The total number of Buy ratings for the eight stockbrokers monitored daily by FNArena stands now at a firm 45%, with the margin widening, versus 40.24% Neutral and 14.76% Sell ratings. History suggests, when Buy ratings are this far ahead of Neutral/Holds, this might herald tougher times for the local share market.

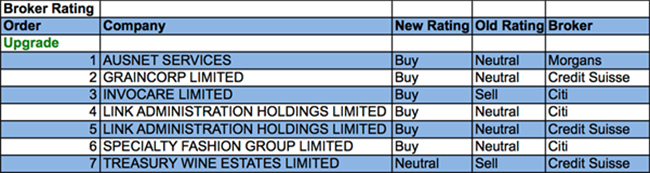

In the good books

TREASURY WINE ESTATES LIMITED (TWE) was upgraded to Neutral from Underperform by Credit Suisse. B/H/S: 3/3/1. Credit Suisse had already identified issues in China with regard to the Rawson’s Retreat brand as early as July last year. Treasury Wine acknowledged the problem at the time and began taking steps to rectify it. Hence the press reports sparking the sell-off in the stock yesterday are old news and, as far as the broker is concerned, exaggerated. Credit Suisse still believes FY19 guidance of 25% earnings growth is achievable, but the broker also believes consensus forecasts for FY20 are too high. Hence an upgrade to Neutral from Underperform on the stock price fall, with an unchanged $15.65 target.

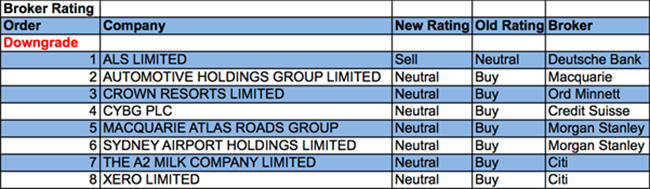

In the not-so-good books

THE A2 MILK COMPANY LIMITED (A2M) was downgraded to Neutral from Buy by Citi. B/H/S: 4/2/0. Citi downgrades given the increased uncertainty around the short-term outlook. The planned transition to new infant formula packaging should be a one-off but the broker is concerned about re-seller price reductions. Citi downgrades FY18-20 estimates for earnings per share by -9-10%. Target is reduced to $11 from $14.

ALS LIMITED (ALQ) was downgraded to Sell from Hold by Deutsche Bank. B/H/S: 2/2/1. The company has benefited from a recovery in mineral drilling activity but Deutsche Bank does not expect it can sustain above-industry growth. Life sciences are supported by structural growth drivers but this is being offset by price pressure across key markets. Deutsche Bank downgrades to Sell from Hold as the stock appears expensive relative to the growth it offers. Target is $6.99.

CROWN RESORTS LIMITED (CWN) was downgraded to Hold from Buy by Ord Minnett. B/H/S: 1/5/0. Ord Minnett reviews its investment thesis and downgrades to Hold from Buy. The share price has increased 12.2% in the year to date and VIPs appear to have shifted in favour of Star Entertainment (SGR). Crown must rebuild its turnover, or gain slots, the broker suggests.

MACQUARIE ATLAS ROADS GROUP (MQA) was downgraded to Equal-weight from Overweight by Morgan Stanley. B/H/S: 5/1/0. Morgan Stanley believes the company presents a complex, but ultimately positive, opportunity for investors, although recent share price gains may temper further gains in view of the performance fee accruing to Macquarie (MQG). Morgan Stanley downgrades to Equal-weight from Overweight. Target is raised to $6.36 from $6.26. Industry view: Cautious.

SYDNEY AIRPORT HOLDINGS LIMITED (SYD) was downgraded to Equal-weight from Overweight by Morgan Stanley. B/H/S: 4/3/0. Morgan Stanley anticipates continued growth in the retail and accommodation development for the business. The passenger outlook remains constructive. The broker suggests if the airport could move from its current movement/minutes base, to a more modern time-based separation system, then on-time performance and longer-term capacity would improve materially. Morgan Stanley downgrades to Equal-weight from Overweight, amid a lack of near-term catalysts, and raises the target to $7.27 from $7.07. Cautious industry view.

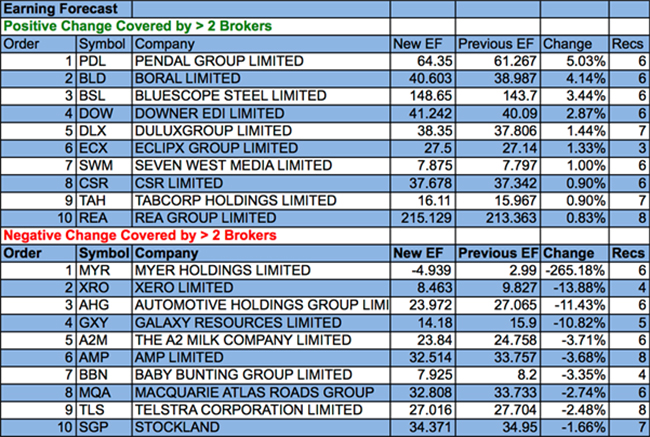

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.