US jobs came in weaker than expected but economists found excuses for the slight miss. The consensus remains that the economy is still looking strong and the Fed will stick to its script and raise interest rates in September and December.

Let’s look at the numbers, with 157,000 jobs created against an estimate of 192,000 but Toys R Us caused 37,000 positions to disappear. Other unforeseen developments also helped explain the miss. Trump’s trade ‘spat’ has also added to some of the job losses.

Unemployment fell from 4% to 3.9%, which is nearly an 18-year low, which is a psychological plus. It should be remembered that the monthly average for jobs growth this year has been a huge 200,000. You always have to be careful of one month’s numbers. The chart below shows there’s a pattern of a couple of big months, followed by a pullback and then jobs surge again.

The other positive from these slightly disappointing numbers was the stock market reaction, which was largely positive, with Apple and even IBM adding to the Dow Jones index. What was even more surprising was this market rise, despite China saying it would slap $US60 billion worth of tariffs on US goods, with imposts ranging from 5% to 25%. This was a retaliation to the US President talking out loud about the $US200 billion worth of tariffs on specified goods to have the tariffs raised from 10% to 25%!

Why was the stock market so nonreactive to the news? CNBC talked to Scott Clemens, the chief investment officer at Brown Brother Harriman and this is what he said: “Even if you take the proposed tariffs into account, the impact would be rather limited…. from a macroeconomic standpoint, it’s still pretty small.”

This could explain why small caps that would benefit from a trade war have been losing friends on Wall Street, while big caps have been gaining ground.

Also helping stocks has been a very good US reporting season. The latest news from FactSet is: “81% of the companies in the S&P 500 have reported actual results for Q2 2018. In terms of earnings, more companies are reporting actual EPS above estimates (80%), compared to the five-year average. If 80% is the final number, it will mark the highest percentage of S&P 500 companies reporting a positive EPS surprise for a quarter, since FactSet began tracking this metric in Q3 2008.

In aggregate, companies are reporting earnings that are 4.9% above the estimates, which is also above the five-year average. In terms of sales, more companies (74%) are reporting actual sales above estimates compared to the five-year average. In aggregate, companies are reporting sales that are 1.4% above estimates, which is also above the five-year average.”

Clearly, this is a very good reporting season and that’s why stocks continue to rise.

Let’s head home and check out the unmissable market developments of the week.

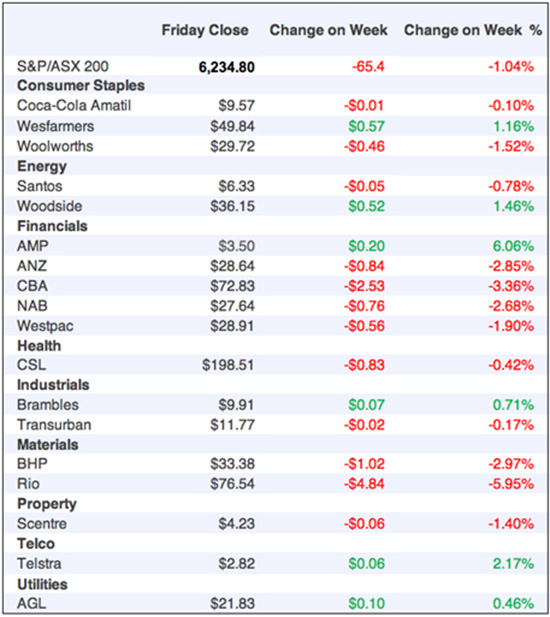

We were down 1% on the S&P/ASX 200 index for the week. While there was a tech-bump for stocks when Apple became a trillion dollar company (with the likes of Appen and Xero going higher), the positivity didn’t last. Banks were victims of profit-taking by short-term players, after the release of a Productivity Commission report, which told us nothing new. The Treasurer latched on to it to bag the banks and the Government has to do that, with Bill Shorten regularly telling the media that the Turnbull Government wants to help banks get tax cuts rather than see working Aussies get hospitals and schools.

The impact of Bill will be that he will be remembered as the best bank basher or bank killer of all time. I worry his crusade against the banks will be like Kevin Rudd’s mining tax crusade, which hit miners when the boom was over! That brought no real tax revenue and helped seal his fate as a PM. Guess who was one of the masterminds of that knifing? Yep, ‘kill’ Bill Shorten.

On Friday alone, CBA dropped 1.2% to $72.83, Westpac lost 1% to $28.91, NAB slipped 0.6% to $27.64 and ANZ fell 0.9% to $28.64. The sector lost about 2% for the week and it could get worse, as the Royal Commission cranks up again this week, with super funds in the frame.

Rio’s OK earnings report didn’t help either, with the mining sector down 2.4% for the week. Both Rio and BHP had bad Fridays, with the former down 1.4% to $76.54, while the latter lost 1.6% to $33.38. Some of this fall was related to trade war fears, with the US and China flexing their tariff muscles. This is why I’ve been saying a stocks sell off can’t be ruled out, with a guy like Donald Trump poking the China bear.

The only standout plus in the big stock department has been Telstra’s sneaking higher performance. On Monday, I had Roger Montgomery explain why he’s given up on his near-decade hate session on Telstra, so you might want to catch up on my Money Talks show [1] for that. When a good company hater like Roger changes his mind, there has to be good reasons.

In other interesting big cap news, the SMH pointed out that “Credit Suisse retained its outperform rating on CSL saying that data from the United States Plasma Protein Therapeutics Association (PPTA) showed that immunoglobulin demand and growth was going strong.” Credit Suisse said it was retaining its outperform rating for CSL based on the company’s continued strength in immunoglobulin demand and the company’s shift to higher margin products.

Meanwhile, the upcoming reports from retailers could be interesting, with another good retail figure from the ABS. Retail trade rose by 0.4% in June, taking the annual growth rate to 2.9%. And I loved this, as a reinforcement of my positive view on the economy from CBA senior economist Kristina Clifton, who said that the lift was driven in part by improving employment levels. “The driving factor seems to be the lift in household incomes courtesy of strong employment growth,” she said. “And consumers seem more willing to spend as shown by the sharp lift in consumer sentiment.” (SMH)

In summary, given our strong rise in June for the stock market and the OK July, it only makes sense that we’d have an ordinary week for stocks this week, with RIO not shooting the lights out and telling us that cost-cutting is going to be hard going forward. That means rising commodity prices become important and this trade war anxiety doesn’t help our miners and our market overall. That said, I do like the fact that the VIX (or fear index) was under 12 overnight, which says Wall Street isn’t too panicky about all this trade testosterone war talk.

Gotta love those optimistic Yanks!

What I liked

- The annual growth rate of the Living Cost Index for wage-earning households accelerated to 2.3% in the June quarter, up from 2% in the March quarter – the strongest rate of growth in four years. The LCI outpaced the annual rate of headline inflation, which lifted to 2.1% in the June quarter from 1.9% in the March quarter. This is a positive sign for the economy.

- International scheduled passenger traffic through Australian airports increased to 3.03 million in May from 2.87 million a year ago – an increase of 5.4%.

- In seasonally-adjusted terms, new detached house sales rose by 2.2% in June – the first monthly increase in six months. However, sales fell by 5.3% over the year.

- Retail trade rose by 0.4% in June, after rising 0.4% in May and rising 0.5% in April. Annual spending growth rose from 2.5% to 2.9%.

- The ABS has released retail spending data for the June quarter. CommSec obtained detailed spending data from the ABS in nominal and real (inflation-adjusted) terms. The data provides insights on how spending has been changing across the economy. Spending rose 1.2% in real terms in the June quarter – above the 0.7% decade average. Spending has been supported by weak prices. Retail prices fell by 0.1% in the June quarter.

- The AiGroup services sector gauge eased 9.4 points to 53.6 in July. The CBA services sector gauge eased from 52.7 to 52.3 in July. Any reading over 50 indicates expansion.

- The Fed left the federal funds target rate unchanged as expected in a 1.75%-2% range.

- For US economic data, personal income and spending both rose by 0.4% in June. The core personal consumption expenditures (PCE) price index rose by 0.1% to 1.9% for the year to June. The Employment Cost Index (ECI) rose by 0.6% in the June quarter. The Case-Shiller Home Price index rose by 0.7% in May.

- The ISM for New York manufacturing index surged from 55 to 75 in July.

- Apple has become the first US company to pass US$1 trillion in market capitalisation, which means little but it reinforces market positivity.

- The Bank of England lifted the base rate by 25 basis points to 0.75%. While the vote was 9-0 to lift rates, Governor Carney signaled that the Bank was in no hurry to lift rates again: “policy needs to walk – not run – to stand still.”

- The Caixin Manufacturing Purchasing Managers’ Index (PMI) fell from 51 to 50.8 in July, in-line with market forecasts but results above 50 points imply expanding activity.

What I didn’t like

- Trade war talk is still restraining Wall Street.

- In July, 85,551 new vehicles were sold, down 7.8% over the year. In the 12 months to July, sales totalled 1,187,883 units, up 0.6% on a year ago.

- The drunken canary in the coalmine, with European share markets falling on Monday, due to disappointing earnings results. Shares of Heineken fell 6.5%, after the world’s second largest beer maker reported weaker-than-expected earnings and cut its full-year guidance.

A HUGE dislike

I hate the media’s use of statistics to scare us about a house price collapse. Look at this objective assessment of our housing numbers by CommSec’s Craig James: “The CoreLogic Home Value Index of capital city home prices fell by 0.6 per cent in July to stand 2.4 per cent lower over the year. The national home price index also fell by 0.6 per cent in the month to be down 1.6 per cent over the year. The monthly decline was the largest fall in 6½ years.”

Yep, the monthly decline was the worst in 6½ years but it was a 0.6% fall. This is only significant because for over six years, so many months have seen price rises or very small falls. I talked to BIS Shrapnel’s Rob Mellor, who said claims of big price falls are exaggerated. I have him on my TV show on Monday week to get the true story of future price falls.

The Week in Review:

- A picture paints a thousand words and charts can do the same! With that in mind, I gave a pictorial presentation of the graphs that say, ‘staying long stocks makes a lot of sense.’ [2]

- With earnings season upon us, Paul Rickard [3] talked about the key data you should be paying attention to.

- Going against the herd is hard but can reap rewards if you’re prepared to take a risk. James Dunn offered 4 contrarian buys to consider. [4]

- Among this week’s Hot Stocks was Aristocrat [5] from CMC Markets’ Michael McCarthy. Find out why!

- As we head into reporting season, downgrades outnumbered upgrades in our first Buy, Hold, Sell – what the brokers say. [6] And in our second edition [7], two resources companies – Regis Resources and Senex Energy – saw upgrades.

- Charlie Aitken talked about why Clydesdale Bank [8] is still his number one ASX-listed bank.

- Not all old-school media is dead! Tony Featherstone offered two radio stocks [9] you should be keeping an eye on and shared his view about who the real winner is from the Nine/Fairfax merger [10].

- Could an SMSF be right for you? Graeme Colley [11] shared six steps to setting up an SMSF.

- Our Stock of the Week [12] was Corporate Travel Management (CTD) by Manny Pohl of ECP Asset Management.

- In Questions of the Week [13], we answered some very detailed questions from a happy subscriber who is after an SMSF check-up.

Top Stocks – how they fared:

[14]

[14]What moved the market?

- The US proposed to increase tariffs on $US200 billion worth of Chinese goods from 10% to 25%, with China responding that it would take countermeasures.

- Australia’s earnings season kicked off this week, with Rio Tinto the first major company to report. The miner’s first-half underlying earnings fell short of market expectations.

- Commodity prices took a slide during the week, with copper, iron ore, zinc and other materials all taking a hit.

- Apple became the first US listed company to reach the trillion dollar hallmark.

- The Banks took a lashing with the Productivity Commission accusing the lenders of flooding the market with similar products, ripping off customers and misleading them to gain new business.

Calls of the week:

- Charlie Aitken still backs Clydesdale Bank (CYB) [8], calling it his ‘highest conviction’ ASX-listed bank.

- Tony Featherstone made a call on who the real winner is out of the Nine/Fairfax merger. [10]

- Coles made a call to give out free plastic bags indefinitely after previously pledging to phase out single use bags by July. The supermarket chain then backflipped once more, saying that it would begin charging 15 cents a bag from August 30.

- AMP Chairman David Murray called out “ASX corporate governance principles” for contributing to “what happened to AMP and others in the financial sector” following revelations out of the Hayne Royal Commission.

The Week Ahead:

Australia

Monday August 6 – ANZ job advertisements (July)

Tuesday August 7 – Reserve Bank Board meeting

Wednesday August 8 – Housing finance (June)

Wednesday August 8 – Reserve Bank Governor speech

Friday August 10 – Lending finance (June)

Friday August 10 – Statement on Monetary Policy

Overseas

Tuesday August 7 – US JOLTS job openings (June)

Tuesday August 7 – US Consumer credit (June)

Wednesday August 8 – China International trade (July)

Thursday August 9 – China Inflation (July)

Thursday August 9 – US Producer prices (July)

Thursday August 9 – US Wholesale inventories (June)

Friday August 10 – US Consumer prices (July)

Friday August 10 – US Treasury budget (July)

Friday August 10 – China Vehicle sales (July)

Food for thought:

“Do you want to know who you are? Don’t ask. Act! Action will delineate and define you” – Thomas Jefferson

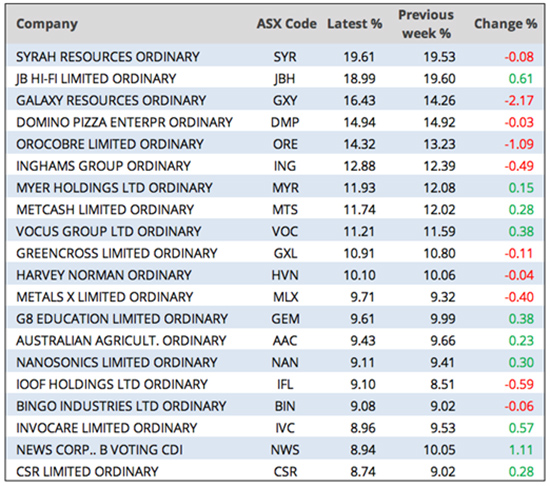

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

[15]

[15]Chart of the week: [16]Source: Commsec

[16]Source: Commsec

Top 5 most clicked:

- These charts still scream good news for stocks [2] – Peter Switzer

- Clydesdale Bank (CYB): all-time highs and going higher [8] – Charlie Aitken

- 4 contrarian buys to consider [4] – James Dunn

- What to look out for this company earnings season [3] – Paul Rickard

- Buy, Hold, Sell – what the brokers say [6] – Rudi Filapek-Vandyck

Recent Switzer Super Reports:

- Monday July 30 : A thousand words [17]

- Thursday 02 August: Back on board [18]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.