I have mixed feelings about the lockdown ending in Melbourne this week. Part of me can’t wait for life to return to something like normal and for kids to return to school on-campus.

Another part of me dreads the thought of getting back into the gym and other high-intensity sports. After months of modest activity and lost fitness, the thought of heavy-duty exercise again – and the fatigue and injuries that inevitably follow – feels daunting.

But like many in Victoria, I’ll get back into the gym when the lockdown ends. And visit my physiotherapist, dentist and other service providers. And get a haircut, too.

Talk about “reopening plays” invariably focuses on sectors such as travel and entertainment, retail or food. Less considered are personal services, such as gyms and physios. My hunch is that both sectors will be far busier in the next 12 months than the market realises.

Consider gyms. I don’t buy the argument that fewer people will have gym memberships after the pandemic. Yes, there’ll be an initial drop-off because of lapsed memberships. A low proportion of people might deem gyms are too enclosed and prone to Covid spreading.

That hasn’t been the case in the United States. Reports I’ve read suggest gym membership sign-ups this year (particularly in the busy summer period) have matched those in previous years. In some cases, gym membership sign-ups have exceeded prior years.

Pre-Covid, my gym was full of teenagers and twenty-somethings at night who spent more time talking to friends and checking their phones than exercising. For them, a gym membership is also about exercising with friends and social interaction. That’s healthy.

I believe gyms could do well out of Covid, after the initial shock of having to close their facilities. The pandemic has sparked new interest in online fitness classes. US reports suggest gyms there are increasingly “pivoting” their business model to provide a mix of in-gym and virtual classes.

Potentially, that exposes the gym to a much larger market than it could accommodate with its gym facilities, but also more competition. Forward-looking gyms will translate this newfound interest in online exercise to new business models and revenue streams.

Physiotherapy is another interesting market after Covid. Heaven knows there will be plenty of injuries as people get back into exercise and thus a rise in demand for physio (I’ll be one of them!).

Longer-term, the physiotherapy market has attractive growth prospects as an ageing population demands more health services. It’s no stretch to believe an older population that is more active and exercising later in life than previous generations will boost physio demand.

As in the fitness industry, cashed-up physiotherapy chains should have more opportunities to acquire businesses at better prices after the pandemic. Industry consolidators could pounce on acquisition opportunities as small players crushed by Covid exit their industry.

Sadly, there isn’t much choice in fitness or physiotherapy stocks on the ASX. Among the few available, two are Viva Leisure and Healthia. As small-cap companies, both suit experienced investors who understand the features, benefits and risks of this form of investing.

Here is a snapshot of their prospects:

1. Viva Leisure (VVA)

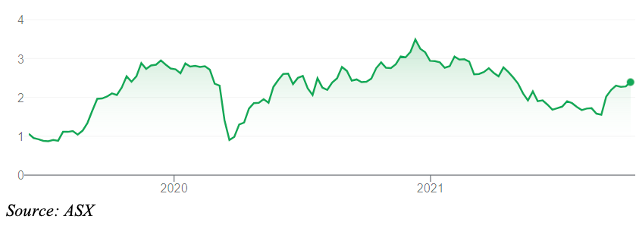

The gym owner listed on the ASX in June 2019 through an Initial Public Offering valuing it at $52.6 million at the $1 offer price. Viva is now $2.26.

It’s been a bumpy ride. Viva soared to almost $3 within six months of listing, then sank to 90 cents during the global equities crash in March 2020. With gyms forced to close, and Covid uncertainty gripping the world, Viva was an obvious stock for fund managers to sell.

Viva was back above $3 by late 2020, then drifted lower. The Canberra-based company has started to rally again as the market looks to lockdowns ending in NSW, Victoria and the Australian Capital Territory – and a recovery in gym memberships.

Viva is expanding quickly. It had 310 locations in August 2021 through a mix of company-owned and franchised gyms. Total membership was about 290,000 people. Viva’s Plus Fitness brand opened its 200th location this month.

Like other gyms, Viva was hit hard by Covid. In August, Viva said 92 of its company-owned locations were not operating because of Covid lockdowns. The flip side is that Viva has a lot of gyms to come back online when Covid restrictions finally ease nationwide.

My main concern is the risk of franchise disputes. I’ve seen too many companies over the years grow rapidly by buying franchising networks and selling franchises to prospective business owners. Bitter franchising disputes that play out in the media have almost killed some companies that have grown too quickly through industry consolidation and “roll-ups”.

Viva is in dispute with a number of Plus Fitness franchisees (Viva became master franchisor of Plus Fitness in August 2020). It looks like an ugly fight, judging by newspaper reports, and something prospective investors should watch closely.

But in its 2021 Annual Report, Viva said it is confident it is dealing with franchising “appropriately and within the law” and has not made provision for a potential claim from disgruntled franchisees. I’ve heard other franchisors say the same over the years.

Still, I like Viva’s business model, execution and long-term prospects for the gym industry. Having raised capital through its IPO and placement, Viva is well-placed to acquire businesses and expand rapidly through organic growth via franchising and new company-owned stores.

Share-price gains might be slower from here, but Viva should have strong tailwinds in the next few years as more Australians get back into fitness after the pandemic.

Chart 1: Viva Leisure (VVA)

2. Healthia (HLA)

Healthia listed on the ASX through an IPO in September 2018 that valued it at $63 million at the $1 offer price. Healthia is now $1.94, having been as high as $2.20.

Healthia was formed to bring together allied health brands, including My FootDr Podiatry and Allsports Physiotherapy. A step-change in the company’s growth came in September 2020 when it acquired the physiotherapy chain Back in Motion and sought to raise $60 million.

Healthia says the Back in Motion acquisition, which settled this month, positions it as the largest provider of physio services in Australia with 122 clinics. Healthia says Back in Motion will add $62.9 million to its revenue and is earnings accretive (12% earnings-per-share growth in FY21).

Healthia paid $88.4 million for Back in Motion’s business and 64 physiotherapy clinics. Back in Motion is one of Australia’s largest and fastest-growing physio networks, said Healthia.

It looks like a good deal. Healthia paid an underlying (EBITDA) multiple of 7.1 times for Back in Motion. That seems reasonable given Back in Motion’s network, growth and prospects.

The deal takes Healthia into a new league. Now capitalised at $246 million, Healthia should start to attract more small-cap fund managers as its stock liquidity increases.

Back in Motion founder Jason Smith will act as a strategic consultant to Healthia and is a shareholder in that company. The deal also has $4.2 million in clinics earnouts if certain performance targets are met. That’s a good sign because small-caps can come unstuck after making their first big acquisition, which always sounds good on paper.

Investors should take extra care with small-cap companies that raise money to rapidly acquire other businesses and “roll up” their industry. The prospect of “consolidating a fragmented industry” makes for a strong sales pitch but has burnt many investors in years past.

That said, the physiotherapy industry is fragmented. Unlike other sectors, such as dentistry or veterinary care, there has not been nearly as much IPO or private-equity activity in the space.

Healthia has recognised the opportunity, raised plenty of cash and has so far made a good impression as a listed company. It’s a stock to watch over the next few years.

Chart 2: Healthia (HLA)

Tony Featherstone is a former managing editor of BRW, Shares and Personal Investor magazines. The information in this article should not be considered personal advice. It has been prepared without considering your objectives, financial situation or needs. Before acting on information in this article consider its appropriateness and accuracy, regarding your objectives, financial situation and needs. Do further research of your own and/or seek personal financial advice from a licensed adviser before making any financial or investment decisions based on this article. All prices and analysis at 20 October 2021.