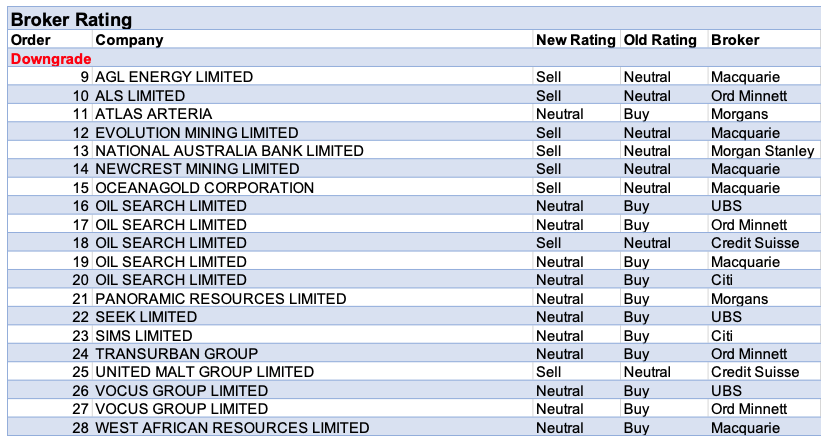

After a near three-month hiatus, there have now been two consecutive weeks of broker downgrades (20 this week) exceeding upgrades (8) for ASX-listed stocks on the FNArena database. For the week ending Friday November 20, this was assisted by multiple downgrades for Oil Search (5) and Vocus Group (2).

While the Oil Search share price had already rallied by 49% during the month on vaccine news, brokers still fear risks may be skewed to the downside. This fear is driven by the disappointing progress on the Alaska sell-down, along with shifting political winds in Papua New Guinea. By contrast, brokers were broadly positive on the earnings and growth path for Vocus Group and downgrades were largely due to recent share price outperformance.

GrainCorp had the week’s largest percentage increase in earnings estimates by brokers in the FNArena database. As per last week’s commentary, this is the result of a positive outlook by management and strong leverage to an expected bumper harvest.

Seven West Media also had a lift in earnings expectations for the reasons detailed above. Next in terms of percentage increase was Aristocrat Leisure, as brokers gain confidence in the revenue momentum within the digital and gaming operations.

Xero’s earnings expectations jumped after the first half slowdown in growth was less than feared. Sales and marketing expenses fell sharply, resulting in a strong boost to profits and cash.

A week wouldn’t be complete without more commentary (and earnings forecast upgrades) surrounding Afterpay. At the company AGM, management noted while October was a record month for underlying sales globally, November is turning out to be even better.

Earnings forecasts were down in percentage terms for Nearmap. As mentioned last week, one broker was expecting slightly higher revenue guidance from management and was averse to the company’s use of constant currency (which implies a -6% foreign exchange headwind).

Finally, Karoon Energy received the second largest downgrade in forecast earnings for the week. Not to fear, as Morgans maintained the company’s Add rating in the wake of the ‘transformational’ Bauna acquisition. In addition, the broker was effusive on the solid prospects for a healthy share price performance, even in the absence of a recovering oil price.

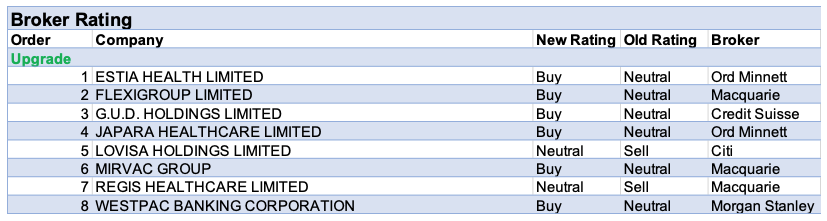

In the good books

ESTIA HEALTH LIMITED (EHE) was upgraded to Accumulate from Hold by Ord Minnett B/H/S: 1/3/0

Ord Minnett notes Washington H Soul Pattinson’s (SOL) bid to acquire Regis Healthcare (REG) highlights the rising investor interest in the aged care sector. The broker believes investors should consider building a position in the sector now despite the continuing uncertainty. Ord Minnett upgrades its rating on Estia Health to Accumulate from Hold. The target rises to $1.85 from $1.40.

FLEXIGROUP LIMITED (FXL) was upgraded to Outperform from Neutral by Macquarie B/H/S: 2/1/0

Shareholders have approved FlexiGroup’s name change to Humm. FlexiGroup’s first-quarter update shows a material upgrade to its FY21 numbers led by improvements in the credit quality. Macquarie has increased its first-half cash net profit estimate to $36.1m from $28.8m primarily led by reduced impairment expenses. The broker also expects receivables growth to return as repayment activity normalises. Rating is upgraded to Outperform from Neutral. Target is raised to $1.40 from $1.33.

G.U.D. HOLDINGS LIMITED (GUD) was upgraded to Outperform from Neutral by Credit Suisse B/H/S: 2/2/0

Credit Suisse notes via the Automotive Components and Accessories division (ACAD) deal, GUD Holdings has diversified into a growing component of the car park while managing to purchase this exposure at a lower multiple from a distressed vendor. Furthermore, the company can add material value to the acquired business in terms of distribution and manufacturing know-how. Incorporating the acquisition drives about 4-5% earnings accretion across FY22-23, adds the broker. Rating is upgraded to Outperform from Neutral with the target unchanged at $13.

JAPARA HEALTHCARE LIMITED (JHC) was upgraded to Buy from Hold by Ord Minnett B/H/S: 1/3/0

Ord Minnett notes Washington H Soul Pattinson’s (SOL) bid to acquire Regis Healthcare (REG) highlights the rising investor interest in the aged care sector. The broker believes investors should consider building a position in the sector now despite continuing uncertainty. Ord Minnett upgrades its rating for Japara Healthcare to Buy from Hold. The target rises to $0.75 from $0.55.

REGIS HEALTHCARE LIMITED (REG) was upgraded to Neutral from Underperform by Macquarie B/H/S: 0/4/0

Washington H. Soul Pattinson (SOL) and its consortium partner, Ashburn have submitted a non-binding proposal to acquire Regis Healthcare for $1.85 per share via a scheme of arrangement. Ashburn controls 27.2% of Regis Healthcare’s shares on issue. Macquarie notes the offer price is at a 25% premium to the closing price of Regis Healthcare’s shares on November 19, equating to an enterprise value of $773m. The broker considers the offer price attractive. Rating is upgraded to Neutral from Underperform with the target price rising to $1.85 from $1.1.

In the not-so-good books

ATLAS ARTERIA (ALX) was downgraded to Hold from Add by Morgans B/H/S: 2/3/0

Morgans downgrades the rating for Atlas Arteria to Hold from Add on recent share price strength and foreign exchange rates. In addition, weaker traffic and CPI indications in France are considered negative factors for valuation. The CPI affects forecasts as it feeds into calculations for any potential APRR (French motorway network) annual toll increase in February 2021. The target price is decreased to $6.74 from $7.01.

OIL SEARCH LIMITED (OSH) was downgraded to Underperform from Neutral by Credit Suisse, to Neutral from Buy by Citi, to Hold from Accumulate by Ord Minnett and to Neutral from Buy by UBS B/H/S: 1/5/1

Credit Suisse downgrades its rating to Underperform from Neutral with the target rising to $3.10 from $3.06. The downgrade is driven by the higher valuation of Alaska offset by the higher capex at the PNG LNG project. The broker fears risks may be skewed to the downside for Oil Search versus peers. This is driven by the disappointing progress on the Alaska sell-down along with political winds in Papua New Guinea which have the potential to go either way. On a more positive note, the broker is pleased with the increased transparency and disclosures by management.

With the recent share price rally, Citi now considers the Oil Search share price fair and downgrades the rating to Neutral from Buy. The broker doesn’t see any material catalysts in the near term and downgrades EPS forecasts largely on oil price revisions. Guidance on capex of US$2.2-2.5bn pre-first oil is in-line with the analyst’s US$2.3bn. The 80kbpd production guidance was a touch lower than the analyst’s 90kbpd. 50% debt cover of capex is in-line. Overall, Citi considers execution, funding and capital structure are key going forward. The target price is increased to $4 from $3.80 on revisions to Alaska late-life production capacity.

Ord Minnett notes the most significant change announced in Oil Search’s investor day pertains to Alaska with a 33% increase in the 2C (contingent) resource and a rephasing of development, which will include a -16% sell-down in Alaska for US$450m. While management had previously flagged synergies between the P’nyang and Papua development projects, the broker believes the JV partners will proceed with the 5mtpa Papua LNG project alone. Noting the share price has already increased by 49% in this month, Ord Minnett downgrades its recommendation to Hold from Accumulate, while the target rises to $4.00 from $3.35.

Oil Search’s investor day presentation has led UBS to upgrade its target to $3.70 from $3.60 due to higher forecast production in Alaska. But a more than 30% increase in share price since the first vaccine announcement has the broker pulling back to Neutral from Buy. Valuation now implies oil at US$58/bbl — the highest across the broker’s coverage — and implies an excessive valuation for long-dated growth projects, UBS suggests. Oil Search is now the broker’s least preferred O&G name.

PANORAMIC RESOURCES LIMITED (PAN) was downgraded to Hold from Add by Morgans B/H/S: 0/1/1

Morgans reviews Panoramic Resources after the share price has rallied around 40% since September. The company’s development activities to support a restart of production at Savannah North are on or ahead of schedule (and on budget), highlights the broker. Management also said they are seeing improving terms and payability in the nickel offtake market. Morgans raises the target price to $0.15 from $0.14 after some changes to foreign exchange assumptions. The rating is decreased to Hold from Speculative Buy.

SEEK LIMITED (SEK) was downgraded to Neutral from Buy by UBS B/H/S: 2/4/0

Seek has upgraded FY21 revenue guidance given all businesses are performing better than was predicted back at the August result. UBS believes guidance may be conservative given current listings momentum. That said, the broker is wary of such momentum reflecting a pull-forward of a return to pre-covid volumes, suggesting it may not be sustainable. Upgraded forecast earnings lead to a target increase to $26 from $22 but UBS pulls back to Neutral from Buy.

SIMS LIMITED (SGM) was downgraded to Neutral from Buy by Citi B/H/S: 2/4/0

Citi highlights the share price of Sims is up 30% in 3 months led by higher aluminium and scrap steel (Turkey) prices. The Turkey scrap steel price is expected to average around US$308/t in FY21. The broker notes Sims margins appear to be thin, meaning there’s plenty of earnings leverage to both the upside and downside. Believing most of the share price upside has been captured, Citi moves to a Neutral rating from Buy. The target price rises to $11 from $9.50.

UNITED MALT GROUP LIMITED (UMG) was downgraded to Underperform from Neutral by Credit Suisse B/H/S: 2/1/1

The maiden FY20 result was ahead of relatively bearish expectations, Credit Suisse asserts. The broker downgrades FY21 estimates to allow for a partial reversion of the current sales trajectory during the northern hemisphere winter. Temporary cost reductions and some government assistance also benefited the business during the year and these inputs may not continue in FY21. Credit Suisse is watching closely for signs of a permanent contraction in craft brewing capacity but forecasts an earnings recovery in FY22 on the basis of a craft market recovery. A rapid increase in the share price following the results has meant the broker downgrades to Underperform from Neutral. Target is raised to $4.23 from $4.02.

VOCUS GROUP LIMITED (VOC) was downgraded to Hold from Buy by Ord Minnett and to Neutral from Buy by UBS B/H/S: 1/5/0

Vocus Group’s decision to progress with the sale of its New Zealand franchise and prioritise investment into Australian fibre and network solutions supports Ord Minnett’s investment case. At its AGM. the group re-affirmed its FY21 operating income guidance. Management reiterates that Vocus networks is in the growth mode, driven by contract wins and rising utilisation on the Australia-Singapore cable. Looking at the recent share price strength, Ord Minnett reduces its rating to Hold from Buy. The target rises to $4.50 from $3.74.

The market had been discounting its valuation of Vocus Group, UBS suggests, based on pessimism over the company’s ability to deliver on earnings forecasts and on under-valuation of its portfolio of assets. The August result and contract wins have countered the first point. Yesterday Vocus announced its intention to IPO its NZ business to bolster the balance sheet and reinstate dividends. Tick box two. The broker has increased its target price to $4.40 from $3.60 but with the market already there, downgrades to Neutral from Buy.

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

The above was compiled from reports on FNArena. The FNArena database tabulates the views of seven major Australian and international stockbrokers: Citi, Credit Suisse, Macquarie, Morgan Stanley, Morgans, Ord Minnett and UBS. Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.