We are past halfway in the local reporting season if we measure by market capitalisation, but far from it in terms of numbers of Australian companies reporting.

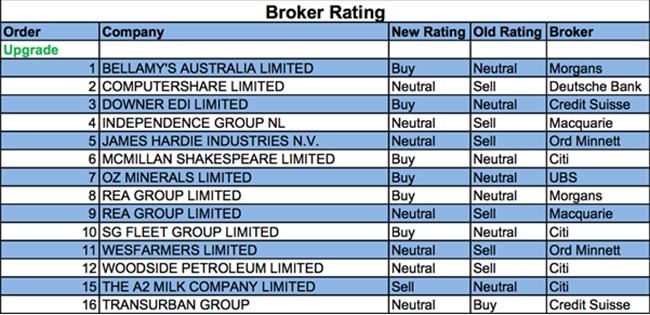

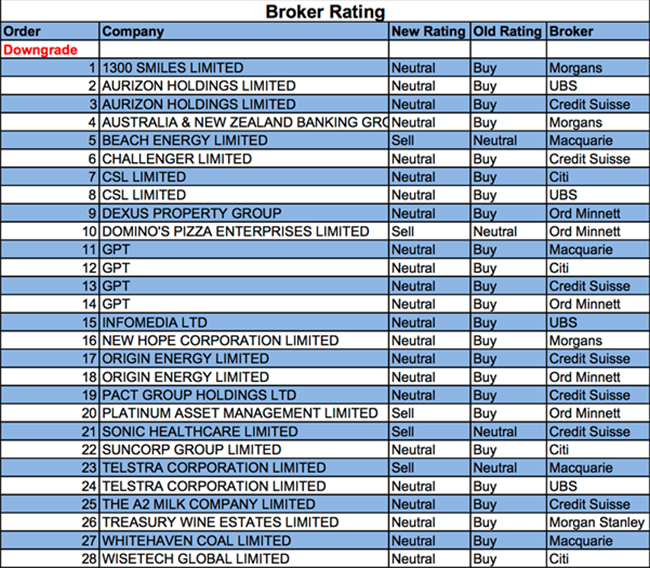

And it is raining downgrades for individual ASX-listed entities. For the week ending Friday, 17th August 2018, FNArena registered no less than 28 downgrades against twelve upgrades. Six out of the dozen upgrades only moved as far as Neutral/Hold.

Consensus target prices provided a positive offset in that average increases proved larger than downward adjustments.

The local reporting season accelerates into much higher numbers in the week ahead.

In the good books

COMPUTERSHARE LIMITED (CPU) was upgraded to Hold from Sell by Deutsche Bank. B/H/S: 0/6/1. FY18 results were in line with guidance and growth was supported by higher margin income and an improved performance in the US. Management EPS was up 14.1% in constant currency terms. Target is $19.20.

DOWNER EDI LIMITED (DOW) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 5/0/0. Downer delivered a full-year result in line with guidance for the seventh year in a row. Management provided a very confident FY19 outlook, underpinned by expected significant improvement from Spotless. Ongoing state government investment in infrastructure and a strong resources sector translate to attractive growth opportunities for Downer. Target rises to $8.25 from $7.00.

JAMES HARDIE INDUSTRIES N.V. (JHX) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 5/2/0. First quarter net profit was below estimates but Ord Minnett is pleased to observe that exterior volume growth has returned to a rate above the segment’s market index. Target is raised to $23.00 from $22.30.

MCMILLAN SHAKESPEARE LIMITED (MMS) was upgraded to Buy from Neutral by Citi. B/H/S: 1/3/0. Organic growth in novated leasing and salary packaging remains robust, while discussions from industry participants seem to be indicating good opportunities for ongoing growth as some fleets transition from corporate to consumer. Citi has made a valuation call, upgrading to Buy from Neutral. Target price has increased to $17.26 from $16.69.

WESFARMERS LIMITED (WES) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 0/5/2. Wesfarmers’ FY18 result beat the broker by a nose, thanks to department store operations and the chemicals, energy and fertilisers business. Despite signs of slower sales from Bunnings, Ord Minnett believes sales will moderate rather than fall sharply. The broker upgrades to Hold from Lighten and increases the target price to $50 from $45.

WOODSIDE PETROLEUM LIMITED (WPL) was upgraded to Neutral from Sell by Citi .B/H/S: 2/5/1. Citi increases the value for Browse in its analysis. However, tolling revenue for the North West Shelf is reduced, which is a net positive, the broker suggests, considering Woodside has a larger equity interest in Browse. First half dividend exceeded the company’s 80% pay-out ratio but, assuming no repeat of one-offs, Citi suspects the second half dividend will return to normal. Target is raised to $34.14 from $30.07.

In the not-so-good books

THE A2 MILK COMPANY LIMITED (A2M) was downgraded to Neutral from Outperform by Credit Suisse. B/H/S: 3/2/1. Supply diversification, expended distribution and China growth are all positive drivers but there’s more to do, the broker suggests, and risks remain while the price is heavily influenced by momentum trading. The share price has been weak since May but is in line with the broker’s valuation. Target is reduced to NZ$11.90 from NZ$12.75.

AUSTRALIA & NEW ZEALAND BANKING GROUP (ANZ) was downgraded to Hold from Add by Morgans. B/H/S: 3/5/0. Morgans finds the extent of the slowdown in the bank’s owner-occupied home loan portfolio baffling and suspects that margin pressures in the institutional business may also be intensifying. Morgans downgrades to Hold from Add because of share price strength. Target is raised to $30 from $29.

CSL LIMITED (CSL) was downgrade to Neutral from Buy by Citi and UBS. B/H/S: 2/6/0. Citi analysts have downgraded, while retaining a price target of $232. The analysts note the shares are now trading at a 31% and 35% premium over the 3-yr trading average P/E and EV/EBITDA, respectively. In a general sense, Citi remains of the view this company’s investments in R&D and capex should allow it to maintain its market leading position in innovation and plasma. UBS downgrades to neutral, but raises target to $220 from $196.

DOMINO’S PIZZA ENTERPRISES LIMITED (DMP) was downgraded to Lighten from Hold by Ord Minnett. B/H/S: 3/1/3. Domino’s Pizza’s FY18 profit missed guidance of 20% growth and fell marginally short of the broker. FY19 guidance also missed consensus. Ord Minnett reduces FY19 and FY20 EPS estimates, reflecting weaker same-store sales. Target price is reduced to $42.50 from $47. Ord Minnett notes that a question mark over expansion targets translates into a less attractive valuation on a discounted cash flow basis.

ORIGIN ENERGY LIMITED (ORG) was downgraded to Hold from Accumulate by Ord Minnett and to Neutral from Outperform by Credit Suisse. B/H/S: 4/4/0. FY18 net profit was 14% below Ord Minnett’s estimates. The contribution from energy markets was above expectations, but the performance of the APLNG business fell short. Ord Minnett finds it difficult to remain positive, given the scale of the downgrades to its estimates. Target is reduced to $9.40 from $10.30. Credit Suisse believes the impact of competition and concessionary measures is greater than expected implying retail margins are lower. Target falls to $9.70 from $10.50.

PACT GROUP HOLDINGS LTD (PGH) was downgraded to Neutral from Outperform by Credit Suisse. B/H/S: 1/4/0. Credit Suisse’s response to Pact’s “bad miss” is to cut forecast earnings by 20%, the target to $4.35 from $5.80 and downgrade to Neutral from Outperform. Volumes were lower and costs higher than the broker expected, and FY19 is not yet offering much relief. The broker suggests Pact is prioritising acquisitions ahead of fixing the core business.

PLATINUM ASSET MANAGEMENT LIMITED (PTM) was downgraded to Sell from Buy by Ord Minnett. B/H/S: 0/2/2. Ord Minnett observes the relative and absolute performance has waned over the last six months. Flows remain reasonable but the broker envisages deterioration leading into FY19. Having upgraded in May on the back of flow momentum, Ord Minnett now downgrades on new evidence including a negative 2.2% absolute performance for the international fund for August. Target is reduced to $4.77 from $6.50.

SONIC HEALTHCARE LIMITED (SHL) was downgraded to Underperform from Neutral by Credit Suisse. B/H/S: 3/4/1. Sonic Healthcare’s result was in line with Credit Suisse and guidance. The broker is forecasting no earnings growth in FY19, as higher pathology volume growth is offset by German and US fee cuts and the rising cost of consumables. Despite a stable regulatory environment for local pathology, the broker sees limited margin expansion in Australia, and sees ongoing risks in Germany. Target falls to $23.50 from $24.00.

TELSTRA CORPORATION LIMITED (TLS) was downgraded to Underperform from Neutral by Macquarie and to Neutral from Buy by UBS. B/H/S: 4/1/3. Telstra’s FY18 result was at the low end of consensus with unchanged guidance. Macquarie expects intensifying competition, particularly in the mobile market where earnings fell 11.6%, will outweigh positives going forward. Target price rises to $2.80 from $2.75. UBS downgrades given the recent re-rating of the stock. UBS envisages upside to the unchanged target of $3.00 from a more rational industry, 5G and the potential for TPG Telecom (TPM) to have a lesser impact than currently anticipated. Equally, UBS suggests downside to a $2.50 target if Telstra fails to execute on its plans and long-term EPS falls to around $0.14 per share.

TREASURY WINE ESTATES LIMITED (TWE) was downgraded to Equal-weight from Overweight by Morgan Stanley. B/H/S: 2/3/2. FY18 earnings were in line with expectations. However, Morgan Stanley notes operating cash flow conversion the quality of earnings deteriorated badly in the second half. Despite very strong growth prospects the broker believes better buying opportunities will emerge and downgrades to Equal-weight from Overweight. $20 target retained. Industry view: Cautious.

WHITEHAVEN COAL LIMITED (WHC) was downgraded to Neutral from Outperform by Macquarie. B/H/S: 3/5/0. FY18 results were in line with expectations. Production guidance has been downgraded, particularly Narrabri, the highest margin mine. Costs are expected to rise to $64/t. The company provided a surprise special dividend, but with no franking credits and net debt back up to $270m, Macquarie is curious why a buyback was not used. Target is reduced to $5.10 from $5.70.

WISETECH GLOBAL LIMITED (WTC) was downgraded to Neutral from Buy by Citi. B/H/S: 1/3/1. Citi has made a valuation call on the stock, downgrading to Neutral from Buy. Target price has increased to $16.21 from $14.12.

Earnings forecast

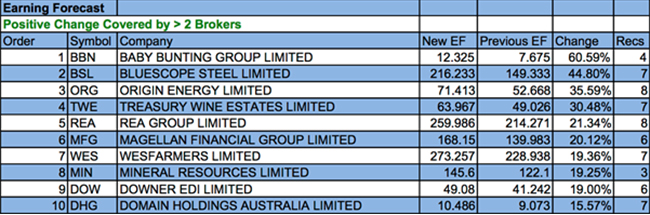

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

The table for negative adjustments is this week cut short due to a technical problem, but it is clear negative adjustments have been smaller than positive revisions during the week. Aveo Group was hit hardest, followed by Telstra and Pilbara Minerals.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.