The end of the financial year is just around the corner. Here are 7 actions to take before June 30.

1. Review your investment strategy

The transition from one financial year to the next is a good trigger point to review your investment strategy. Make sure it is up to date and is meeting your objectives.

If you have an SMSF, then your investment strategy should be in writing and formally approved by the Trustees. As part of any review, consider the insurance needs of your members (life, total permanent disability insurance etc.). While you are not required to take out insurance, the law requires that Trustees review whether their SMSF holds insurance cover for one or more members of the Fund.

2. Check and confirm your asset allocation

Working top down first, let’s start with your overall asset allocation. While you are not necessarily going to manage the allocation dynamically, it is not meant to be static. In the circumstances of a change to your investment objectives, a lifestyle change or your preparedness to accept risk changes, then your asset allocation will probably need to change.

Also, as your views on markets change, you may wish to review your allocation. And as the weighting is based on the market value of each asset class, the chances are that your allocation at the end of the year will be somewhat different to how you started the year.

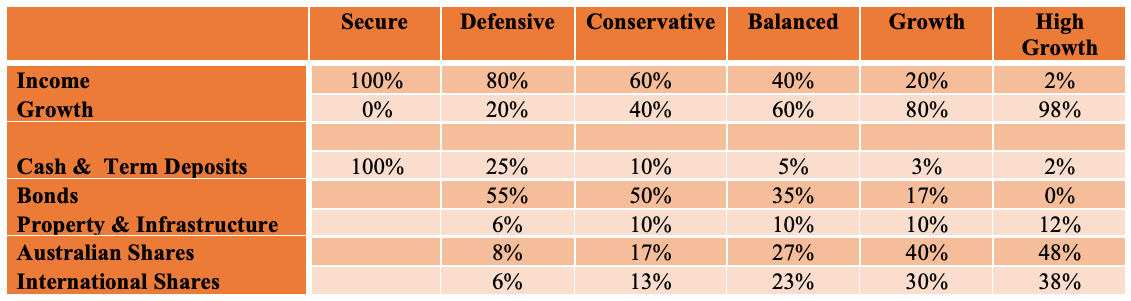

Listed below are some target asset allocations. These are categorised according to 6 common risk profiles and comprise standard assets only. Starting with the ‘Secure’ profile, income style assets are weighted at 100% and growth style assets are weighted at 0%. At the other end of the spectrum, ‘High Growth’, where income assets are weighted at 2% and growth assets are weighted at 98%.

Indicative Target Allocation by Risk Profile

Source: Switzer Financial Group

3. For stocks, check your sector allocation

Continuing the “top down” approach in relation to your share portfolio, is the balance across the sectors right?

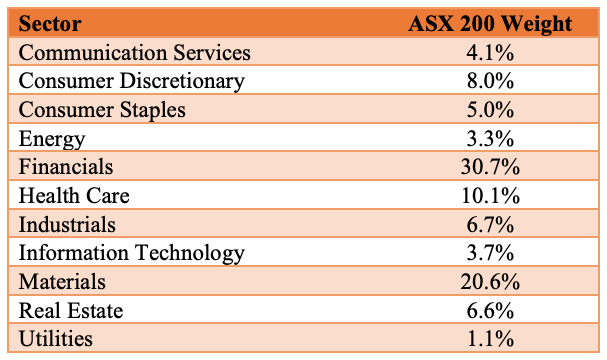

The S&P/ASX 200 is divided into 11 industry sectors, which have different weightings according to the market capitalisation of the stocks that make up that sector. Over the course of the year, the weightings change as companies join or leave the index, others raise capital, and due to changes in the share price, the market value of each company changes.

Depending on your investment objectives, you will probably target biases in some sectors where you will be overweight relative to the index, and in other sectors, underweight. For example, if your main priority is growth, you may wish to be overweight sectors such as consumer discretionary, industrials, information technology and health-care, and potentially underweight some of the defensive sectors such as utilities and property trusts.

The following table shows the sectors and current S&P/ASX 200 weights as of 31 May 2021.

Source: S&P Dow Jones

If the actual sector biases are different to how you intend them to be (your target positions), then depending on the materiality, you may want to act to address these.

4. Throw out the dogs

Next in relation to your share portfolio, do you have any dogs? The hardest part of investing is to acknowledge a mistake and cut a position. There is an old adage that goes “your first loss is your best loss”, and in my experience, this proves right (in hindsight) at least 8 out of 10 times.

In thinking about this, take into account your sector positions and mismatches away from your target position. The other factor that may influence your decision is whether you can utilise any capital loss.

For SMSFs, capital gains and losses are only relevant if the Fund is paying tax (i.e. some of the monies are in accumulation phase).

5. Capital gains tax to pay? Can you offset gains with losses?

Individuals pay tax on a gain at their marginal tax rate (potentially as high as 47%, including the 2% Medicare Levy). Where an asset has been held for more than twelve months, individuals are eligible for a 50% discount and pay tax on half the gain. There is no discount for companies.

For superannuation funds including SMSFs, if the fund is in accumulation mode, then you are liable for capital gains tax when as asset is disposed. While the nominal tax rate is only 15%, it is further reduced to 10% of the gain if the asset has been held for more than 12 months (super funds get a 1/3rd discount).

Importantly, you can offset capital gains with capital losses, and losses that cannot be used can be carried forward to the next tax year.

So, if you have taken capital gains during the year, then you may want to consider any assets in a loss situation and review whether you should continue to hold them. Of course, tax should never be the primary driver for an investment decision.

And just because you haven’t set out to sell shares on the ASX doesn’t mean you haven’t taken any gains. For example, takeovers are a disposal for CGT purposes (unless rollover relief is offered).

6. Check your super contributions and pension. Can you get the Government to help?

Can you make additional concessional contributions to super?

Concessional contributions include your employer’s 9.5%, salary sacrifice contributions and any amount you claim as a personal tax deduction. (You no longer need to be self-employed to claim the tax deduction). Your concessional contributions can’t exceed $25,000 in aggregate.

The normal age rules apply. Up to age 67, anyone can make a contribution. If you are between 67 and 74 years, you must pass the work test, which is defined as working 40 hours over any 30-day consecutive period. If you are 75 or over, only mandated employer contributions (the compulsory 9.5%) can be made..

Can you make additional personal (after tax) contributions?

The cap on non-concessional (after-tax) contributions is $100,0000. If you can access the bring forward rule, which allows you to make up to 3 years’ worth of contributions in one year, then you can potentially contribute $300,000 in one go. A couple could potentially get a combined $600,000 into super. To access the bring forward rule, you must have been aged 64 years or less on 1 July 20 and not already have accessed it in the preceding two years.

There is an important caveat to this. If your total superannuation balance is over $1,600,000, you won’t be able to make any further personal (non-concessional) contributions. Super balances are measured each June 30 (i.e. your balance on 30 June 20 determines whether you can make non-concessional contributions in 2020/21) and include all amounts in accumulation and pension. If your total super balance was between $1,400,000 and $1,500,000 then the maximum amount you can access under the bring-forward rule is $200,000, and if your balance is between $1,500,000 and $1,6000,000, you are limited to $100,000.

And don’t leave your contributions to the last minute. While there is some flexibility around the allocation of contributions to member accounts, they must be received and banked by the super fund by 30 June. This year, 30 June falls on a Wednesday y – so if making a contribution to your SMSF by cheque, or making it on behalf of a family member to an industry or retail fund by BPay, EFT or cheque, allow sufficient time for the monies to be processed and cleared. Most super funds say to allow at least two working days – so get your contributions in by Friday 25 June.

Can you access, or can a family member access, the Government Co-Contribution? If eligible, the Government will contribute up to $500 if a personal super contribution of $1,000 is made.

The Government matches a personal contribution on a 50% basis. This means that for each dollar of personal contribution, the Government makes a co-contribution of $0.50, up to an overall maximum of $500.

To be eligible, there are 3 tests. The person’s taxable income must be under $39,837 (it starts to phase out from this level, cutting out completely at $54,837), they must be under 71 at the end of the year, and critically, at least 10% of this income must be earned from an employment source.

While you may not qualify for the co-contribution, this can be a great way to boost a spouse’s super or even an adult child. For example, if your kids are university students and doing some part time work, you could potentially make a personal contribution of $1,000 on their behalf – and the Government will chip in $500!

Can you claim a tax offset for super contributions on behalf of your spouse?

If you have a spouse who earns less than $37,000 and you make a spouse super contribution of $3,000, you can claim a personal tax offset of 18% of the contribution, up to a maximum of $540. The tax offset phases out when your spouse earns $40,000 or more. Your spouse’s income includes their assessable income, reportable fringe benefits and any (though unlikely) reportable employer super contributions. One additional eligibility test – your spouse’s total super balance on 30 June 2020 was less than $1,600,000

Finally, if you are taking an account-based pension, have you been paid enough?

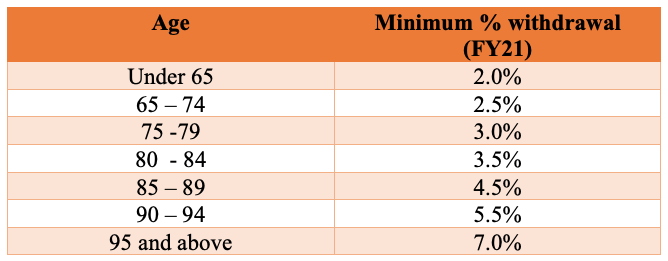

The Government requires that you take at least the minimum payment, otherwise your fund will potentially be taxed at 15% on its investment earnings rather than the special rate of 0% that applies to assets that are supporting the payment of a super pension.

The minimum payment is based on your age, and calculated on the balance of your super assets at the start of the financial year (1 July). To assist retirees following the Covid-19 pandemic, the Government reduced the minimum annual payment required by 50% for the 2020-21 financial year. The factors to apply this year are shown below.

For example, if you were aged 66 on 1 July 2020 and had a balance of $1,000,000, your minimum payment is 2.5% of $1,000,000 or $25,000. You can take your pension at any time or in any amount(s), but your aggregate drawdown over the year must exceed the minimum amount. If you commenced a pension mid-year, the minimum amount is pro-rated according to the number of days remaining until the end of the financial year.

7. Investment property? Deductions to organise?

If your own an investment property, or your SMSF has a property and the Fund is in the accumulation phase, then you should be able to claim a number of deductions. While you cannot claim capital costs (these can potentially be used to increase the cost base and reduce any subsequent capital gains tax on disposal), you can claim revenue costs and you can claim depreciation.

Revenue costs are those costs incurred in the process of earning the rental income. They include, but are not limited to:

- Advertising for a tenant;

- Loan interest and bank fees;

- Body corporate fees, rates, energy and water bills;

- Land tax;

- Cleaning, mowing, gardening, repairs and maintenance;

- Building, contents, liability and landlord’s insurance;

- Property management fees, legal fees (not relating to the actual purchase);

- Lease costs;

- Pest control;

- Quantity surveyor’s fees;

- Security patrol fees; and

- Stationery, postage and telephone.

The list goes on, and your accountant will be able to tell you what’s included as a viable property expense.

You cannot claim:

- Stamp duty on conveyancing;

- Expenses on the property not actually paid by you, such as water and electricity paid by the tenant;

- Travel expenses when inspecting the property; and

- Expenses that do not relate to the renting of the property.

Depreciation can be divided into two types —depreciation on plant and equipment (also known as Division 40 deductions) and depreciation on the building or capital works deductions (also known as Division 43 deductions).

Plant and equipment includes furniture and fixtures and fittings that are not part of the part of the building’s structure. (As a rule of thumb, if the item can be moved, then it is an item of plant and equipment, otherwise it is capital works). For properties purchased after 9 May 2017, you cannot claim depreciation on “second- hand” plant and equipment assets previously installed by another owner. You can only depreciate assets that you purchase for the property (for example, a new carpet).

Capital works deductions include the cost of the construction of the building apportioned over a 40-year period. You may need a Quantity Surveyor to assess this for you, and of course, your claim is limited to 100% of the cost of the construction. It is calculated at a rate of 2.5% of the cost of the construction.

Capital works deductions can also be claimed on in-ground swimming pools, plumbing and gas fittings, garage doors and skylights, and baths and toilets.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.