Following the sale of its shares in Autohome, Telstra announced last Wednesday in conjunction with its full year results, that it would use the surplus cash to buy back $1.5 billion of ordinary shares. $250m will be conducted through an on-market buyback, with the balance of approximately $1.25bn through an off-market buyback.

Telstra’s decision to offer an off-market buyback will be welcomed by SMSFs. Due to the high franked dividend component, this is a no brainer for most low rate taxpayers to accept.

Deciding whether to accept an off-market buyback is a pretty straightforward decision. If you are paying tax at a high marginal rate (34.5% or higher), don’t even bother to open the offer document when it hits your mailbox – throw it in the bin. If you are paying tax at 0% (such as an SMSF in pension or an income under the tax free threshold), you are mad if you don’t accept. If you are somewhere in between, such as an SMSF in accumulation, then depending on the tender discount and your ability to use any capital gains tax loss, it will generally make sense to accept.

What’s special about an off-market buyback?

There are two types of buybacks. An on-market buyback is conducted on behalf of the company by a broker purchasing the shares on the ASX. The other type is an off-market buyback which is usually conducted through a tender process, and provided it is an equal access scheme, allows a company to distribute surplus franking credits to its shareholders.

It is this distribution of franking credits that makes the off-market buyback very special. Part of the sale proceeds is treated as a franked dividend, with the other part treated as a capital component. Effectively, the shareholder gets a franked dividend with imputation credits, and materially reduced sale price for capital gains tax purposes. This is what makes off market buybacks so tax advantageous to some shareholders, and because shareholders are keen to accept, means that the company can purchase the shares at a discount to the market price.

Telstra’s off-market buyback

Shareholders will be offered the opportunity to participate and tender all, some or none of their shares, with the tender closing on 30 September.

The tender will be at a discount to the market price, ranging from 6% up to a discount of 14%. Because the buyback is relatively small (the $1.25bn represents only 2.2% of the issued capital), Telstra will accept tenders from those shareholders offering to sell at the lowest price (highest discount), and reject those offering to sell at a higher price (lower discount).

The buyback will comprise two components – a capital component of $1.78, and the balance as a fully franked dividend. For example, if the market price of Telstra shares is $5.50 and the tender discount is 14%, then the buy-back price will be $4.73 and comprise a capital component of $1.78 and a fully franked dividend of $2.95.

The buy-back price will be the same for all tenders – so if the tender is cleared at a discount of 10%, shareholders who nominate discounts of 11%, 12%, 13%, 14% will be successful and receive the price at a 10% discount. Rather than nominate a % discount, shareholders can also tender ‘final price’ (take whatever the market clears at). As a scale-back is expected, Telstra has also announced some priority rules – to clear successful shareholders who are left with a residual parcel of 350 shares or less, and a guaranteed minimum allocation to successful tenderers of the first 880 shares.

The market price will be determined by calculating the volume weighted average price of trades on the ASX over the five trading days from 26 September to 30 September. The announcement of the buy-back price and any scale back will be made on Monday 3 October.

Shareholders worried about Telstra’s share price can also set an overall minimum price. If your tender discount is successful (this also includes ‘final price’ offers), then you will only be accepted if the buy-back price is equal to or above your minimum price.

Should I accept?

The premise is that you should accept the buyback if your effective sale price (after tax) is higher than you could achieve by selling the same shares on the ASX. If you feel that you want to maintain your Telstra shareholding, you just buy them back on the ASX.

Let’s compare the two alternatives – selling your shares on market, or selling your shares in the buyback.

We will do this from the perspective of an SMSF in accumulation (paying tax at 15%), and a SMSF supporting the payment of a pension (paying tax at 0%).

We will also make a few other assumptions:

- the market price for Telstra is $5.50;

- the deemed tax value is also $5.50 (this is determined by the ATO and won’t be available until after the buyback is completed). The sale price for CGT purposes is the deemed tax value less the franked dividend – small variances don’t have a huge impact on the numbers;

- Purchase price for your Telstra – in the first two examples, $3.60 (this was the price paid in the T3 offer), and in examples 3 and 4, $7.40 (the T2 offer price);

- A tender discount of 14% (the maximum), and also the minimum of 6%.

Four examples are shown:

- Example 1: discount of 14%; original purchase price of $3.60;

- Example 2: discount of 6%; original purchase price of $3.60;

- Example 3: discount of 14%; original purchase price of $7.40;

- Example 4: discount of 6%; original purchase price of $7.40

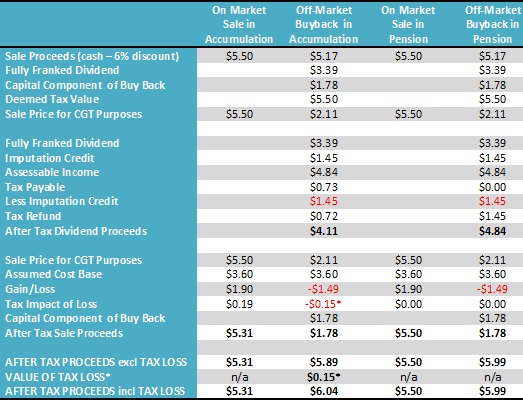

In Example 1, the market price is $5.50. Applying a 14% discount, the buy-back price is $4.73, which comprises a fully franked dividend of $2.95 and a capital component of $1.78. For a fund in accumulation, the after tax proceeds from selling on market would be $5.31. In the buyback, the effective after tax price is $5.36. There is also a capital loss of $1.05 per share, which is potentially worth another $0.11 (15% tax rate, one-third discount) if it can be applied to offset a capital gain on another asset.

For a fund in pension, the buy-back return is $5.99, which is $0.49 higher than if the shares were sold on market.

Example 1 – Discount 14%, Original Purchase Price of $3.60, Market Price $5.50

[1]

[1]* Value of losses can only be accessed by applying against other capital gains

Example 2 – Discount 6%, Original Purchase Price of $3.60, Market Price $5.50

[2]

[2]* Value of losses can only be accessed by applying against other capital gains

Example 3 – Discount 14%, Original Purchase Price of $7.40, Market Price $5.50

[3]

[3]* Value of losses can only be accessed by applying against other capital gains

Example 4 – Discount 6%, Shares Purchased at $7.40, Market Price $5.50

[4]

[4]* Value of losses can only be realised against other capital gains

Conclusion

In pension, it is a no-brainer to accept. At a discount of 14%, you are $0.49 better off – and at the minimum discount of 6%, you would be $1.12 per share richer.

In accumulation, it is still going to make sense to accept in most situations, more so if you can utilize the capital loss.

Two years ago, Telstra conducted an off market buyback and it was cleared at a tender discount of 14%. As this buyback is also relatively small and the dividend component is quite high, it is also likely to clear at 14%. If tendering and you want to be accepted, either tender ‘14%’or ‘final price’.

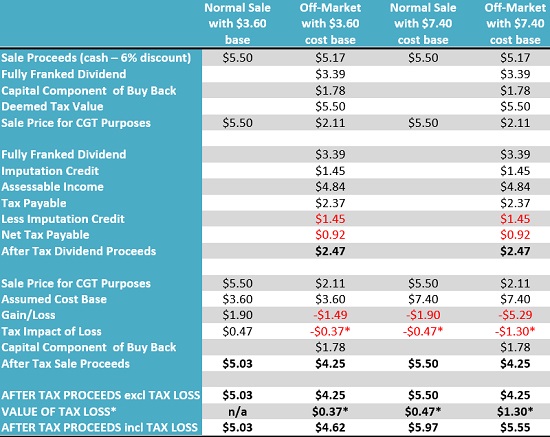

And if you want to review the outcome for a high marginal taxpayer paying tax at 49%, see Example 5 below. Even at the most favourable tender discount of 6%, a shareholder, after taking into account the value of the capital gains tax loss, is $0.41 per share worse off.

Finally, Telstra shares go ex-dividend and ex-buy-back entitlement on Thursday. This means that potentially, you could purchase Telstra shares up until this Wednesday to participate in the buyback. To access the benefits of the franking credits, you will need to observe the 45-day rule.

Example 5 – 49% taxpayer, Discount 6%, Shares Purchased at $3.60 or $7.40

[5]

[5]* Value of losses can only be realised against other capital gains

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.