Positivity remains for stocks with the two big drivers of US share prices – earnings and the economy – prevailing, despite another controversial week for President Donald Trump. At home, our market keeps defying gravity.

The S&P/ASX 200 climbed 23 points (or 0.4%) to 6285 on Friday for a 0.3% advance over the week. Yep, it’s not convincingly positive but we have had a great run since June and this is the old “sell in May and go away” time period for stocks.

And Donald hasn’t been a big help with his lamentation this week on CNBC. “I’m not thrilled…I don’t like all of this work that we’re putting into the economy and then I see rates going up.”

This followed the new Fed boss telling it as it is when it comes to interest rates but he did say a lot to keep stock buyers pretty happy with their activity. On Tuesday, following Fed Chair Jerome Powell’s optimistic comments about the US economy, the stock market stuck to its positive disposition even with the President’s confusing views on Russian boss, Vladmir Putin and US intelligence services.

“With appropriate monetary policy, the job market will remain strong and inflation will stay near 2 per cent over the next several years,” Mr Powell said in his testimony to the US Senate Committee.

And even though some market influencers wanted to suggest the chances of rate rises looking more likely following these comments, the fact that the Fed chairman gave the economy a strong endorsement without any real inflation fears, has to be a plus.

This positivity was reinforced by a very rosy outlook for the global economy from the International Monetary Fund.

The IMF left its forecast for global economic growth unchanged at 3.9% in 2018 and 2019, above the 40-year average growth rate of 3.5%.

“If realised it would be the fastest pace of growth in seven years,” explained CommSec’s Craig James. “While there was no update for Australia, economic growth is forecasted to grow by 3 per cent in 2018 and 3.1 per cent in 2019.”

That’s a nice result and again supports stock market positivity.

Meanwhile, the minutes from the July 3 Board meeting were issued.

“The Board’s neutral policy bias for interest rates remains with a period of record low interest rate stability ahead for the foreseeable future,” James said.

“However, the phrase ‘the next move in the cash rate would more likely be an increase than a decrease’ was reinstated after being removed last month.”

The Big Bank is not rushing to raise rates but if the economy keeps delivering like it did this week with a huge increase in jobs – nearly 51,000 when economists expected 17,000 – then I think we will see the cash rate moving higher next year and not in 2020, as some more negative economic experts are predicting.

Back to stocks locally, overall the technology sector rose 1.4 % over the week, however industrials were the best performers by sector, with a 1.7% gain.

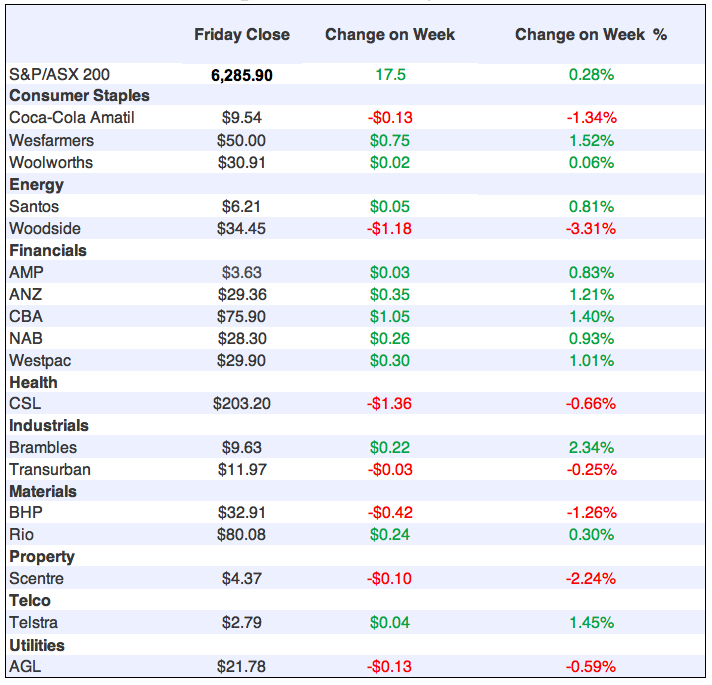

The ‘re-loving’ of the banks continued, with Banks up for the week. On Friday, CBA shares rose 0.7% to $75.90, Westpac went up 0.7% to $29.90, NAB climbed 0.6% to $28.30 and ANZ was 0.5% higher to $29.36.

The stocks shock of the week was two analysts telling us that they are in a forgiving mood for QBE! Now that might be carrying positivity too far for even me.

Fairfax says “Citi’s insurance analyst Nigel Pittaway upgraded QBE to buy from neutral ahead of the firm’s earnings release on August 15.”

Asset disposals in Asia and the US have improved the business and the overall economic outlook seems “supportive”, the broker said. “Citi’s deep dive into QBE’s plans give us a little more confidence in our forecasts for FY19 and beyond. If our forecasts prove correct, this is an outstanding buy in this market,” Nigel says.

So I’ve shared that one with you but it’s up to you if you want to forgive QBE.

Adding to my positivity was the fact that by early Friday on Wall Street we learnt that 16.4% of S&P 500 companies had released their latest quarterly results, with 83% of them topping analyst expectations, according to FactSet. “Wall Street has high expectations for this earnings season, with analysts expecting earnings growth of 20%,” FactSet said.

On the subject, Ed Yardeni, president and chief investment strategist at Yardeni Research was positive for this reporting season, which has to be good for our market’s potential to rise.

“There have been some individual surprises, but it’s still looking like we’re going to get year-over-year growth in the neighbourhood of 20%.” (CNBC)

My only real concern remains the US President. On CNBC’s Squawk Box, he said: “I’m ready to go 500”! This means he could take tariffs on China from his latest threat of $200 billion to $500 billion, which means he’s gambling with much higher stakes. If he did this, the trade war and stock market implications would be very worrying.

What I liked

- Employment rose by 50,900 in June after a 13,400 increase in May (previously reported as a rise of 12,000 jobs). Full-time jobs rose by 41,200 and part-time jobs rose by 9,700. Economists had tipped an increase in total jobs of around 17,000. Total employment is at a record-high 12.574 million.

- Our unemployment rate was unchanged at 5.4%. But at 5.37% it is the lowest unemployment rate in 5½ years. The participation rate rose from 65.5% to 65.7% – just below record highs.

- State-by-state news on the jobless rate in June was great, except for Victoria. NSW 4.7% (May 4.9%); Victoria went up to 5.6% (May 5.1%); Queensland 5.9% (May 6.2%); South Australia 5.4% (May 5.6%); Western Australia 6.1% (May 6.3%); Tasmania 5.8% (May 6.6%). In trend terms, unemployment in the Northern Territory was steady at 4.1%; ACT unemployment fell from 3.6% to 3.5%.

- The weekly ANZ-Roy Morgan consumer confidence rating rose by 1.2% (the first lift in five weeks) to 121.5, above the average of 114.0 since 2014.

- The Philadelphia Fed Manufacturing index rose 5.8 points to 25.7 points (survey of economists predicted 21.5 points) in July.

- The US Conference Board’s Leading Index rose by 0.5% (survey: +0.4%) in June.

- US initial jobless claims fell to 207,000 (survey: 220,000) last week. This is the lowest level since December 1969.

- US industrial production rose by 0.6% (survey: +0.6%) in June.

What I didn’t like

- Energy stocks ended the week 2.2% lower, while the materials segment of the market fell 1.2% but they have been having a great run until recent falls.

- This quote: “The tail risk of a Sino-US trade war is getting fatter. Chinese President Xi Jinping, like US President Donald Trump, is a nationalistic leader who has emphasised his strength and resolution and cannot afford to look weak in a confrontation with a large sovereign power,” commented Chi Lo, senior economist at BNP Paribas Asset Management and reported by Fairfax Media. “The two sides may misjudge each other’s intentions when patriotism takes over rationality and push themselves into an escalating series of attacks and retaliations. The resultant damages are negative for risk assets.”

A big like

The performance of Afterpay Touch this week, where I learnt the founders Nick Molnar and Anthony Eisen made $110 million each on Thursday after some great results, was good news. Their stock was up 30% this week, with 400 retailers signing up for their service in the States, after only two months’ work knocking on doors there. Overall, they have about 16,500 retailers taking their ‘product’. Why am I so happy when I don’t hold any Afterpay stock? Well, our experts here at Switzer have given the business the thumbs up in the past and Anthony was a prized student of mine when I started out teaching Economics at Sydney Grammar School, ahead of heading off to UNSW to teach with Dr. John Hewson.

The Week in Review:

- I looked at the importance of forming a strong investment strategy [1]. After all, the biggest mistake an investor can make is changing a good strategy prematurely!

- As the banks face higher borrowing costs, investors need to stay on their toes. Paul Rickard [2] offered a comprehensive guide to the latest term deposit rates on offer.

- James Dunn [3] took a look at a new global fund offering diversification to investors looking to branch out beyond Australia.

- Wesfarmers and AMP featured in this week’s Hot stocks [4] – find out why!

- In this week’s first Buy, Hold, Sell – what the brokers say, [5]a number of high flyers, such as Sydney Airport and Fisher & Paykel, faced downgrades. And in our second edition [6], Fortescue Metals received a double upgrade.

- The air is heating up, which means it might be time to get out of overpriced companies. Charlie Aitken [7] reviewed what the Netflix story is telling us about tech stocks.

- Tony Featherstone [8] reviewed two niche AREITS to get excited about. Find out which ones!

- There are a couple of rules that you need to be on top of to make sure you’re eligible for all of your franking credits. Graeme Colley asked ‘does your SMSF qualify? [9]’

- In Question’s of the Week [10], we answered reader’s queries about Transurban, Telstra and Ardent Leisure.

Top Stocks – how they fared:

[11]

[11]What moved the market?

- US President Trump challenged the Federal Reserve, saying he’s “not thrilled” with the interest rate hike, breaking the long-established standard of the White House not commenting on central bank policy.

- There are growing concerns that the European Union will retaliate if Trump raises tariffs on car imports following next week’s key meeting between the US President and EU chief Jean-Claude Juncker.

- Surprise! Australia’s June employment data was much stronger than anticipated.

- International benchmark Brent crude tumbled nearly 9% from last week’s high of over $79 a barrel. It’s most recent dip comes amid emerging evidence of higher global crude production.

Calls of the week:

- Charlie Aitken called ‘Sell’ on global and Australian tech stocks, [7] including WiseTech Global (WTC), Appen (APX), and Afterpay Touch Group (APT).

- Westpac made the call to stop property lending to SMSFs.

- Tony Featherstone named two niche AREITs [8] to get excited about.

The Week Ahead:

Australia

Tuesday July 24 – Weekly consumer confidence

Wednesday July 25 – Consumer price index (June quarter)

Wednesday July 25 – Skilled internet job vacancies (June)

Thursday July 26 – Export & import prices (June quarter)

Thursday July 26 – Detailed job data (June)

Friday July 27 – Producer price indexes (June quarter)

Overseas

Monday July 23 – US Chicago Fed National Activity Index (June)

Monday July 23 – US Existing home sales (June)

Tuesday July 24 – US Home prices (May)

Tuesday July 24 – US, Europe ‘Flash’ purchasing managers (July)

Tuesday July 24 – US Richmond Fed Manufacturing Index (July)

Wednesday July 25 – US New home sales (June)

Thursday July 26 – US Trade in goods (June)

Thursday July 26 – US Durable goods orders (June)

Friday July 27 – China Industrial profits (June)

Friday July 27 – US Economic growth (June quarter, advance)

Food for thought:

“Real knowledge is to know the extent of one’s ignorance.” – Confucius

Stocks shorted:

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

Chart of the week:

Top 5 most clicked:

- With term deposit rates rising, where is the best rate? [2] – Paul Rickard

- The biggest mistake investors make – changing a good strategy prematurely! [1] – Peter Switzer

- Is Netflix telling you to rotate from growth to value? [7]– Charlie Aitken

- Buy, Hold, Sell – what the brokers say [5] – Rudi Filapek-Vandyck

- Hot stocks – Wesfarmers and AMP [4]– Switzer Report

Recent Switzer Super Reports:

- Monday 23rd July: Strategy time [12]

- Thursday 19th July: Too cool for school [13]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.