The ASX Bank Index is trading at five-year lows. I think the margin of safety is now high enough to start BUYING the big four Australian banks (even for just a quick short-term seasonal trade).

The case for…

As you know, I’ve been cautious on Australian banks for many years and have not owned them in my fund. On occasions we have been short them tactically. However, over the last week, as prices touched new lows, I decided it was time to start taking advantage of what are now the cheapest bank share prices we have seen in recent times.

We all know how Australian banks got to five-year lows:

- The Royal Commission.

- Earnings downgrades driven by response to The Royal Commission.

- Earnings downgrades driven by weak loan growth.

- Fears of a housing crash.

- Fears of a change of Federal Government and the lowering of the value of franking credits.

- Rotation to growth stocks.

- Flattening yield curves.

- Global bank sector underperformance.

The question then becomes: “Are we at the peak of Australian bank pessimism right now, as all the above are “known knowns” in Donald Rumsfeld terminology?” I think the answer is yes, and I think it’s time to start picking up the vibrating knife that has stuck in the deep contrarian value floor ahead of the pending bank dividend season.

All the major concerns above are “real world” but they’re in the price and, arguably, too much in the price. The way I think of it now, is these negatives are more than priced in, and I ask myself: “What if” the Royal Commission recommendations are less draconian than expected; the earnings downgrade cycle is bottoming right now, with the recent bank charges for client remediation and legal costs; loan growth picks up a notch as banks start loosening credit; the housing market doesn’t crash it just plateaus; there isn’t a change of government; and the bank sector starts leading global markets as global yield curves steepen? If that scenario unfolded, and it’s not unlikely, then Australian banks could generate after-tax total returns of 20% plus from these current share prices over the next 18 months.

What isn’t mentioned in the Australian bank story is credit quality, which remains very sound. Bank balance sheets are in good shape in terms of tier 1 capital and I think this is a very, very important point.

The good news

Pretty much every Australian who wants a job has a job. Australians will service their mortgage under all circumstances. In Australia it remains a “disgrace” to lose your home to the bank, with the social stigma enormous in a population obsessed with property ownership and driven into it by tax advantages. That means, as the GFC showed, that Australians will give up discretionary spending to service their mortgages. I would be far more concerned about discretionary retailers and home improvement companies than Australian mortgage banks right now.

Similarly, Australian corporates are in good balance sheet and interest serviceability positions. Gearing levels are conservative, and I don’t see a bad debt problem on the horizon from the Australian corporate sector.

What we must also remember, and this is the key reason Australian banks have been such a great long-term investment, is that they remain a very cosy oligopoly. That oligopoly, in which they have a deposit funding advantage, has driven, and will continue to drive, high net interest margins and higher ROE’s than global peers. If anything, I think the Royal Commission will make banks better businesses, focusing them on their core business of taking deposits and responsible lending. As they shed non-core sales-based businesses, and lose the ridiculously flawed concept of cross-selling, I think they will be better businesses and better investments.

Disruption for the disruptors

The other threat has been the perception of fintech disruption to the Australian banks. P2P lending has been slow to gain momentum in Australia, and it appears that unregulated credit providers are about to be regulated, as they face a Senate inquiry. Perhaps the high-flying listed fintech space is about to be “disrupted”, if recent price actions in fintech poster children, such as Afterpay (APT), now -52% below recent post capital raising euphoria highs, are any guide (ditto Credit Corp Group:CCP and Money3 Corporation: MNY). This Senate inquiry into the banks credit-providing competitors is good news for the big four banks.

Writing this on Australian banks actually reminds me of that buy note I wrote on Qantas (QAN) at $1.00. The consensus QAN view was just so negative and I knew when I pressed the send button my screen would light up with “you’ve got to be joking” replies. I suspect there will be a similar response to recommending buying Australian banks today, however, the situation is broadly identical in terms of when “known knowns” meet deep contrarian value.

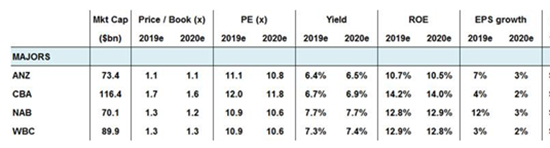

In the context that Australian cash rates will most likely not change for the next year at 1.5%, it’s also worth remembering the dividend yield advantage Australian banks have over cash, even before franking credits are taken into account. Below is the investment arithmetic for the next two years for the big four banks. It’s fair to say you are being paid to take the risk now, with NAB, for example, having a grossed-up dividend yield (at 100% payout ratio) roughly equal to its P/E.

When it comes to seasonality and technical timing, the timing is right now as I am of the view that the US bank sector underperformance is ending, which will have a positive sentiment effect on global banks.

US banks

Let me digress to US banks for a moment, as it’s important to the buy Australian bank thesis.

The US Q1 reporting season for banks is seeing a positive earnings surprise, led by Citi, Bank of America and Morgan Stanley. However, in recent times, there has been a disconnect between rising US bond yields and US bank equity prices.

The chart below, from Vanda Research, highlights the disconnect between the KRE (the benchmark US regional banks ETF) and the US 10YR bond yield.

At AIM, we remain bearish on long duration bonds globally and believe yield curves will continue to steepen from here. This is important as the vast majority of banks borrow short and lend long, with profitability linked, at the margin, to steepening yield curves.

The current disconnect, which we see as an aberration that won’t last, is being driven by concerns around late cycle monetary tightening. We think that is premature and we see Q4 net interest margin (NIM) growth from US banks being strong, leading to a re-rating that will most likely drag up all global banks.

Finally, US banks now emerge from the share buyback blackout period and will be again back on market, buying back large amounts of stock.

In Australia seasonal support for the banks will start to emerge. I asked Richard “Coppo” Coppleson from Bell Potter, who is excellent on seasonal historic trends in Australian equities, to contribute his views on supportive seasonality trends in Australian banks. “Coppo’s” views are below in italics.

Supporting evidence

Banks, after selling off -8.6% in the last 7 weeks – are now a BUY (overweight) for the rest of October (it’s a three to four-week trade – they will bounce) It’s been the winning trade year after year.

- Also, October has been the best month for the S&P/ASX 200 (since 2000) – but the bank rally is the foundation of that rise.

- It’s important to know what is the stand out sectorthat leads the market higher.

- Well, since 2000 the Bank Index, on average, has been up 14 out of the last 18 years, or up a huge 77% of the time.

- The average rise in those 14 years has been a MASSIVE 5.41%, so this is significant.

- The reason, I believe, is that investors chase the banks for their dividends– since hardly any other stocks are going ex-dividend in early November – they tend to see huge buying interest.

The table shows the performance of the S&P/ASX 200 Bank Index over the last 18 years

Source: Coppo report

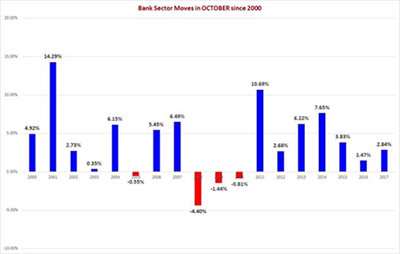

The chart below shows how strong the Bank Index has been in October since 2000

- The average rise has been +3.81%

- Notice that since 2011 it has been up 7 years straight, by an average of 5.05%.

Source: Coppo report

Why are the banks so strong in October?

- One reason has to do with the fact that the three big banks (not CBA) all report in late October/early November and as a result, investors buy them ahead of reporting.

- Over the last 20 odd years I have seen it happen again and again.

- The onlyexceptions come when there is a big “global macro” event that is causing markets to be hit across the globe.

- The banks have been smashed after the Royal Commission, but on a short-term basis it mostly seems to be factored in and a short sharp three-week bounce looks possible.

- With the September reportingseason now over, and all stocks from then have already gone ex dividend, most are in the process right now of “paying” the dividend into investors accounts.

So now …

- So, what happens now is that many investors, in their desperate “hunt for income”, look to where they can next “harvest” income from.

- There are some funds that follow the dividends around and provide big distributions and these funds I know will be buying the banks for their income.

- And what we see is a ‘rotation” out of the stocks that have already paid dividends into the next ones that do.

Now the bank dividends are some of the biggest in the market.

- For instance, we saw in September $18.9 billion in dividends were paid and another $7.3 billion were paid in October.

- So, in total over those 2 months we have $23.7 billionbeing paid.

Now the three big banks have dividends coming up and based on dividend estimates we see each bank paying approximately:

- NAB $2.66 billion (based on a dividend of 99c ff)

- ANZ $2.3 billion (based on a dividend of 80c ff)

- Westpac $3.22 billion (based on a dividend of 94c ff)

Just three stocks will pay a total $8.2 billion versus 380 stocks paying $26.3 billion in September and October.

Also, with the “45 Day rule” this means that retail investors must continuously hold shares ‘at risk’ for at least 45 days to be eligible for the franking tax offset.

The three big banks report in late October / early November:

- 31 October ANZ

- 8 November NAB

- 5 November WBC(day before Melb Cup)

And the ex-dividend dates, based on when they went ex-dividend last year, are roughly around these dates:

- 13 November ANZ

- 9 November NAB

- 14 November WBC

The first ex dividend date (NAB) is approximately four weeks away.

So, there will be investors who will, from now, be buying the banks to secure another major income stream.

- I have seen quant studies done over the years that prove this, whereby the banks “outperform” in the four weeks prior and two weeks post going ex-dividend. (I have been quoting this number for 20 odd years and it seems to occur most times).

- It will happen again this year, the only thing that would kill a bank rally from here is a global selloff, which seems to be feared every time we are in October.

Conclusion

It’s time to BUY the big four Australian banks at what could prove the peak of pessimism.

It’s always darkest before the dawn and at these low entry prices, with low expectations discounted, the potential for solid total returns is there.

My approach is not to over-complicate this and for the first time in the three and a half years since my fund started, I now have investments in the big four Australian banks.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.