Last week I warned you to ignore “scare broking” and after further developments with the fund manager who wound up his fund and “sold everything”, I am even more resolute in that call now.

The Australian press never “fact checked” the story and ran with it hard. Of course, there now appears more to the story and the real reasons for the fund being wound up are coming out.

As I wrote last week, “the media coverage this generated was completely nonsensical relative to the size or influence of the fund. Quite frankly, had anyone heard of the fund in question before this week? I hadn’t.

“The media coverage was akin to Warren Buffett liquidating his portfolio! It was ridiculous, but these are the headline grabbing days we operate in. “Bad news” gets clicks.

“Clearly there are a variety of reasons to be concerned about the outlook for the Australian economy and the Australian equity market. However, I absolutely DO NOT believe we are at the “sell everything” point, I strongly believe that the ASX200 is morphing into a great LONG/SHORT market where the best returns from here will be generated by funds like my own (AIM Global High Conviction Fund) who can buy the best companies in Australia and short the weakest.”

Fast forward to today, and I was absolutely right to be sceptical of this call and the media’s coverage of it. Quite frankly, it’s a classic example of FAKE NEWS.

I continue to believe there are many stock specific investment opportunities in Australian equities. I remind investors it’s a market of stocks, not a stock market. During periods of index weakness, there are ALWAYS stock specific buying opportunities for genuine investors. This is particularly so when FAKE NEWS headlines about “SELL EVERYTHING” are driving sentiment.

Today I want to take the opportunity Mr Market is giving us and reiterate our positive view on APN Outdoor (APO), a stock that has been beaten down as an Australian cyclical, but we believe unfairly so.

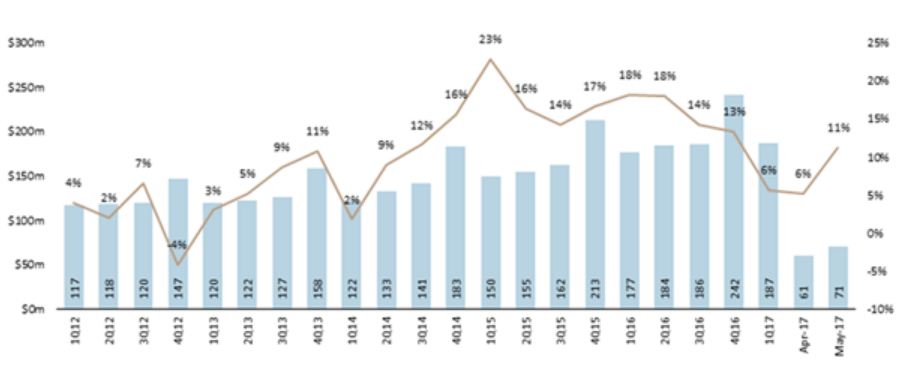

To start top-down at the industry level, the outdoor advertising industry continues to grow.

Total outdoor industry bookings grew by +9.6% to $70.5m in May following April’s revised +6% increase. Year-to-date growth for the total market is now +6.6% year on year to $315.4m. Divisional analysis (based on unadjusted previous corresponding period numbers) suggest:

i) ‘Roadside Billboard’ revenues lifted c16%-18% year on year to $27.3m

ii) ‘Roadside other’ (which includes street furniture, taxis, bus/tram externals, small format) up c9%-11% to $20.4m

iii) ‘Transport’ down c3%-5% year on year to $11.3m and

iv) Retail up c9%-11% year on year to $11.5m

Digital as a proportion of total outdoor revenues was 44.7% in May-17, compared to 36.8% for May-16, implying digital revenue growth of +33% and a -4% decline in static revenues.

Following April’s blip in roadside billboards (c.+4%), growth has returned to the mid-to-high teens % in May and is now up c.13% in CY17 year-to-date. Despite the headline stronger result in large format, with the amount of industry digital inventory coming online, we think OMA data still suggests slower digital yield growth in recent months vs. history. As a reminder, APO is primarily exposed to the roadside billboard segments (c50% of APO revenues), roadside other (c30% of APO revenues), and transport (c20% of revenues).

Outdoor advertising industry growth (year on year %)

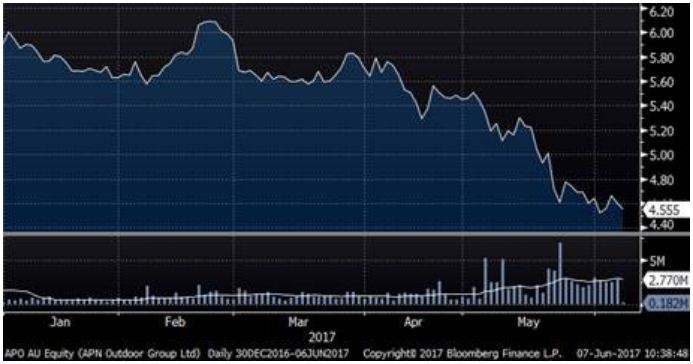

Considering the industry data above is confirming growth, it would now seem odd that APO’s share price has tanked over the last month to levels we consider deep contrarian value. We are not alone in thinking this, as the Packer-backed Ellerston Capital used the APO share price weakness to increase their holding to over 14% of the company.

APO: 2017 YEAR-TO-DATE -25%

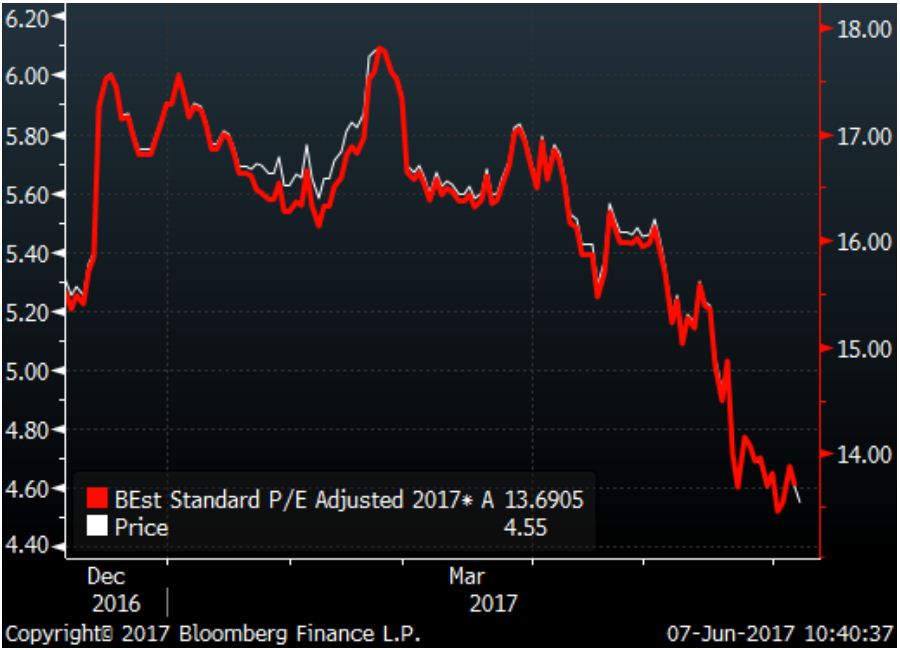

Similarly, the 2017 CY P/E has dropped from 17.5x to around 13.6x.

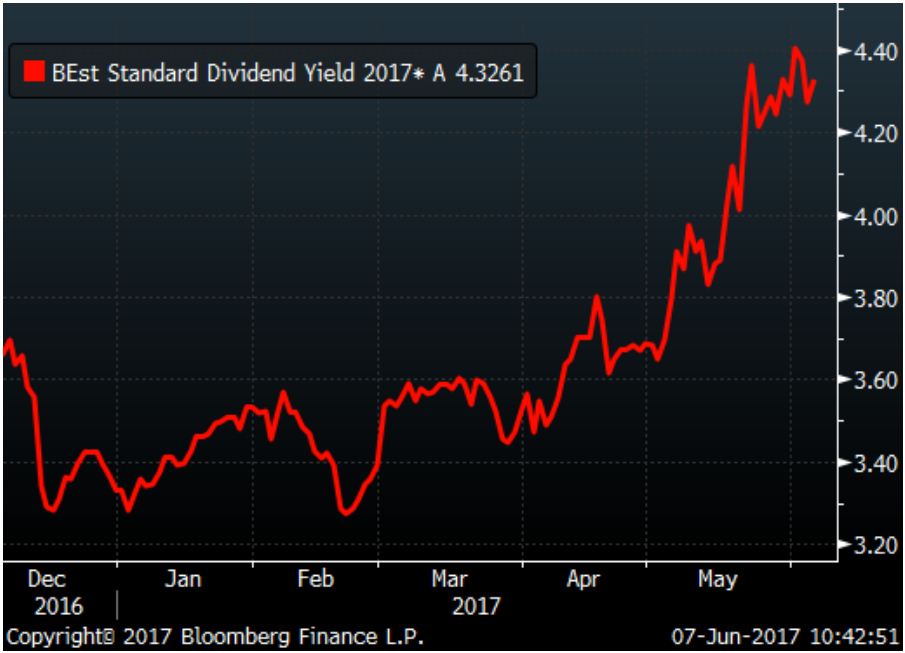

2017 CY prospective dividend yield has risen from 3.4% to 4.4%.

The industry has continued to grow yet its main player, APO has been aggressively de-rated over the same time period.

Some part of this may be disappointment from investors that the merger with oOh!media (OML) was blocked by the ACCC, but that seems somewhat odd as APO was effectively buying OML offering APO shares as collateral. Similarly at no stage was the deal “priced in”, as investors were worried the ACCC would have issues with the deal, which they clearly did.

We thought the confirmation of the deal being blocked would see APO shares stage a relief rally, but for reasons we don’t understand, they quickly fell to 12-month lows. We suspect small cap manager transition flow played a role, but we see the weak price action as an investment opportunity rather than a threat.

APO should deliver 2017 CY EPS growth of +12%. That is stronger than the broader ASX200 will deliver, and the dividend yield has risen to broadly in line with what the index offers. Paying a price to growth ratio of 1x for APO seems too cheap to us, particularly given the structural change to digitalisation of billboards continues with the associated uplift in returns from those digital billboards.

The 2018 CY should see another +10% EPS growth, and this will again look good versus the broader growthless ASX200. In our view the earnings growth outlook for APO remains solid, yet the market is allowing is to buy that multi-year structural growth stream at a P/E discount to the growthless ASX200. That is an opportunity for investors.

APO is a classic example of what I consider a stock specific investment opportunity in a broader market pullback. The broader market pullback should remind you all that there is absolutely no capital protection in index/passive products themselves.

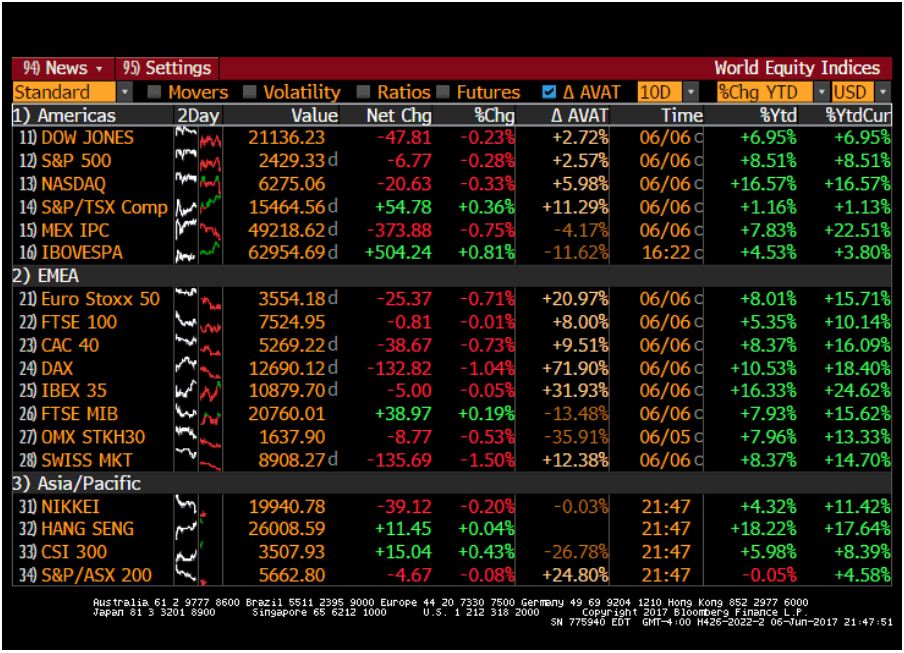

Similarly, it is also worth noting that it is a “market of markets”. By that I mean Australia is just a small part of the global equity world.

“Home bias” is costing Australian investors plenty of relative and absolute performance. The ASX200 is the worst performing market on my developed markets page this year.

The ASX200 is now DOWN for the 2017 year, the underperformance of Wall St, Europe and Asia is as large as I can remember. Our heavy weighting in banks (-7% year-to-date, -14% from highs) & retailers (-18% year-to-date), and our almost non-existent technology sector, is seeing Australia left behind. In fact there appears to be hedge funds shorting Australia to fund rotation to other jurisdictions where earnings growth is up to triple what the ASX200 currently offers.

So don’t listen to the “FAKE NEWS” of sell everything. That’s not the right approach. This is a market of stocks and a market of markets. You can ALWAYS find a number of quality companies GROWING their earnings and dividends and being priced fairly or cheaply.

We remain of the view APN Outdoor (APO) is an example of that in the Australian market right now.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.