The ping pong match between the Presidents of the USA and China got serious overnight with the Fed ‘umpire’ Jay Powell having little impact on a game that’s getting out of hand!

The day kicked off with China announcing a series of tariff responses on $US75 billion worth of US goods, which includes cars. They’ll come in batches, some starting September 1 and others December 15, which looks like retaliation return of serves for the tariffs that Donald Trump announced, which affect $US300 billion worth of Chinese goods.

These too will have similarly staggered starting points. This Chinese action was step one in the escalation of the trade war overnight, made worse by a series of Trump tweets, which the stock market didn’t like. At the close, the Dow was down 623 points (or 2.37%) to 25,628.9. We need to get ready for a bad day for stocks locally on Monday.

This rough CNBC shot (off my TV at 5am) shows it all:

China’s retaliation, followed by little positivity from the Fed boss Powell and then the Trump tweets! Let me show you some of these:

“Our Country has lost, stupidly, Trillions of Dollars with China over many years. They have stolen our Intellectual Property at a rate of Hundreds of Billions of Dollars a year, & they want to continue. I won’t let that happen! We don’t need China and, frankly, would be far…

But wait there’s more…

“…better off without them. The vast amounts of money made and stolen by China from the United States, year after year, for decades, will and must STOP. Our great American companies are hereby ordered to immediately start looking for an alternative to China, including bringing…”

If you weren’t sure what a trade war escalation looks like, well now you are. I suspect it will get worse before it gets better.

And it did get worse, with the Powell speech not strongly saying that a rate cut would be used to offset the trade threats to the economy. The market needed more than this from Powell: “Our challenge now is to do what monetary policy can do to sustain the expansion so that the benefits of the strong jobs market extend to more of those still left behind, and so that inflation is centred firmly around 2 percent.”

This speech from Jackson Hole, Wyoming, didn’t cut it, with China and the US trading trade blows from Beijing to Washington having a bigger market effect!

Not surprisingly, the yield curve inverted and the efforts of Donald, Xi and Jerome did a lot to make that happen. Well done, team!

Rate cuts are coming and we’re bound to see them in September in the US. And if this trade stoush goes from bad to worse, which looks likely, our RBA could cut before Cup Day.

These tweets from Trump about Powell show that we’re in for some tough times on the market next week:

“As usual, the Fed did NOTHING! It is incredible that they can “speak” without knowing or asking what I am doing, which will be announced shortly. We have a very strong dollar and a very weak Fed. I will work “brilliantly” with both, and the U.S. will do great…”

And then he threw this killer in:

“My only question is, who is our bigger enemy, Jay Powell or Chairman Xi?”

Companies such as Ford, GM, John Deere, Caterpillar, 3M, Goldman Sachs and IBM were all clobbered and took the Dow down big time.

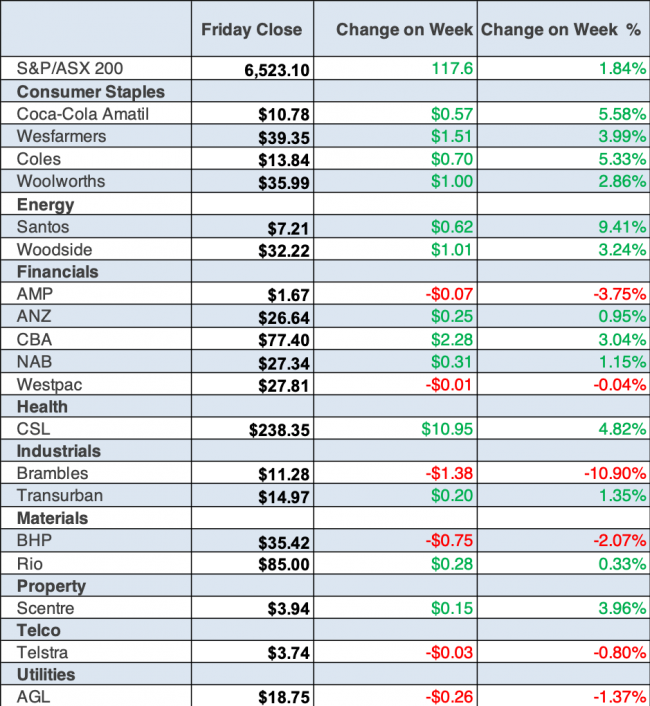

On the local front, we didn’t need this ping pong play, with shares up 117.6 points (or 1.8%), with the S&P/ASX 200 finishing at 6523.1 for the week. And it has been so good to see that earnings season hasn’t been a disappointment as some experts were predicting.

I’m not saying it has been great but it hasn’t been a shocker.

This is AMP’s Shane Oliver’s take on earnings season so far:

- The Australian June-half reporting season is now around 75% done in terms of companies and about 85% done by market cap and it’s been relatively soft.

- Only 37% of results have surprised on the upside, which is below the long-term norm of 44% and is the lowest since 2012.

- 61% have seen earnings rise from a year ago but this time last year it was 77%.

- 53% of companies have raised their dividends but this compares to 77% doing so a year ago. 25% have cut their dividends, which is the highest in the last seven years, suggesting greater caution. Downgrades have dominated upgrades, with 2018-19 consensus earnings growth expectations cut to 1.5% from around 2% at the start of August.

- While consensus earnings expectations are for a pick-up in earnings growth to 7.5% this financial year, the slowdown in economic growth, cautious outlook statements and falling commodity prices suggest some downside risk to this.

Good news came from Lend Lease, up 23%, as it called an end to the residential downturn crisis. Goodman Group was up 6.2% after a solid report and McMillan Shakespeare was the huge winner, up 30.6% for the week! Wisetech rose 24.5%, Smartgroup 20.14% while Altium put on 12.7%.

Losers included A2 Milk, down 8.3%, despite a good profit surge, South 32 gave up 10.9% but other miners did a lot worse. Pilbara Minerals lost 16.3%, St Barbara shed 15.16%, while Saracen was down 11.25%.

Good news for those of you who’ve been going for gold for a long time or those who took my ETF tip a few weeks back, with RBC Capital tipping more gold price spikes. The spot price is around $US1,506 but RBC can’t support those who think it will go to $US2,000. That said, there’s still a lot of room to go higher!

What I liked

- In trend terms, the Internet Vacancy Index rose by 0.4% in July – the first rise in seven months. Record vacancies exist for health and education workers.

- The estimate of family finances compared with a year ago was up from +10.1 points to +10.3 points. And the estimate of family finances over the next year was up from +27.7 points to 28.5 points.

- The US leading index rose by 0.5% in July (forecast +0.2%).

- Minutes of the last US Federal Open Market Committee meeting show that members debated a larger rate cut of 50 basis points but decided on a 25 basis point rate cut, as they wanted it to be seen as a recalibration of the policy stance or a mid-cycle adjustment.

- President Trump is also considering a cut in payroll taxes.

- The German Chancellor said that a solution to the Irish border issue could be found before the October 31 Brexit deadline.

- The Italian share market posted a big 1.8% increase on Thursday on hopes that a new coalition government may be formed.

- German Finance Minister Olaf Scholz reinforced hopes of easier fiscal policy, saying that the country possessed the fiscal strength to counter any future economic crisis “with full force”.

What I didn’t like

- The weekly ANZ-Roy Morgan consumer confidence rating fell by 2.3% to 112.8 points. Consumer sentiment is now below the average of 114.5 points held since 2014 and the longer-term average of 113.1 points since 1990.

- Economy-wide spending remained soft into July. The Commonwealth Bank Business Sales Indicator (BSI) fell by 0.1% in July after a similar decline in June. Spending has softened over the past five months and is below the 0.4% long-term average monthly growth pace.

- According to the Australian Institute of Petroleum, the national average price of unleaded petrol rose by 4.9 cents in the past week to 142.8 cents a litre. The metropolitan price rose by 7 cents to 143.6 cents a litre and the regional price rose by 0.8 cents to 141.3 cents a litre.

- The ‘flash’ purchasing managers index for manufacturing in the US fell from 50.4 to 49.9 in August (forecast 50.5), with services down from 53 to 50.9 (forecast 52.8).

- The European Union rejected calls by UK Prime Minister Boris Johnson to re-open Brexit negotiations.

Growth expected

The RBA minutes, released this week, said: “The forecast for GDP growth over 2019 had been lowered to 2½ per cent. Growth was expected to pick up to 2¾ per cent over 2020 and to around 3 per cent over 2021. This was supported by a range of factors, including lower interest rates, tax measures, signs of an earlier-than-expected stabilisation in some established housing markets, the lower exchange rate, the infrastructure pipeline and a pick-up in activity in the mining sector.”

And this table from Morgan’s Michael Knox says our economy is set to grow faster than the US, the EU and Japan, and I bet we beat the UK!

Gotta hope this trade war ping pong match doesn’t make these numbers wrong.

My new book ‘Join the Rich Club’ is now available for purchase through the Switzer Store website [1].

The week in review:

- Two recent events have encouraged me to solidly get behind the idea of buying banks. These will be the stocks that will spike [2] if a trade deal comes and recession fears abate.

- Paul Rickard wrote this week that Telstra is probably better than its competitors and the company under Andy Penn’s leadership is trying hard. But how far is there to go to make up for the havoc the NBN is reeking on this telco? [3]

- Trying to time a downturn is essentially a futile exercise and the temptation to look at daily, weekly or monthly performance can be a guaranteed way to make poor investment decisions. In his latest article, Charlie Aitken explained the steps and actions he takes [4] to address perceived risks and take advantage of any short-term volatility.

- The search for yield can identify some attractive alternative situations, where there’s potential for healthy yields and – just maybe – the bonus of share price gain. The cut and thrust of profit reporting season always throws up candidates of this kind: here are four that James Dunn has noticed [5].

- Buying shares in discretionary fashion retailers is as contrarian as it gets in this market, even though some are performing well and others are undervalued. To Tony Featherstone, City Chic Collective and Noni B stand out [6].

- FNArena registered 24 upgrades for individual ASX-listed stocks against 13 downgrades in the first Buy, Hold, Sell – What the Brokers Say [7] this week, while 14 stocks were downgraded and 13 upgraded in the second edition [8].

- We had two Hot Stocks this week [9], with CMC Markets’ Chief Market Strategist Michael McCarthy highlighting BlueScope Steel and Burman Invest Portfolio Manager Julia Lee selecting Baby Bunting.

- In Questions of the Week [10], Paul Rickard answered queries about share purchase plans for Transurban, AMP, and what would happen if Governments run up deficits to increase spending on infrastructure.

Top Stocks – how they fared:

The Week Ahead:

Australia

Sunday August 25 – Speech by Reserve Bank Governor

Tuesday August 27 – Speech by Reserve Bank official

Tuesday August 27 – CBA Household Spending Intentions (July)

Wednesday August 28 – Construction work done (June quarter)

Thursday August 29 – Business investment (June quarter)

Friday August 30 – Building approvals (July)

Friday August 30 – Private sector credit (July)

Friday August 30 – APRA bank statistics (July)

Overseas

Monday August 26 – US Durable goods orders (July)

Tuesday August 27 – China Industrial profits (July, annual)

Tuesday August 27 – US House Price Indexes (June)

Tuesday August 27 – US Consumer Confidence (August)

Tuesday August 27 – US Richmond Fed manufacturing (August)

Thursday August 29 – US Economic growth (June quarter)

Thursday August 29 – US Goods trade balance (July)

Thursday August 29 – US Pending home sales (July)

Friday August 30 – US Personal income/spending (July)

Saturday August 31 – China purchasing manager indexes (August)

Food for thought:

“This company looks cheap, that company looks cheap, but the overall economy could completely screw it up. The key is to wait. Sometimes the hardest thing to do is to do nothing.” – David Tepper

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

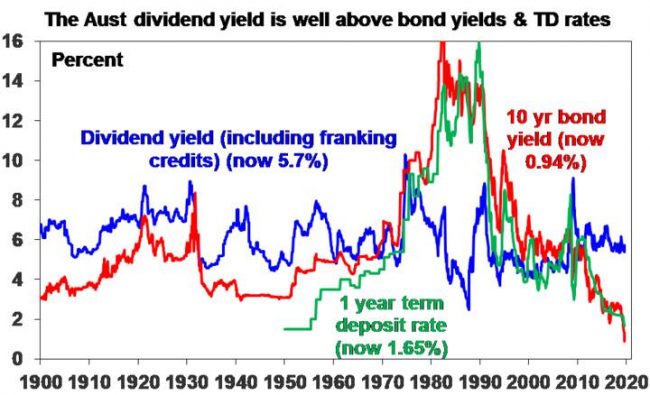

Chart of the week:

AMP Capital’s chief economist Shane Oliver this week highlighted that the gap between the grossed-up dividend yield on Australian shares (5.7%) and the Australian 10-year bond yield (0.94%) has reached a record high of 4.8%:

Source: Global Financial Data, Bloomberg, AMP Capital

Top 5 most clicked:

- Are banks a good buy or a good-bye? [2] – Peter Switzer

- Don’t be spooked by short-term volatility. Take advantage of it [4]. – Charlie Aitken

- 4 yield stocks (maybe a share price gain too) [5] – James Dunn

- Telstra: put it on hold for now? [3] – Paul Rickard

- Buy, Hold, Sell – What the Brokers Say [7] – Rudi Filapek-Vandyck

Recent Switzer Reports:

Monday 19 August: Big banks + Telstra [11]

Thursday 22 August: Take advantage of short-term volatility! [12]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.