Takeovers have been a seemingly permanent feature of Australia’s telecommunications landscape. Smaller telcos joined forces, only to be swallowed by aggressive mid-tier players in the race to become Australia’s next great telco network.

TPG Telecom’s takeover of iiNet in 2015 and Vocus Group’s merger with M2 Group in 2016 are examples. Superloop’s acquisition last year of BigAir, a provider of wireless services to corporate customers, continued the sector-consolidation theme.

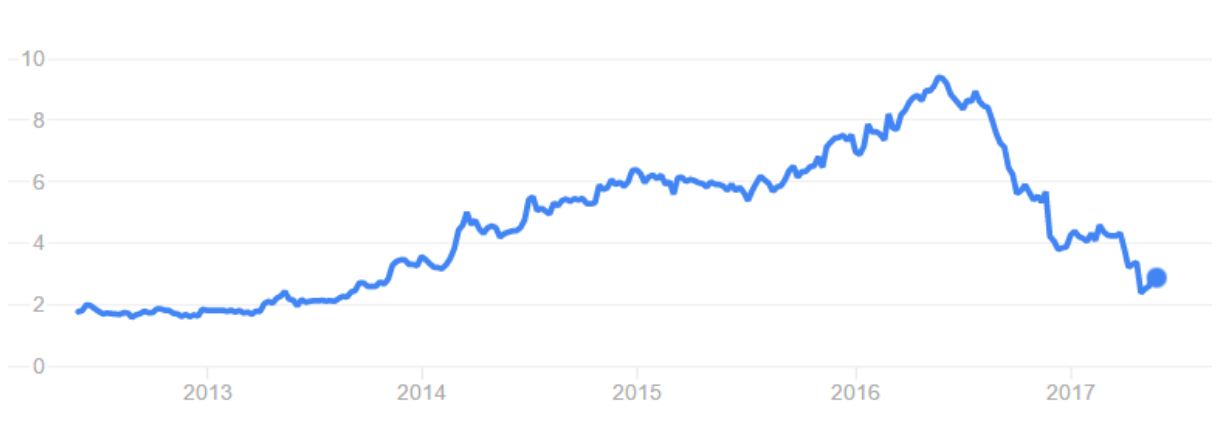

Market chatter tips Vocus as a takeover target for a private-equity firm. The ambitious telco plunged from $9.40 in May 2016 to $2.82 after profit downgrades. A savvy private-equity firm could extract plenty of value from Vocus at those levels.

Credit Suisse reportedly argued that a predator would need to stump up at least $3.30 a share to get its hands on Vocus and its prized infrastructure assets. The company has several non-core assets that could be sold or spun off, adding to its appeal for private equity.

Vocus looks a classic private-equity play. Like many companies that grow rapidly through acquisition, integration issues eventually surface. A business overpays for assets and struggles to extract sufficient synergies, fast enough, to please the market.

A private-equity firm privatises the listed company, solves its integration issues, jettisons non-core assets, fixes the balance sheet and creates value, away from the market’s glare. It might be a similar story to Fairfax Media if private equity has its way, albeit without the complication of acquisitions.

Vocus could attract several suitors and a contested takeover, should the company be in play. Demand for the company’s non-core assets, such as its data centre, is likely. Arguably, Vocus is worth a lot more than the sum of its parts.

But that will not appease the market. Vocus’s earnings update in March was disappointing, given the size and timing of the downgrade. Investors could be forgiven for losing faith, given the company only confirmed guidance in February.

Integration challenges are testing the market’s patience and reducing visibility on Vocus’s FY18 earnings. Investors need to see positive organic growth in the business, particularly in the company’s Enterprise and Wholesale division, and stronger sales momentum.

Vocus’s challenges are exacerbated by a telco sector that has lost favour this financial year. Telstra Corporation has slumped from $5.83 to $4.40 amid fears of rising competition from TPG Telecom in the mobile sector. TPG has halved from its 2016 high after guidance downgrades.

These are serious company and sector headwinds for Vocus and an opportunity for private equity to snap up a business that has strategic value for investors with a medium-term view.

Perhaps private equity believes it can get Vocus cheaper. A consensus of 15 broking firms has a price target of $2.58 for the company, versus the current $2.82. Watch brokers revise price targets lower as Vocus struggles to halt the earning downgrade momentum.

Vocus is not screamingly cheap, despite the share-price falls. But there’s plenty of reason for predators to pounce and enough value for experienced investors who can tolerate higher risk to put Vocus on their takeover radar.

Chart 1: Vocus Group

Source: ASX

Amaysim Australia

As broking firms speculate about Vocus, far less consideration has been given to small-cap operator Amaysim Australia.

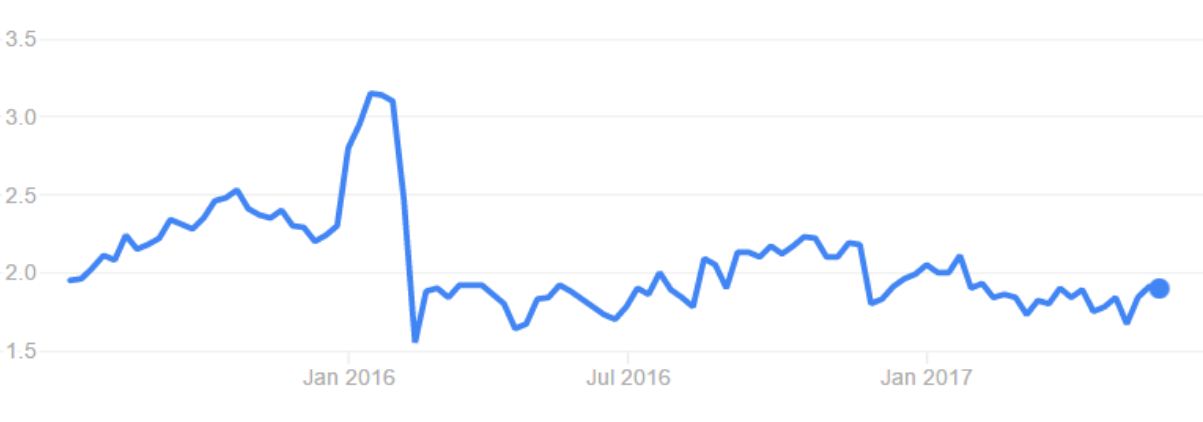

To recap, Amaysim raised $207 million and listed on ASX in July 2015 through a float at $1.80 a share. The price initially soared, then the mobile-services operator tanked to $1.50 in February 2015 after reporting disappointing revenue and customer growth. A sharp downgrade to prospectus subscriber forecasts dented the market’s confidence in the company and it has struggled to get back above the issue price.

Amaysim looks like a basic business. As a reseller of the Optus spectrum, it has lower margins and faces cut-throat competition, which includes retailers such as Aldi that sell phone plans. Buying businesses that do not have a clear advantage in a commoditised, price-taking segment is rarely a good idea.

But Amaysim has some interesting traits. The company’s online model allows it to acquire customers at a fraction of the cost to big telcos and by leasing mobile spectrum off Optus, Amaysim has a relatively capital-light business model compared to telcos that must invest in and maintain networks.

As customer numbers grow, economies of scale improve. Amaysim’s EBITDA margins are rising and it is potentially a very profitable business as scale is built. TPG Telecom’s plan to build its own network and disrupt the mobile market has implications for Amaysim. TPG will need a lot of customer growth to make its $2-billion network investment pay off.

Amaysim’s 1 million-plus subscribers would boost TPG Telecom’s customer base and provide another low-cost channel to keep customer numbers ticking higher. The $5.4 billion TPG Telecom has plenty of firepower to snap up the $400 million Amaysim.

Another possibility is Optus, Amaysim’s wholesale partner, jumping in first to counter the threat of TPG. Optus would lose a decent chunk of subscribers if Amaysim went to TPG and acquiring Amaysim would give Optus wholesale and retail margins on the customer base.

Optus would get Amaysim on a cheap multiple, protect its subscriber base and improve its competitive positioning as TPG expanded in the mobile market.

Whatever happens on the corporate front, Amaysim ticks the first box of takeover investing: finding businesses that are attractive at the current price with or without an acquisition.

A small-cap telco with a million-plus customers and knack of acquiring them at low cost has latent strategic value in a fast-changing mobile-services landscape.

Chart 2: Amaysim Australia

Source: ASX

Portfolio update

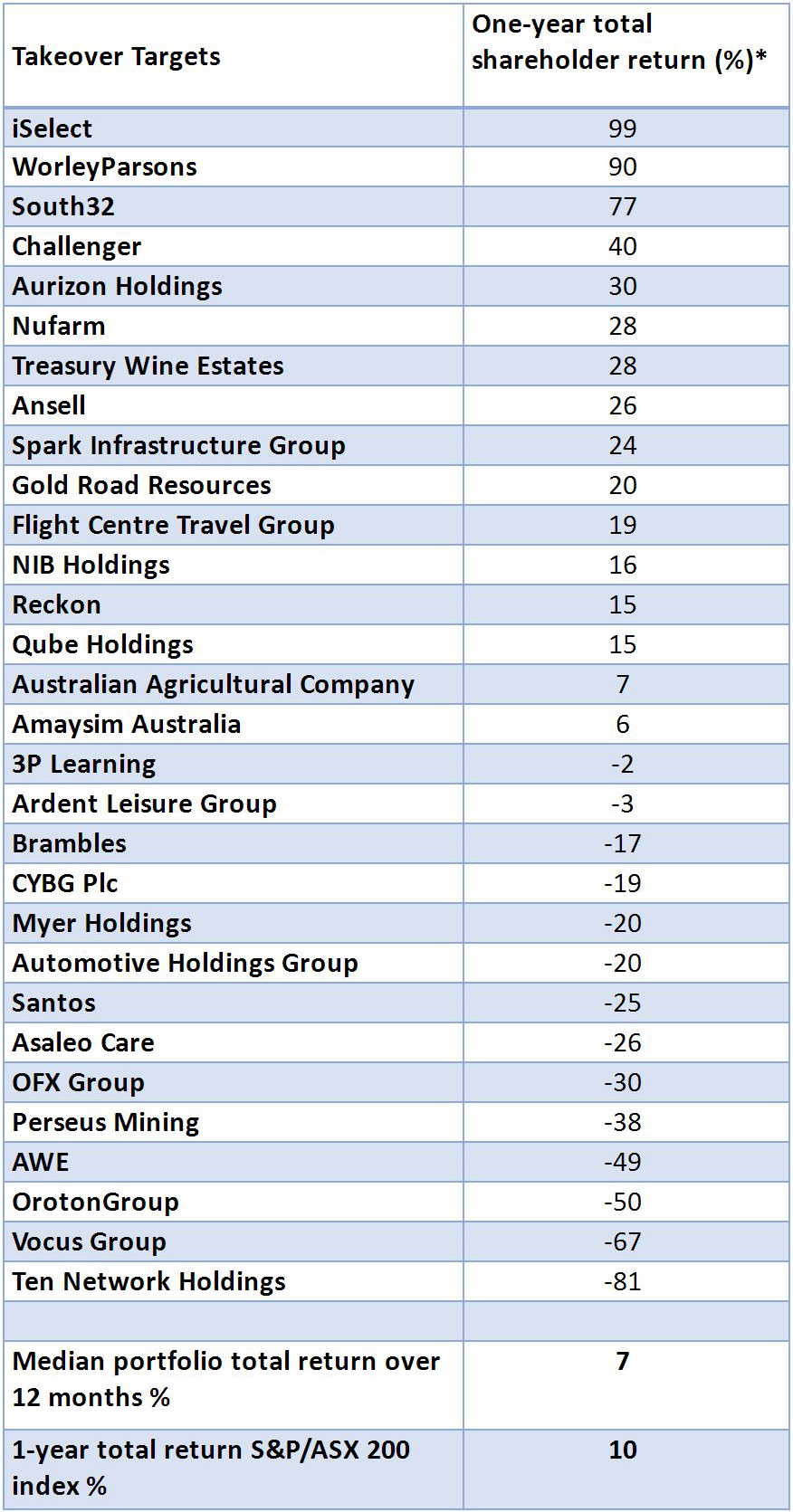

Like the rest of the market, the Switzer Super Report takeover portfolio had a tough second quarter. Deterioration in portfolio laggards, such as Ten Network Holdings and OrotonGroup, weighed on returns, as did Vocus Group’s inclusion. Without Vocus, the portfolio would be tracking slightly above the market return.

Vocus Group and Amaysim this month join the portfolio.

Source: Morningstar (one-year return), Standard and Poor’s (S&P/ASX 200 total return). * assumes dividend reinvestment. Prices at May 31, 2017.

Tony Featherstone is a former managing editor of BRW and Shares magazines. All prices and analysis at May 31, 2017.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.