The ASX is clearly not part of Wall Street, where businesses report better than expected, and in large percentage numbers. In contrast, the local reporting season has started off on a much more benign footing, and last week’s response from stockbroking analysts reflects just that.

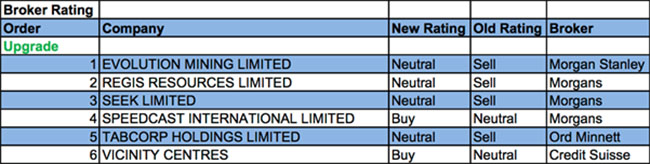

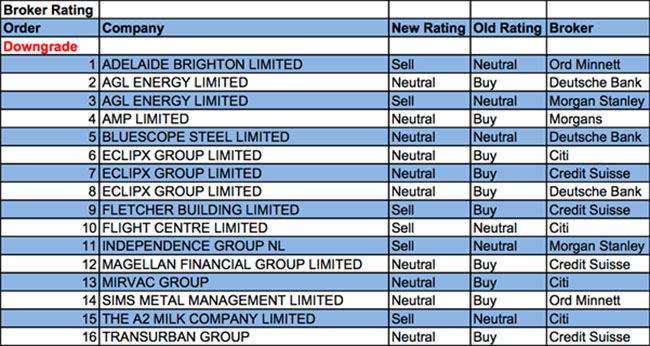

For the week ending Friday, 10th August 2018, FNArena registered 16 downgrades in ratings for individual ASX-listed stocks against only six upgrades, and that pretty much tells the story for the opening week of the August reporting season.

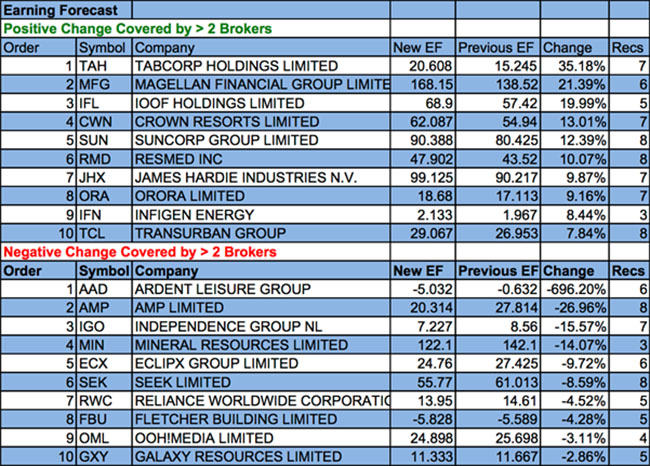

The table for positive revisions to estimates shows a number of large increases, headed by Tabcorp, followed by Magellan Financial, IOOF Holdings, Crown Resorts and Suncorp. On the flipside, there are large reductions for Ardent Leisure, AMP, Independence Group, Mineral Resources, and, yes, EclipX.

Reporting season continues for the next three weeks.

In the good books

EVOLUTION MINING LIMITED (EVN) was upgraded to Equal-weight from Underweight by Morgan Stanley. B/H/S: 2/5/1. Evolution Mining has corrected significantly from its peak and now shows modest downside to Morgan Stanley’s target, revised to $2.60 from $2.70. This has prompted the broker to upgrade to Equal-weight from Underweight, largely driven by better multiples on the base case scenario. Industry view is: In-Line.

SPEEDCAST INTERNATIONAL LIMITED (SDA) was upgraded to Add from Hold by Morgans. B/H/S: 2/2/0. Morgans observes the company is cutting costs to gain growth and expects the first half will be negatively affected by higher costs. Cycling six months of UltiSat is expected to produce an incremental US$30 million in revenue. Offsetting this will be integration costs to realise UltiSat and Harris CapRock synergies. The company will report its results in August 28. Morgans raises the target to $7.21 from $5.57.

TABCORP HOLDINGS LIMITED (TAH) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 6/1/0. Tabcorp’s FY18 results were in line with Ord Minnett forecasts. EBIT was below estimates, due to declines in gaming, lotteries and Keno, plus wagering margins. Ord Minnett has increased its normalised earnings forecasts by 7.5% for FY19 and 9.6% for FY20. Target is lifted to $4.50 from $4.20 and the rating was upgraded in line with the increased valuation.

In the not-so-good books

ADELAIDE BRIGHTON LIMITED (ABC) was downgraded to Lighten from Hold by Ord Minnett. B/H/S: 1/2/2. Ahead of the release of Adelaide Brighton’s half year results on August 22, Ord Minnett downgrades to Lighten from Hold and raises the target price to $6.00 from $5.70.

AGL ENERGY LIMITED (AGL) was downgraded to Underweight from Equal-weight by Morgan Stanley and Downgrade to Hold from Buy by Deutsche Bank. B/H/S: 2/4/1. Morgan Stanley believes AGL’s earnings will peak in FY19, which drives the downgrade. The main policy catalysts are the National Energy Guarantee, the ACCC recommendations and potential direct intervention with respect to Liddell power station. Morgan Stanley reduces the target to $19.44 from $22.88. AGL reported FY18 results that were better than Deutsche Bank expected. Strong wholesale earnings more than offset a significant fall in customer returns and higher costs. The outlook is for flat earnings for at least FY19 and the broker lowers forecasts accordingly, noting wholesale electricity prices are falling and energy retailing and regulatory headwinds continue to confront the company. The broker downgrades reduces the target to $22.25 from $25.45.

AMP LIMITED (AMP) was downgraded to Hold from Add by Morgans. B/H/S: 3/4/1. AMP reported in line with recent guidance. Cost controls in the half were the big positive, Morgans notes, yet management has not altered prior full-year cost guidance, suggesting conservatism. That said, Morgans believes that despite its de-rating, lingering pressures remain on wealth management and wealth protection with regard funds outflow risk and whatever the Royal Commission might yet do. Target falls to $3.88 from $4.56.

BLUESCOPE STEEL LIMITED (BSL) was downgraded to Hold from Buy by Deutsche Bank. B/H/S: 6/1/0. Deutsche Bank increases 2018 steel price estimates for east Asia and the US midwest. The uplift is likely to be short term and the broker expects steel spreads to decline from here on. While recognising this is the high point in the cycle, the broker also believes there is additional risk to earnings given the enterprise agreement that is currently being re-negotiated. Target is raised to $18 from $17.

FLIGHT CENTRE LIMITED (FLT) was downgraded to Sell from Neutral by Citi. B/H/S: 2/3/3. The share price has been on strong uptrend, with Citi analysts referencing a positive turn in the industry’s cycle with oil prices having increased by circa 40% over the past 12 months. This is driving up airfares, helping revenue growth for travel agents such as Flight Centre. However, the immediate outlook will be all about cost out, and with the share price already factoring in material upside, they have decided to downgrade to Sell from Neutral. Target price rises a further 9% to $59, but remains well short of where the share price is trading. Forecasts have been lifted by 3-4%.

INDEPENDENCE GROUP NL (IGO) was downgraded to Underweight from Equal-weight by Morgan Stanley. B/H/S: 2/2/3. Following the updated reserves at Nova, Morgan Stanley remodels the asset and expects negative revisions to consensus estimates for FY19 and FY20. The valuation for Nova has decreased -12% despite accounting for an expanded throughput rate from the second half of FY20. The broker downgrades to Underweight from Equal-weight and lowers the target to $3.85 from $4.45. Industry view is: In-Line.

MAGELLAN FINANCIAL GROUP LIMITED (MFG) was downgraded to Neutral from Outperform by Credit Suisse. B/H/S: 3/2/1. Following a 20% run up in the share price over several months, the stock has re-rated from historical PE lows. Hence, Credit Suisse downgrades to Neutral from Outperform. The broker also has some concerns over fee margins in the medium term, given a recent decision to introduce a new class for the High Conviction fund with a lower management fee. FY18 results were slightly ahead of estimates. The broker raises the target to $29 from $28.

MIRVAC GROUP (MGR) was downgraded to Neutral from Buy by Citi. B/H/S: 3/2/2. It appears Citi analysts had been expecting more, but they do note FY19 guidance came out in-line with market consensus for EPS growth and slightly above it in terms of funds from operations (FFO). All in all, Citi believes the FY18 result, combined with guidance, shows the resilience that is embedded in the business. Nevertheless, they downgrade to Neutral, as suggested upside is insufficient to warrant a Buy rating. Target gains 2c to $2.47.

SIMS METAL MANAGEMENT LIMITED (SGM) was downgraded to Hold from Accumulate by Ord Minnett. B/H/S: 1/3/2. Ord Minnett believes the business is likely to have received benefits from a supportive ferrous scrap environment, with strong export volumes out of both the US and UK. However, the broker is somewhat concerned about a temperate ban on scrap into China that may have had a disproportionately large impact on second half earnings. Target is reduced to $17.00 from $17.20.

TRANSURBAN GROUP (TCL) was downgraded to Neutral from Outperform by Credit Suisse. B/H/S: 5/2/1. The main takeaway from Transurban’s result for Credit Suisse was guidance to 5.5-7.5% compound growth in free cash flow over three years, down from an average midpoint of 11% for the past five. The company appears to be entering a more intensive investment phase, while asset prices remain elevated, and more exposed to delivery challenges for its star NorthConnex project than the broker had expected. NorthConnex is likely to be delayed. Target falls to $12.30 from $12.80.

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.