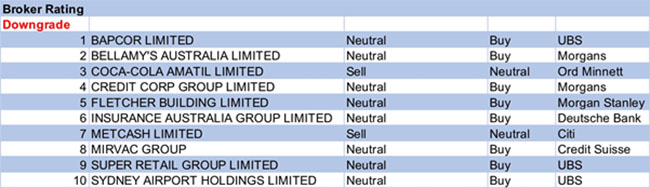

The sudden surge in Australian shares received little sympathy from stockbroking analysts last week, at least not in terms of upgrades and downgrades in ratings for individual ASX-listed stocks.

For the week ending Friday, 22nd June 2018, FNArena counted only four upgrades -of which only two moved to Buy – against ten downgrades. Amongst the latter, only two moved to Sell with Coca-Cola Amatil and Metcash the unlucky recipients.

In the good books

LEND LEASE CORPORATION LIMITED (LLC) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 3/2/0. The company has won a number of major development projects in recent months and Ord Minnett undertakes an in-depth review, focusing on the development earnings to FY24. The broker raises the target to $20 from $17. EPS growth estimates are increased to 8-10% per annum for the next two years.

RAMSAY HEALTH CARE LIMITED (RHC) was upgraded to Buy from Hold by Deutsche Bank. B/H/S: 3/4/1. Ramsay has revealed weak trading conditions in the Australian and UK markets, downgrading FY18 guidance and taking a $125 million impairment charge. Deutsche Bank believes the next two years will be challenging but likes the operating performance, high returns on equity and appealing valuation versus offshore peers. Hence, the rating is upgraded to Buy from Hold. Target is $63.92.

In the not-so-good books

BAPCOR LIMITED (BAP) was downgraded to Neutral from Buy by UBS. B/H/S: 3/1/0. UBS observes the share price is up around 25% over the last six months and while positive about the long-term prospects downgrades to Neutral from Buy. The broker believes the shares are starting to price in a successful roll-out in Asia and a substantial uplift in private-label penetration. Target is raised to $7.00 from $6.40.

BELLAMY’S AUSTRALIA LIMITED (BAL) was downgraded to Hold from Add by Morgans. B/H/S: 1/1/0. Morgans believes the new arrangement to increase Australian organic milk supply is a smart move and will be well received. It takes up to three years to convert conventional farms to organic so it will take time for this supply to materially increase. The share price has had a significant pullback from the highs in March and the broker attributes this to delays in receiving CFDA registration for China-labelled infant formula products. This potentially places FY19 forecasts at risk. For these reasons the broker downgrades to Hold from Add. The main upside risk is a stronger-than-expected FY18 result in August and receipt of CFDA registration sooner than expected. Target is raised to $18.50 from $17.75.

COCA-COLA AMATIL LIMITED (CCL) was downgraded to Lighten from Hold by Ord Minnett. B/H/S: 3/3/1. Ord Minnett has revisited its investment view and notes an absence of strong valuation support. The performance from Indonesia is not improving and the execution risk in the Australian beverages business remains significant. Target of $8.25 is unchanged.

CREDIT CORP GROUP LIMITED (CCP) was downgraded to Hold from Add by Morgans. B/H/S: 0/2/0. Morgans downgrades to Hold from Add, ahead of the company’s expected response to an anonymous sell report. The broker believes the credibility of the sell thesis is low, but secondary and reputation risks have potential to materialise. The primary basis of the report is that the company is avoiding regulatory scrutiny in its lending division by offering a product which is not classified as a small account credit contract (pay-day) loan under consumer regulation.

Short term weakness is likely, given the potential for negative sentiment. Morgans remains positive on the long-term growth prospects and management of the company. Target is steady at $23.

FLETCHER BUILDING LIMITED (FBU) was downgraded to Equal-weight from Overweight by Morgan Stanley. B/H/S: 1/5/0. After the strategy briefing, which confirmed the divestment of Formica and Roof Tile Group, Morgan Stanley believes the outlook rests on the ability to generate improved returns in Australia. Morgan Stanley no longer envisages sufficient upside to support an Overweight rating and downgrades to Equal-weight. Cautious industry view and $6.60 target maintained.

METCASH LIMITED (MTS) was downgraded to Sell from Neutral by Citi. B/H/S: 4/1/2. Industry feedback suggests the risk of another large retailer exiting the Metcash warehouse in 2019 is high, Citi notes, following on from Drakes’ departure. Metcash needs to restore positive sale momentum in order to avoid operating deleverage, the broker suggests. Target falls to $2.50 from $2.80.

SYDNEY AIRPORT HOLDINGS LIMITED (SYD) was downgraded to Neutral from Buy by UBS. B/H/S: 4/4/0. As the stock has outperformed since the February result UBS downgrades to Neutral from Buy. The broker also slightly reduces international traffic growth estimates for 2018 to 5.5% from 6.0%. The broker’s forecasts also show 103% cash flow coverage of the 37.5c distribution guidance. UBS raises the target to $7.30 from $7.10. Beyond 2018 the broker envisages a three-year period of stable and predictable growth in cash flow of 8% despite assumptions that international traffic moderates and effective interest rates rise.

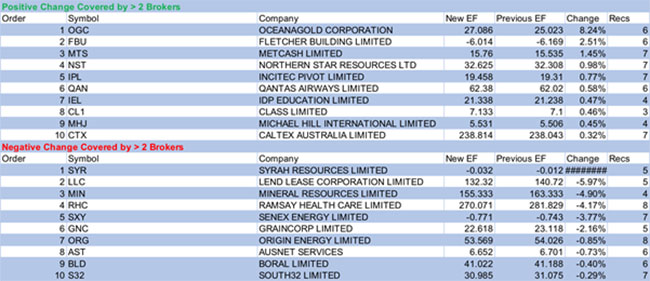

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.