Nasdaq’s record-breaking run reinforces the boom in US tech stocks and provides an opportunity to take profits on Australian stocks caught up in the fervour.

Our listed tech sector is, of course, a minnow compared to the US. But Australia also has had a tech boom of sorts with dozens of emerging tech companies listing on ASX through Initial Public Offerings (IPOs) or backdoor listings. Some have delivered spectacular gains in the past two years.

WiseTech Global, Pushpay Holdings, Appen, Afterpay Touch Group, Elmo Software, Netwealth Group and HUB24 headline the star information tech and financial tech (fintech) IPOs. They follow the likes of Xero and Altium.

The spike in tech IPOs has made the sector second only to mining, by company volume, on the ASX. There are more than 230 tech companies across software, hardware, fintech and online marketplaces (such as REA Group) – and others still if technology definitions are broadened.

More of them are from overseas. At least 40 tech companies on the ASX are based in New Zealand, Israel, Singapore, Malaysia or Ireland.

The local tech boom has solid foundations. Growth in tech-focused venture capital, private equity, and incubators and accelerators that help starts-up grow, means more tech companies are coming to the ASX in better shape compared to previous booms.

Demand for these stocks is rising as fund managers look to increase their exposure to higher-growth sectors. Growth in tech listings is providing the supply, albeit not enough in terms of large and quality listed Australian companies to satiate the appetite of local funds.

The downside is valuation risk. Australian fund managers whose mandate restricts them from investing in global tech must focus on a small group of large tech stocks. This concentration risk adds to higher valuations in ASX-listed tech and is a warning sign.

As such, the tech sector stands out as a source for profit-taking, in this part two of the Super Switzer Report’s “Stocks to Sell”, end-of-financial-year series (you can read part one here [1]). Australia is producing exceptional tech companies but sky-high valuations in several leading stocks strengthens the case for profit-taking.

This is not a reflection on company quality nor a call to dump tech stocks en masse. Rather, it is a suggestion that early investors in tech stars should take some profits, lighten their position and reinvest into companies with more attractive valuations.

Prospective investors must take great care buying ASX tech stars at current prices. The slightest earnings disappointment could drive prices sharply lower. Should global sharemarkets correct, the tech sector could be ground zero for profit-taking given the extent of gains in the US.

Here are three tech stocks for profit-taking:

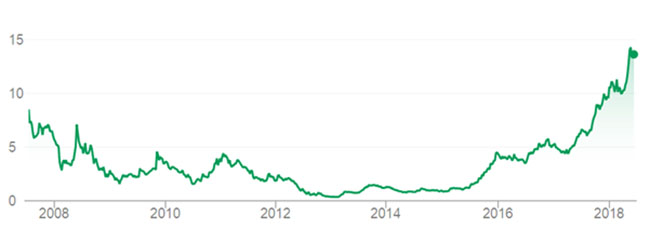

1. Pushpay Holdings (PPH)

The New Zealand-based tithing tech company has a terrific product in a growing global market. Churches, schools and charities are using Pushpay software to accept payments. More than 7,000 customers, including 54 of the top 100 churches in the US, use its echurch product.

Bible Belt churches in the US south-west and south-east have embraced tithing technology and they report rising donations from parishioners and more of them signing up to regular giving plans. An “e-collection plate” is highly effective.

Pushpay dual-listed on ASX in October 2016 through a $54-million IPO. The $2.10 issued shares have raced to $3.92, capitalising Pushpay at just over $1 billion. The stock has gone sideways for much of this year after soaring gains in 2017.

Pushpay expects to be cash flow breakeven by the end of 2018 and the long-term goal is attracting 50% of the medium and large church segments, a market it says is worth more than US$1 billion in annual revenue. The company has many growth options and is doubling revenue each year as user numbers soar.

The issue is valuation. The market is ascribing a billion-dollar valuation to a loss-making company. Pushpay has a good chance to justify and grow that valuation in time, but the market may have run ahead of itself for now.

Pushpay, like other high-growth, loss-making tech stocks, is hard to value. My concern is co-founder and executive director, Eliot Crowther, announcing last week that he sold his entire 9% holding in the company – a move that could unnerve investors.

Tech founders are entitled to exit their company and cash in at some stage, but the sale suggests executives are either losing the faith or believe Pushpay’s valuation is inflated. Either way, insiders taking profits in high-flying tech stocks is often a signal for others to do the same.

Chart 1: Pushpay Holdings (PPH)

[2]

[2]Source: ASX

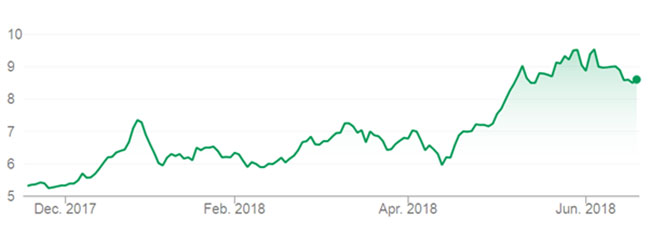

2. HUB24 Group (HUB)/Netwealth Group (NWL)

I have been bullish on both fintech stocks this year amid expectations the Financial Services Royal Commission will quicken the move towards independent financial advice and thus lift demand in listed investment platforms offered by HUB24 and Netwealth Group.

Hub24’s share price soared from $5.20 in January 2017 to $13.55. Hub24’s larger listed peer, Netwealth Group, has raced from a $3.70 issue price in a November 2017 float to $9.02, capitalising it at more than $2.1 billion. Netwealth is among the best floats in years.

Each has benefited from rising interest in fintech stocks and on market expectations that listed investment platforms are among the few winners from the Royal Commission. Some fund managers I know piled into the stocks this year in the lead-up to, and during, the commission hearings.

The long-term prospects of HUB24 and Netwealth stack up. It is possible that Hub24 could grow market share from less than 1% of funds under advice through its investment platform, to more than 5% by 2025 on current growth rates. HUB24 and Netwealth are attracting about 30% of all new net fund flows into investment platforms.

If that happens, both stocks will trade on significantly lower price-earnings (PE) multiples in the next five years than they do now (Hub is on a forward PE of 67 and Netwealth is on about 55, using consensus estimates). But their near-term valuation multiples leave no room for disappointments and seem to assume that banks will not fight harder in investment platforms to keep their market share.

With both stocks more than doubling over a year, and with sentiment (in terms of HUB24 and Netwealth) from the Royal Commission peaking, early investors should lock in some profits.

My hunch is they will be able to buy back into both stocks at lower prices later this year or next and get cheaper exposure to the trend towards independent financial advice and platforms.

Chart 2: HUB24 (HUB)

[3]

[3]Source: ASX

Chart 3: Netwealth Group (NWL)

[4]

[4]Source: ASX

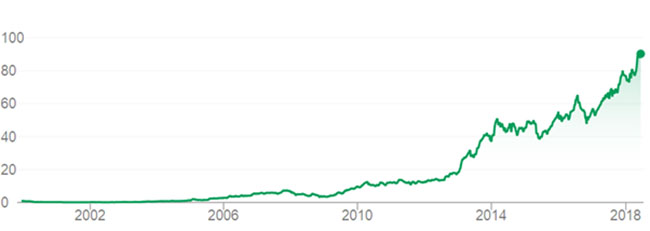

4. REA Group (REA)

The online platform, a doyen of the Australian tech sector, deserves more respect than loss-making tech newcomers’ “unicorn” valuations (over $1 billion). REA Group has for years proved wrong the naysayers who argued the stock was overvalued.

One of my favoured strategies over the past decade was to buy the big platform stocks – Seek, Carsales.com, REA Group and Webjet – on bouts of price weakness during market corrections. Value investors need to pounce when exceptional companies trade below intrinsic value.

REA’s inclusion on this list is based mostly on valuation grounds. The company is performing strongly, meeting market expectations and should deliver a good FY19.

REA has shown before that it can exploit its pricing power when markets slow, through higher fees for advertising and other services, and it has done a good job expanding margins. REA continues to make sensible acquisitions and should quicken overseas growth.

However, two headwinds strengthen the case for profit-taking. The first is the property market. I have not been a bear on the property market, except for apartments in Brisbane and other oversupplied inner-city markets. I expect manageable, single-digit declines in house prices.

Still, the property market faces its softest period in years. Falling auction clearance rates in several markets could be a precursor to lower listing volumes as vendors sit tight and wait for higher prices to return. REA can do well in softening markets if properties take longer to sell (and extra advertising is required). But moderating listing volumes are a challenge.

The second headwind is valuation. REA is trading on a forward PE of about 37 times FY19 earnings, on Macquarie’s numbers. This is near REA’s peak PE in FY14 when the property boom was building steam and had a few years of strong growth in front of it.

If REA reverts to its three-year rolling average PE, the share price would decline by around 20%, wrote Macquarie in late May. The insightful share-valuation service, Skaffold, believes REA is trading 32% above fair value at the current price.

As REA hurtles towards $100 in a slowing property market, some profit-taking is prudent. True believers might maintain a smaller position in REA and use their profits to top up that position at lower prices in the next 12 months.

An average price target of $86.69 for REA, based on the consensus of 11 broking firms, also suggests REA is overvalued at the current price. More brokers lately have downgraded their recommendations to hold or underperform, after REA’s price rally.

Chart 3: REA Group (REA)

[5]

[5]Source: ASX

- Tony Featherstone is a former managing editor of BRW, Shares and Personal Investor

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.