A reader recently asked for suggestions on stocks exposed to inbound tourism. It’s a fair question. The boom in Asian tourists to Australia is a ripper. And it’s only getting started as millions of people in developing nations join the middle-class.

I have written on this trend several times for the Switzer Super Report over the past three years, preferring stocks such as Sydney Airport, Qantas Airways, The Star Entertainment Group, Mantra Group and small cruise company, SeaLink Travel Group.

For the most part, these stocks were suggested for their capital-growth prospects and each delivered. I went a little cold on Sydney Airport and SeaLink in 2016 on valuations grounds alone, after almighty share-price rallies.

But the Switzer reader seeks income stocks for his Self-Managed Superannuation Fund and is in pension mode. He will not find many stocks exposed to inbound Asian tourism that offer consistently attractive, reliable, fully franked dividend yield.

Qantas Airways is an example. I highlighted the stock for readers in June 2016 around $2.50. Qantas has since recovered to $4.92, amid improving operating performance and earnings. However, Qantas now looks fully valued and a forecast yield of about 3% is too low for income investors.

The same is true of The Star Entertainment Group. I wrote favourably about The Star (then called Echo Entertainment Group) in August 2015 for this report at $5.10 a share. It is still okay value for long-term investors given its growth prospects in South-East Queensland, but a forecast dividend yield below 3% is too low for income seekers.

Nevertheless, there are yield opportunities in tourism-related stocks if investors look hard enough and are prepared to own stocks that can have higher volatility.

International visitors to Australia rose 11% to 7.6 million in 2016, shows Tourism Research Australia data. They spent $39.1 billion.

Chinese tourists rose 17% to 1.1 million, continuing a period of remarkable growth. Japanese tourists leapt 24%. With another 2 billion Asians expected to join the middle-class by 2030 on OECD forecasts, growth in inbound Australian tourism is a good bet.

My hunch is this trend will be bigger than expected. Percentage gains in international visitors impress, but Australia has only scratched the potential of Asian tourism. Lots of people there want to visit our shores; the potential is converting those intentions into tourism dollars.

Here are three tourism-related stocks that offer a mix of yield and capital growth:

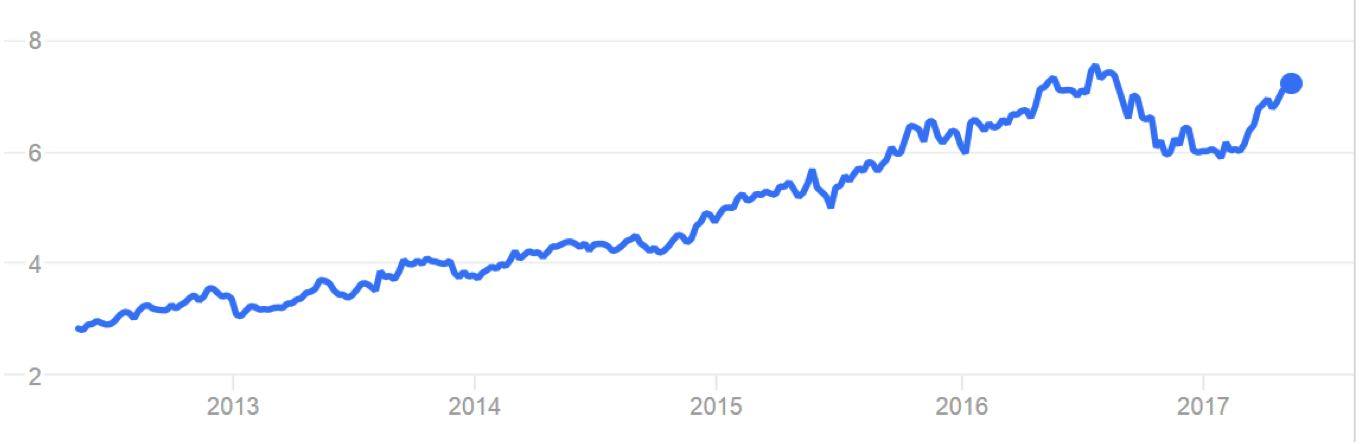

1. Sydney Airport (SYD)

The airport owner was among my top stock ideas for the past five years. It owns a fabulous monopoly asset (for a long time yet) in Sydney and is superbly leveraged to growth in Asian tourism. Sydney is the priority destination for international visitors.

Sydney Airport rallied as investors pounced on interest-rate-sensitive stocks, such as infrastructure assets with reliable yield. The stock almost doubled from 2014 to 2016.

I suggested taking profits on Sydney Airport in this report in May 2016, at $7.50 a share. It peaked at $7.62 then tumbled below $6 this year as investors rotated into cyclical growth stocks. The stock has since rallied to $7.62.

I have become more comfortable with Sydney Airport as it becomes clearer that the proposed Western Sydney Airport will be a minimal long-term threat.

International evidence shows airports in prime locations have significant competitive advantages over satellite ones that are hard to break.

Western Sydney Airport, as a Commonwealth government-developed asset, could be a less aggressive challenger to Sydney Airport, which should continue to enjoy airline-traffic stability.

The market may have over-reacted to the threat of Western Sydney Airport and overlooked the incumbent’s airport’s growth potential.

Granted, Sydney Airport looks fully valued at the current price and its high debt is always a complication. But long-term income investors seeking a mix of capital growth and yield could do worse than invest in an asset that will enjoy monopoly status for a long time yet.

Sydney Airport’s forecast yield is about 5%, using consensus forecasts.

Chart 1: Sydney Airport

[1]

[1]Source: ASX

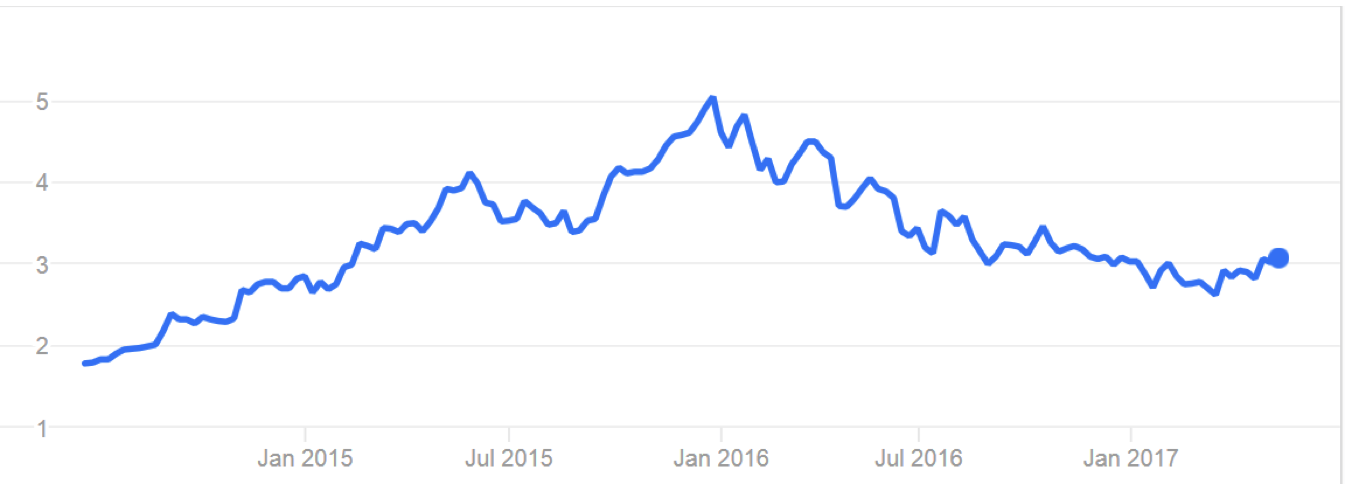

2. Mantra Group (MTR)

Investors could not get enough of the fast-growing accommodation group when it listed on ASX in June 2015 through a $239 million initial public offering (IPO). The $1.80 issued shares soared above $5 in late 2015, making Mantra among the best IPOs in years.

The stock has since fallen to $3.08 amid lingering concerns about Airbnb’s potential to disrupt the Australian hotel sector and crunch Mantra’s earnings.

Those concerns are overdone. Airbnb’s share of city room supply in Sydney and Melbourne is estimated to be at or below 4% by some brokers. Its share will grow, but not by enough to threaten Mantra’s business model and industry position anytime soon.

To recap, Mantra is Australia’s second-largest accommodation provider, serving two million guests annually through more than 100 Peppers, Mantra and Breakfree hotels.

It is an obvious beneficiary of growth in inbound Asian tourists seeking accommodation directly or through tours. Many tourists often favour four-star hotel chains from reputable brands (such as Mantra). Can’t see too many Asians tourists using Airbnb for their first overseas holiday here.

Airbnb is a formidable competitor and serious long-term threat to the global hotel industry. But there is not a huge price difference between Airbnb and average hotel charges; many choose Airbnb for the experience of staying with residents as much as the cost savings.

At $3.02, Mantra is on a forecast Price Earnings (PE) multiple of about 15 times FY18 earnings and at a significant discount to the aggregate valuation of its global hotel peers. A forecast yield of around 5% is handy given Mantra’s medium-term growth prospects.

As the market obsesses about Airbnb, it is easy to overlook Mantra’s potential to open more hotels and upgrade others — and fill them with Asian tourists, locals and business travellers. Mantra’s high customer-satisfaction ratings are the best defence against Airbnb.

Chart 2: Mantra

[2]

[2]Source: ASX

3. Crown Resorts (CWN)

The casino operator has had a hellish 12 months; the arrest of multiple employees in China and weakness in high-roller volumes at its Asian casinos headlining a long list of problems. Crown has fallen from a 52-week high of $14.06 to $12.84. The stock traded above $17 in 2014.

For all the problems, Crown has attractive assets in its Melbourne and Perth casinos. Both have resilient earnings, long-dated licences and privileged positions as sole casino operators. The Perth casino’s redevelopment, the completion of an adjacent new sporting stadium for 2018 and an eventual upturn in Western Australia will help casino earnings.

The Crown Sydney development at Barangaroo on the CBD’s western fringe, is due by 2021. The $2 billion development will transform the city’s current one-casino-operator industry and is expected to snare a large slice of high-roller gamblers and premium patrons from The Star.

Less considered is Crown’s potential to cross-sell its Melbourne and Sydney casino resorts to VIPs and other international tourists. Australia has a tiny share of the global VIP market, so there is upside to lure more gambling “whales” with a two-casino offer.

Crown has divested most of its international projects, de-risking the company by reducing exposure to more volatile Asian gambling markets. That fortifies the balance sheet and creates greater focus on the Sydney casino, a potential goldmine.

Crown does not suit conservative income investors. It has had asset restructures, problems in China and lingering weakness in VIP activity. The Sydney casino is still years away from opening and market sentiment is against Crown.

But the stock is superbly leveraged to inbound Asian tourists, many of whom love to gamble and stay at integrated casino resorts. Owning flagship casinos in Sydney and Melbourne will give Crown a formidable local advantage and improve Australia’s global competitiveness in casinos.

At $12.84, Crown trades on a forecast of about 21 times FY18 earnings, consensus estimates show. Morningstar values the stock at $13.50; Macquarie values it at $13.30. The forecast FY18 dividend yield is almost 5% based on consensus forecasts.

Chart 3: Crown

[3]

[3]Source: ASX

Tony Featherstone is a former managing editor of BRW and Shares magazines. All prices and analysis at May 17, 2017.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.