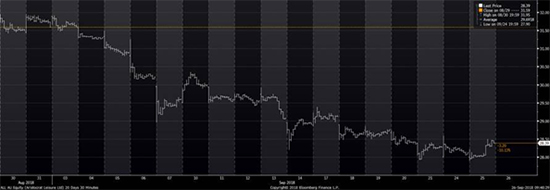

Aristocrat Leisure (ALL) has had a poor performance month, with the chart below showing the stock has fallen almost every day to record a loss of around -10%.

ALL: one-way traffic down this month

The rotation continues

The selling of Aristocrat can be attributed to a variety of development. Firstly, we have seen globally and locally a rotation from “growth” stocks to “value” stocks. Secondly, the Australian dollar appears to have made a short-term bottom and Aristocrat is a majority US dollar earner. And thirdly, analysts have been trimming their Aristocrat EPS forecasts marginally to reflect higher research and development costs. There has also been speculation of a large transition-based seller of Aristocrat, driven by an investment mandate loss.

While I strongly believe we are witnessing the early stages of a rotation from growth to value, as long bond yields break higher, inside that rotation there will be stock specific bottom-up investment opportunities where the rotation has gone too far. I believe Aristocrat at around $28 now represents one of those opportunities as the investment arithmetic is compelling.

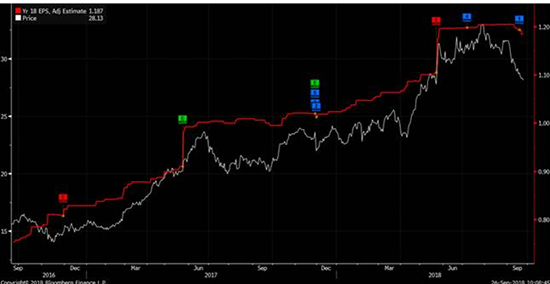

The table below overlays the Aristocrat share price (white line) and current year consensus EPS forecasts (red line).

The next table confirms consensus EPS forecast for 2018 for Aristocrat have been lowered by -1.47% this month, yet remain 18.7% higher than this time 12 months ago.

And the following table confirms consensus EPS forecasts for 2019 for Aristocrat have been lowered by -.96% this month yet remain 25% higher than this time 12 months ago.

An opportunity

Aristocrat shares have dropped -10% on a -1% downgrade to consensus earnings. The consensus FY19 P/E is now under 20 times, at 19.9 times, yet the stock offers another year of likely 20% EPS growth. At a PEG ratio of 1 that is an opportunity ahead of a seasonally strong period for the Aristocrat share price.

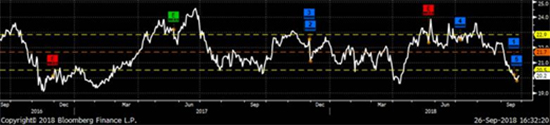

The following graph highlights that Aristocrat is trading one standard deviation below its two-year average PE ratio.

The annual Global Games expo – G2E gaming conference – starts in Las Vegas on 9 October 2018. Aristocrat has led the trade shows over the last four years and it would be fair to expect that to continue as they showcase a further offering of market-leading content. We do expect G2E to reinforce Aristocrat’s market leading position and be the catalyst to reverse the recent share price underperformance.

Upside potential

In addition to a change in market sentiment and positioning, I see several key fundamental drivers of upside to Aristocrat at current levels:

- Organic growth

- Continued industry feedback, surveys and performance data all suggest that Aristocrat is still a clear industry leader.

- Product and technology continue to outperform all relevant competitors.

- The existing land-based business still has significant momentum.

- The majority of noise in the market seems to be around the digital business. We believe the digital growth, and clarity around costs at the November result, will be a positive catalyst for the stock.

- We believe Aristocrat will continue to take market share in the near term.

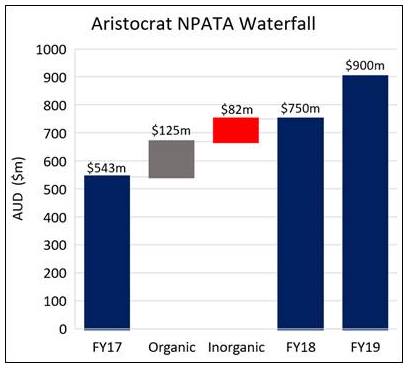

- As is highlighted below, the business is still generating over 23% organic growth based on our estimates for FY18.

- Inorganic growth

- Both digital acquisitions (Plarium in October 2017 and Big Fish in January 2018) will provide a significant contribution to FY18 numbers. See below an NPATA (net profit after tax and amortisation) waterfall chart based on AIM estimates for the next two financial year results.

Source: Company Data, AIM Estimates

Source: Company Data, AIM Estimates

- FY19 will be the first annual period with a full-year inclusion of Plarium and Big Fish.

- We believe it is possible Aristocrat continues to look at inorganic digital opportunities.

- US tax reform

- Greater than 70% of Aristocrat’s earnings are in the United States.

- Guidance for FY18 is a 29% effective rate.

- With a full year benefit of lower taxes in FY19, we estimate the effective tax rate to be closer to 26%.

- There is further scope for this tax rate to go lower in later years.

With this in mind, we believe Aristocrat at current share price levels offers a compelling opportunity. Aristocrat is a world-class company, and this will show at the G2E conference next month.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.