Maybe it is the onset of those cold wintery mornings, but for the first time in almost a decade, I am feeling a little cool on the Aussie stock market. Not cold, but cool. I am thinking that it may be time to take a little bit of money off the table.

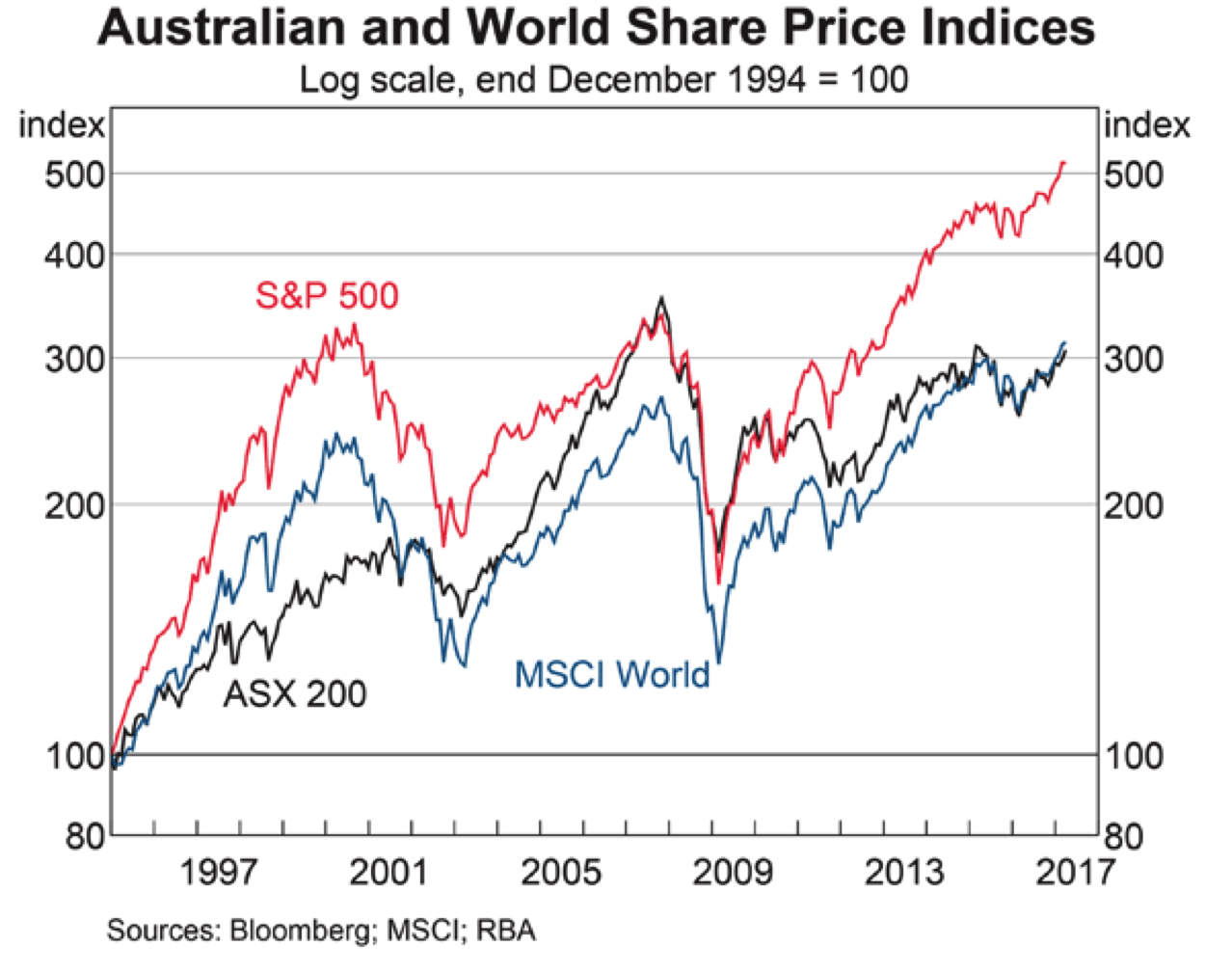

Arguably, this view doesn’t make a lot of sense, because US and major European markets keep making new highs. The correlation between the Australian sharemarket and international markets is so strong, as this graph from the Reserve Bank shows (US red, Australia black, World blue).

On the basis of this correlation, if Wall Street keeps making new highs, this has to be good for the Australian market. As the old adage goes: “let your profits run”.

But despite this “truism”, I still feel cool. Here’s why.

Big picture

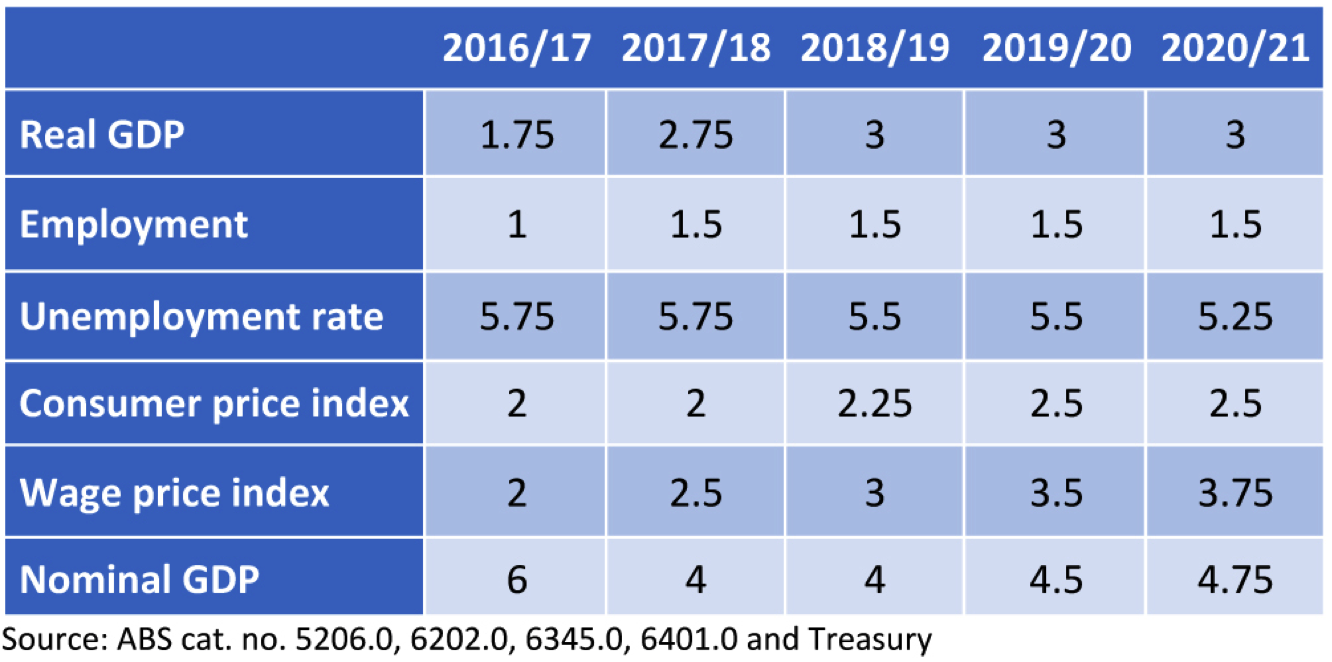

From an economic point of view, Australia looks ok. Not going gangbusters, but not falling in a real hole. If you believe the Government and the boffins at Treasury, the future looks better than okay. According to the Budget, we are set for real GDP growth of 2.75% to 3.0%, a steady unemployment rate, inflation under control, and an improving outlook for wages growth.

Budget assumptions

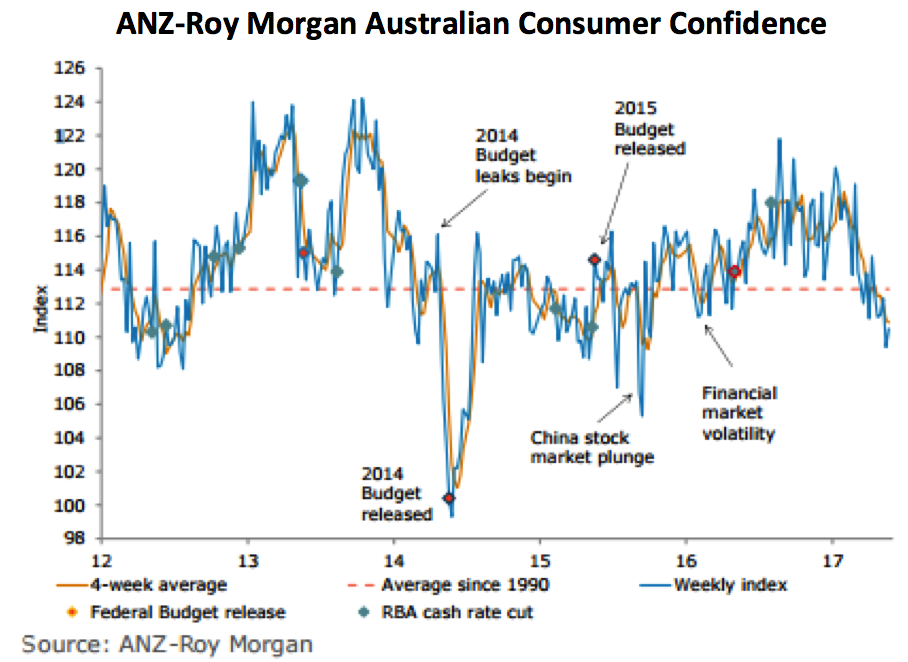

Businesses seem to agree with the Treasury. According to the latest NAB monthly survey, business conditions and business confidence remain robust. However, consumer confidence has been falling. The latest reading from ANZ-Roy Morgan has it at 110.8, below the long run average of 112.8.

ANZ-Roy Morgan Australian Consumer Confidence

Although a backward looking indicator, retail turnover has fallen for two months in a row. The fall in March of 0.1% followed a fall of 0.2% in February. Unemployment remains stubbornly around 5.7% to 6.0%, but with a growing trend towards part-time and casual jobs, and wages growth in the March quarter was just 0.5%.

On an industry level, the farming sector looks strong, while building and construction is starting to slow. The manufacturing and the resources sectors remain weak, notwithstanding that a lower Australian dollar is starting to help.

Overseas, the US economy, led by the consumer, remains solid. Europe and Japan are picking up, and most importantly for Australia, China is set to deliver economic growth (according to the Chinese Government) of around 6.8%.

In summary, the macro environment for the Australian share market and company earnings looks supportive. But it is also not likely to bring out the champagne either.

And I am not that worried about “geo-political risks” or the “black-swan” events that we don’t know about yet. So, why I am feeling a little cool?

Two reasons. Firstly, the inability to break through the 6000 level, despite the very positive leads from offshore. Secondly and most importantly, I can’t see any value in the market. I can’t see any sectors or stocks that say “buy me”.

Let me take you through my analysis – sector by sector.

Sector by sector

Financials: I wrote about the major banks two weeks ago (see here) and said that “they have had a good run and there are enough negatives to warrant a more cautious approach: indexweight”. Leaving aside the impact of the bank levy, the recent set of half-year results from ANZ, NAB and Westpac was disappointing. Negligible revenue growth, modest efforts on the cost side, pressure on interest margins, and falling return on equity.

I don’t see the second tier banks as offering any compelling value over the major banks. The insurers, fund managers or diversified financials such as Challenger could be a little more interesting, but again, they don’t scream out as “raging buys”.

Materials: How do you play BHP, Rio or Fortescue? I have to say that I have absolutely no idea about the short-term direction of the iron ore price and I would probably challenge the credibility (and track record) of anyone who says that they do. Certainly, these companies have done a lot of work to strengthen their balance sheets, improve productivity and cut production costs, and are now well positioned to benefit from any sustainable increase in the iron ore price. That’s one of the reasons they have rallied so hard.

Call me conservative, but I am indexweight on these stocks.

I don’t like the gold miners as I am not a gold bull, and the building material firms are probably a little exposed to a slowing construction market. Packaging companies such as Amcor and Orora are trading on extended multiples. In Amcor’s case, 20.0 times FY17 earnings, and 17.9 times forecast FY18 earnings.

Energy: The oil price seems to have settled into a tight trading range around US$50 per barrel. I like Woodside, but find it difficult to get too motivated about the sector.

Consumer Staples: The supermarket wars aren’t over, and the competitive threats that will hurt margins keep coming. And it is not as though either Woolworths or Wesfarmers are particularly cheap. Woolworths is trading on a multiple of 24.0 times FY17 earnings and 20.9 times FY18 earnings. Fizzy drinks manufacturer Coca Cola Amatil is facing its own headwinds.

Healthcare: I love the tailwinds that support this sector, which is one of the reasons it has done so well this year. CSL, the largest stock, is up by 31.5% in 2017, while Cochlear has added 20.4%. These stocks are now trading on very heady multiples: CSL 32.6 times FY17 earnings and 27.5 times FY18 earnings, Cochlear 38.2 times FY17 and 33.8 times FY18 earning.

Telecommunications: Telstra may have dodged a bullet when the ACCC declined to act in relation to mobile roaming, but the concern about plugging the NBN earnings hole remains. While income investors will purchase the stock for its dividend, until it can demonstrate a path to revenue growth, the stock will lag in a market upswing.

Real Estate: A sector that I am out of. I don’t like the prospects for the shopping centre or retail trusts, and feel that it is inevitable that Australian interest rates will rise as we are forced to follow the lead from the US Federal Reserve. Capitalization rates can’t fall any further.

Avoid.

Consumer Discretionary: The Amazon threat is killing the discretionary retailers (such as JB Hi-fi Harvey Norman, Myer and Super Retail) and the short sellers are active. The gambling and media industries have their own challenges. The Flight Centres, Dominos and RealEstate.coms might be ok, but it is hard to argue that they offer outstanding value.

Industrials: Probably the hardest sector to take a view on, as most of the companies aren’t really “industrials”. Defensives like Sydney Airport, Transurban and Macquarie Atlas have done really well this year as bond yields have stabilized and eased back, but now look close to fully priced. Qantas, Seek and CIMIC have performed strongly, while the largest stock by market cap in this sector, Brambles, disappointed the market with its half year result. Remains a sector to review on a “stock by stock” basis.

Bottom line

This real lack of “value” leads me to the inevitable conclusion that the Aussie market needs to cheapen first to create value again. Because it is so influenced by the direction of offshore markets, it will do this in one of two ways: it will underperform (lag) the US market as it rallies and become “relatively” cheaper, or it will just pull back by itself if the US market holds steady or eases back.

In the absence of any new information about the capacity of companies to increase earnings or an improving economic outlook, taking a little bit of money off the table and waiting is probably the low risk way to play this market

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.