In the good books

HUON AQUACULTURE GROUP LIMITED (HUO) Upgrade to Buy from Accumulate by Ord Minnett B/H/S: 2/0/0

On the back of continuing demand growth, reduced competition, and the option to export to prevent oversupply, Ord Minnett factors in higher wholesale salmon prices for Australia. This has a result of increasing estimates for the company’s operating earnings by 11% and 13% for FY17 and FY18 respectively.

Rating is upgraded to Buy from Accumulate and the target to $5.86 from $5.31. The broker makes the stock its preferred pick in the salmon sector as it has greater upside potential thanks to higher leverage to wholesale prices.

In the not-so-good books

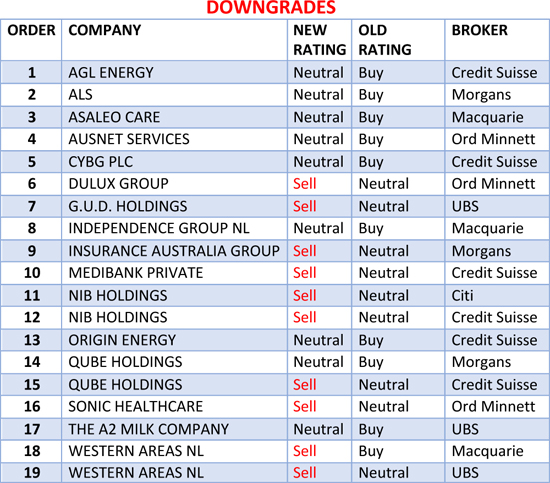

G.U.D. HOLDINGS LIMITED (GUD) Downgrade to Sell from Neutral by UBS B/H/S: 0/3/2

UBS observes since the first half result the share price has appreciated by 23%. While momentum in automotive remains encouraging, the broker downgrades to Sell from Neutral on valuation grounds.

UBS observes both Brown & Watson and Ryco are on track for double-digit growth in FY17. Meanwhile, the earnings consistency of Oates is being challenged by margin pressure on the difficulty in securing price increases in the retail segment.

The broker believes a divestment of Dexion, and potentially Oates, could provide the cash to pay down debt and be deployed into further automotive acquisitions. Target is raised to $11.30 from $10.15.

Earnings forecast

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.