However, Deutsche Bank points out the acquisition adds further risk to a business that has many strategies. Target is raised to $4.35 from $3.90.

TELSTRA CORPORATION LIMITED (TLS) was upgraded to Buy from Neutral by UBS. B/H/S: 4/2/2. UBS continues to believe the $0.22 dividend is unsustainable and a reduction from as early as FY20 is likely. However, with the downside largely known and the full 5G/NBN upside being factored in by the market, the broker upgrades to Buy from Neutral. UBS speculates on an NBN bypass and an aggressive push on market share. Target is raised to $3.00 from $2.80.

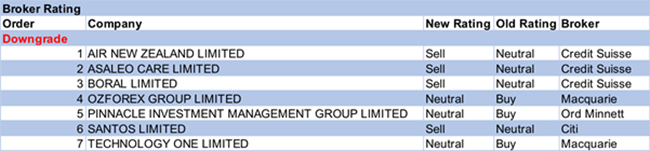

In the not-so-good books

AIR NEW ZEALAND LIMITED (AIZ) was downgraded to Underperform from Neutral by Credit Suisse. B/H/S: 1/1/2. Credit Suisse downgrades to Underperform from Neutral as oil prices have risen, coinciding with a strengthening of the US dollar against the New Zealand dollar. Taking into account current hedging, the broker expects limited impact on FY18 earnings but the persistent increase in oil suggests negative revisions for FY19. Target is reduced to NZ$2.98 from NZ$3.00.

TECHNOLOGY ONE LIMITED (TNE) was downgraded to Neutral from Outperform by Macquarie. B/H/S: 0/3/0. FY18 guidance is below Macquarie’s expectation and implies flat growth year-on-year. The broker notes issues in the consulting division have carried through into FY18 and the UK business is taking longer to reach a profitable scale. Target is $4.77.

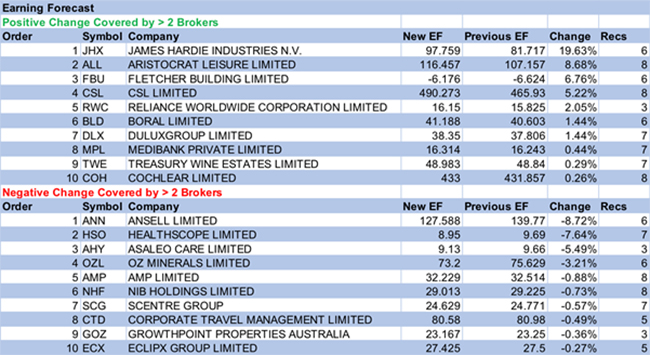

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.