It is always a dangerous strategy to jump too early into a stock that has suffered a major sentiment change. But the case of super fund administrator and registry operator Link Group (LNK) could be the exception to the rule. I reckon that this is a growth stock for the bottom drawer.

Four weeks ago today, Link announced an institutional placement to raise $300 million. This was completed at a price of $8.50 per share, a very tight discount of just 2.4% to the then market price of $8.71. It was accompanied by a Share Purchase Plan for retail investors at the same price of $8.50 per share.

No specific reason was given for the raising, apart from “providing additional balance sheet flexibility to pursue strategic opportunities”. In a note to clients, Goldman Sachs speculated that Link may be looking to acquire online property transaction platform, Property Exchange Australia (PEXA), of which it currently owns a 19.7% stake.

But on Tuesday night in the Budget, the Government announced a plan to ban exit fees and cap passive fees on super accounts with balances under $6,000. It will also implement a consolidation regime that will force the closure of super accounts, which have been inactive for 13 months and have balances below $6,000. Known as the Protecting Your Super Package, this announcement has had a devastating impact on Link’s share price.

Link’s share closed on Friday at $6.98, off 15.9% since its pre-budget close. Compared to the capital raising price of $8.50, the stock is down by 17.9%.

Source: Nabtrade

Link is the largest provider of back office administration services to super funds with a market share of approximately 34%. Clients include AustralianSuper and REST.

The super fund administration business generated 47% of Link’s revenue in the first half but will drop to around 35% when the recently acquired UK business (now known as Link Asset Services – see below) is counted for a full year.

The Government change, which could mean fewer super accounts for Link to administer and potentially lower fees, may be reasonably significant. Link issued a statement to the ASX saying that it couldn’t quantify the impact as the legislation was only in draft form, noting also that it won’t have any impact until FY2020 and that its contracts with super funds usually include volume-based clauses around large movements in member numbers.

UBS estimated that up to 29% of Link’s super accounts may be inactive with an average balance of $12,000. One broker estimated that Link may experience a reduction of 10% in the number of accounts it services. The impact to 2020 earnings was estimated on average to be low single digit (around 4% for Credit Suisse, 2% to 5% by Morgans and up to 10% by Ord Minnett).

Adding to the immediate bearishness was a further announcement by Link that it had lost a contract for CareSuper (1% of the Group’s proforma revenue).

The Link business

In addition to the Fund Administration business, which in recent years has been the key growth driver, Link has three other business units. Corporate Markets, which is a share registry business domiciled mainly in Australia and New Zealand; Information, Digital and Data Services, which is a technology provider to Link’s other business units and external clients (66% of revenue internal, 34% external); and Link Asset Services.

Link Asset Services is the former UK based Capita Asset Services business that was acquired by Link in June 2017 for £888 million. It provides administration and registry services to fund managers, debt issuers and companies in the UK and Ireland.

Buying Capita should be a transformative deal for Link as it will be responsible for 41% of Group revenue and lift the non-Australasian proportion to 46%. Strategically, it is aligned to Link’s growth strategy (for example, exposure to the outsourcing trend in an environment of increasing regulatory complexity), has immediate scale and leadership in the UK and provides a platform for growth in Europe; a defensive financial profile with recurring revenue and opportunity for Link to drive significant growth and post-acquisition efficiencies through the application of technology and investment.

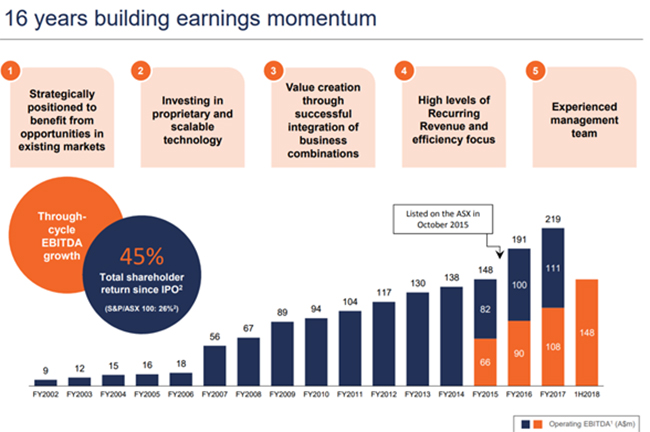

In fact, the Link model is built on identifying mature businesses that have a high degree of recurring revenue, can be readily and efficiently scaled through the application of technology and investment, and have key growth tailwinds (such as outsourcing, superannuation etc). Link has, over the years, successfully acquired and integrated more than 45 businesses.

The following diagram (from Link) shows how it has grown earnings over the last 16 years.

Critically, the Link Group has been led by a very experienced and capable management team. John McMurtrie has been CEO since 2002, while John Hawkins has been the CFO since 2001.

What do the brokers say

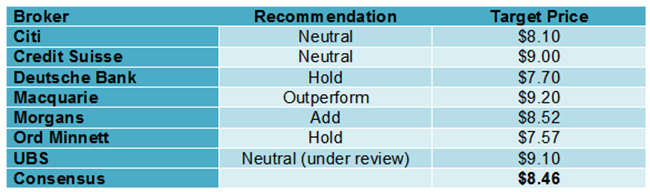

Most of the major brokers reduced their target price for Link following the Budget announcement. Credit Suisse retained its target of $9.00, while UBS placed its rating under ‘review’ and Macquarie is yet to update.

Overall, they are still reasonably positive on Link, with two buy recommendations and five neutral recommendations. The uncertainty over the impact of the change is a common reason for adopting a neutral recommendation. According to FN Arena, the consensus target price sits at $8.46, some 21.1% above Friday’s close of $6.98.

Major Broker Recommendations

My view

Link is a growth business that is now reasonably priced. The fall in share price means that Link is trading on a forecast multiple of 18.2 times FY18 earnings and 15.7 times FY19 earnings. There are risks further out, but this also gives the Company time to adjust.

Link ticks a number of boxes:

- Great track record of growth through selective acquisition;

- Stable, experienced management team;

- Offshore revenue now almost 50% – so will benefit from a weaker Aussie dollar;

- Tailwinds to support long-term growth (superannuation, outsourcing to specialist providers);

- Focus on leveraging technology and driving scale;

- Recurring revenue bias. While exposed to contracting and regulatory risk, quite well insulated from market risk.

Sentiment, once shot, is not turned easily, so it might take a while for Link to regain favour. But I reckon that this is a stock for the bottom drawer.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.