Investors in Australia’s biggest Listed Investment Companies (LICs) have witnessed mixed fortunes over the last 12 months. While on paper an annual return in the range of 12.7% to 13.1% looks pretty commendable, this masks the fact that they have underperformed the benchmark S&P/ASX 200 accumulation index by 2.3% to 2.7% over this period. And if share price performance is considered (growth in share price plus dividends), they have fared even worse as the premium to NTA (net tangible asset value) has evaporated. The second largest, Argo (ASX: ARG), has returned only 7.2% on this measure over the 12 months to 31 August.

Part of the reason for the underperformance of the major LICs is that they tend to invest in the major cap stocks, and the top part of the market has underperformed relative to the mid and small caps. Many of our major companies (the major banks, retailers, insurance companies, telcos, etc) are somewhat “growthless” and are struggling to increase shareholder returns.

This is reflected in the return of the S&P/ASX 20, which is 13.86% for the 12 months to August, 1.54% below the return of the S&P/ASX 200 of 15.40%.

As the following table makes clear, the top part of the market has underperformed over the last few years. Interestingly, it’s almost a reversal of what happened over the first half of the decade, when the market was led by the major stocks. On a 10-year basis, the top 20 stocks have marginally outperformed the S&P/ASX 200, while underperforming on a 1-year, 3-year and 5-year basis.

The ”stars” have been the mid-cap stocks. The midcap 50 index, which tracks stocks ranked 51st to 100th by market capitalisation, has returned 18.17% per annum over the three years.

Total Returns to 31 August 2018

[1]

[1]

Shareholder returns in LICs have been further diminished by the closing of the premium to NTA. And it is this discussion of premiums, or a discount, which leads me to address one of the most frequently asked questions by investors: what is the best managed investment?

While many investors prefer to construct their own portfolio of direct shares, others see the advantages of using a managed investment – particularly if they don’t have a lot of time to follow the market. Some investors use managers to complement a portfolio of direct shares, while others go the opposite way and run a core portfolio with a manager and then invest in individual shares as the satellite component.

Two of the easier ways to gain exposure to the market are through broad based LICs or index tracking Exchange Traded Funds (ETFs). Listed and traded on the ASX, both are managed investments. There are also many other managed investments (ETFs and LICs) that specialise in components of the market (such as mid caps or small caps), sectors, or investment styles (e.g. deep value). And of course there is the Switzer Dividend Growth Fund (ASX: SWTZ), which because I am conflicted, I will exclude from this discussion.

But I propose to stick to funds that offer broad market exposure and address the question: what is the best managed fund? I answer this by saying it largely comes down to the premium or discount.

Exchange traded funds (ETFs)

Most ETFs are designed to track an index. They are on “autopilot” – the manager invests and maintains the investment in accordance with the index. If the index weight for Commonwealth Bank is 7.5%, very close to 7.5% of the ETF will be invested in Commonwealth Bank shares. The manager doesn’t try to beat the market – all he/she does is to try to reduce the index tracking error.

With their low management fees, they should provide a return that closely matches the return of the index. Nothing more, nothing less.

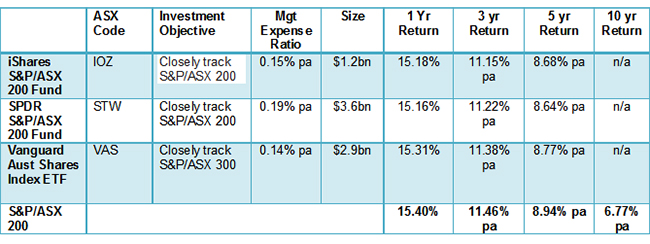

The major market cap ETFs are set out below. They track broad-based indices, with both IOZ and STW tracking the S&P/ASX 200 (IOZ from 1 December 2015), while VAS tracks the broader S&P/ASX 300. Fees are very competitive.

Performances to 31 August 2018 (after fees) are shown below, as is the benchmark S&P/ASX 200 accumulation index.

Major ETFs

[2]

[2]Returns to 31/8/18. Source: Respective Managers

The advantages of an ETF over a LIC are improved transparency and market pricing. ETFs update their NTA every working day, sometimes intraday, and due to their fungibility (the ability of an asset to be interchanged with other assets of the same type) and appointment of market makers, you can buy or sell an ETF within 0.10%/0.20% of the NTA of the fund. The premium or discount should always be small. Unlike LICs, they don’t offer share purchase plans.

Each of the major ETFs pays distributions on a quarterly basis.

The major LICs

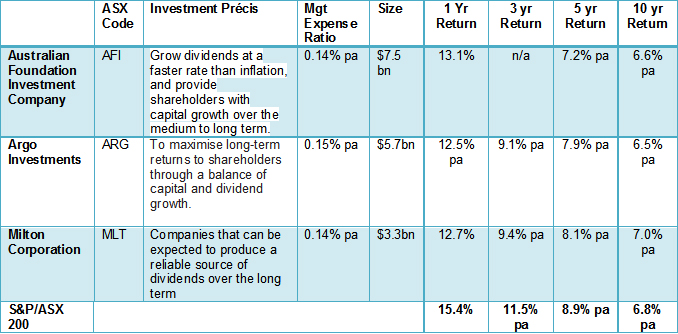

There are three major broad market LICs – AFIC or Australian Foundation Investment Company (AFI), Argo Investments (ARG) and Milton Corporation (MLT). They are big, professionally managed and very credible investment companies. Milton Corporation, for example, was listed on the ASX in 1958 and has paid a dividend to its shareholders every year since.

LICs are actively managed. That said, these broad market LICs essentially invest in the major blue chip companies, placing considerable emphasis on companies that have reliable earnings, pay fully-franked dividends and have an ability to grow these dividends. An investment précis is set out in the table below.

As the table demonstrates, the funds have largely matched the performance of the S&P/ASX 200 accumulation index over 10 years, but underperformed in more recent time periods. Milton Corporation, the smallest in size at just under $3.3 billion, boasts the best performance over three years, five years and 10 years.

Interestingly, one of Argo’s largest investments at 31 August (1.6% of its funds) was in rival Milton Corporation. It also has a sizable investment in another LIC, Australian United Investment Company (AUI).

Major LICs

[3]

[3]Returns to 31/8/2018. Source: Respective Managers

An advantage of LICs compared to ETFs is that they usually offer share purchase plans, which allow shareholders to subscribe for new shares at a marginal discount to their underlying value or NTA (Net Tangible Asset value). Dividends, whilst generally higher, are only paid twice a year (compared to the quarterly distribution cycle offered by ETFs).

A major disadvantage is that as close-ended funds, where new investors become investors by buying shares from other investors on the ASX, the LIC can at times trade at a significant premium or discount to its NTA.

LIC or ETF?

The tables demonstrate that despite their different investment styles, objectives and benchmarks, the broad market LICs can be expected to deliver an index style return plus or minus a bit, and the ETFs an index return less a fraction. While this is not a “given”, the outcome is not that surprising, given the concentrated nature of the domestic share market and the relatively conservative investment style adopted by the LICs.

So, the answer to the question: LIC or ETF? comes down to the premium or discount that the LIC is trading at.

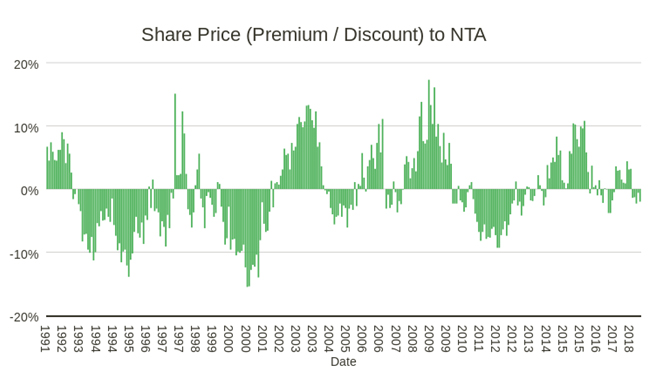

The graph below shows Argo’s share price compared to the underlying NTA. At times, it has traded at a discount of up to 15% and at other times a premium as high as 17%. More recently, this range has narrowed to around 5% either way.

Argo’s share price to NTA – relative premium/discount

[4]

[4]Source: Argo

Over the last 12 months, the LICs have moved from trading at a small premium to trading at a small discount. At the end of August, each of the major LICs was trading at a discount ranging from 0.8% for AFIC to 3.5% for Milton.

Discount/premium (as at 31 August 2018)

[5]

[5]*NTA sourced from Company Reports

With the ASX off almost 2% in September (1.96% on a total return basis), the discount has narrowed. We estimate that AFIC closed at a small premium on Friday, while Milton’s discount was back to 2.7%.

Estimated Discount/Premium (as at 14 September 2018)

[6]

[6]*NTA estimated by Switzer Report, based on reported 31 August NTA adjusted for the movement in the S&P/ASX 200 Accumulation Index

While LICs can point to relatively strong performance in the first half of the decade, their recent underperformance suggests the assumption that the return will be around index may be difficult to sustain long term, and that a safer assumption for long-term performance may be “index minus a bit”. For ETFs, we can be confident that the return will be index less the management fee – nothing more, and nothing less.

So, my rule of thumb is:

If the LIC is trading at discount of at least 2%, then invest in the LIC,

otherwise, invest in the ETF.

While there is arguably a little more variability in the return from the LIC than the ETF (because the former is actively managed), the flipside is that its return may indeed be better than the index return. There is also some manager risk – so you may want to spread any investment across two LICs.

Calculating the premium or discount

LICs are required to publish their NTA each month (via an ASX announcement, plus on their website), which is generally available by the fifth working day of the following month.

At other times, you can quite accurately estimate the NTAs for the broad market LICs. Take the last published NTA, and adjust it up or down by the percentage movement in the S&P/ASX 200 since the calculation date (i.e. end of month). To calculate the premium or discount, compare the estimated NTA with the current market price on the ASX (see table above for 14 September 2018).

Which one?

My ranking of the ETFs (based on management fees and index tracked) is:

- VAS (Vanguard)

- IOZ (iShares)

- STW (SPDR)

There is very little in this assessment – any of these ETFs could be selected. It is heavily influenced by fee and a longer term view that smaller companies will in time do better and hence a preference to opt for a broader index (the S&P/ASX 300 rather than the S&P/ASX 200).

With the LICs, Milton Corporation has the best performance record over three years, five years and 10 years and has the biggest discount. It gets the gong. In a tight race for second, I can’t really split the other two. If investing, I would buy whichever is trading at a bigger discount.

- MLT (Milton Corporation)

- AFI (Australian Foundation Investments) or ARG (Argo)

Buy LICs

Overall? With discounts out to 2% or more, the broad based LICs are starting to look attractive. By a whisker, long-term investors should consider LICs in preference to index based ETFs.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.