Apart from our stock market this week showing that it still plays follow the leader, the big revelation is that Wall Street will sell off when a Fed official suggests the central bank won’t cut rates in March but investors are happy to buy when the likes of the Bank of America gave tech companies such as Apple a better than expected upgrade, with its potential benefit from AI a part of the positive story for the company.

As I told Paul Rickard on Thursday at the start of our Boom Doom Zoom webinar, the conclusion for investors needs to be this: I want to be a buyer of sell-offs. Why?

No, it’s not because I’m an eternal optimist (as one keen follower told me this week), I’m a long-term optimist when it comes to economies and markets. As an undergraduate at the University of New South Wales, I did a lot of economic history, but I can be a short-term pessimist, as I was over the past few weeks.

You see, I was expecting a profit-taking few weeks because of the big rise of the stock market over November and December. Let’s look at it locally.

That was a 9.5% bounce-back, which most of you would recall I was expecting, though the size of the bounce even surprised this “eternal optimist”!

And that’s why profit-taking by professional fund managers and stock players was always on the cards in January. However, the size of that late-year comeback and the Thursday market response to Apple’s new and improved rating, convinces me that while short-term negatives will undermine stock prices, the bigger, longer drivers of stock prices will make 2024 good for investors.

Those longer-term influences include the view that interest rates will fall this year, which should help company profits. In addition, history says the fourth year of a US presidency is the second best for stocks and also that the S&P500 is close to its all-time high.

And while that might worry you, recall that US markets have been below their all-time high for over two years and when levels like these get broken, there’s usually a sustained rise higher for indexes. Also, the history of interest rates falling and stock markets rising has a high repeat incidence as well, and this is worth remembering when sell-offs happen.

Ironically, the sell-off this week was linked to comments from Chris Waller (not the horse trainer but the Fed official) and it wasn’t good for those expecting the first cut in US rates in March. However, it was a good revelation for the long-term optimistic stock player.

This is how The Economic Times reported his utterances: “The U.S. is ‘within striking distance’ of the Federal Reserve’s 2% inflation goal, but the central bank should not rush towards cuts in its benchmark interest rate until it is clear lower inflation will be sustained”, Fed Governor Christopher Waller said on Tuesday.

“And regardless of when rate cuts begin, Waller said they should proceed ‘methodically and carefully,’ not come through the sort of large, fast reductions used when the Fed is trying to bail out the economy from a shock or a pending downturn.”

Even though JPMorgan’s CEO Jamie Dimon amused those at the Davos conference in Switzerland, that “Goldilocks investors shouldn’t forget three bears,” historically Jamie isn’t a great oracle on markets.

Fair enough, inflation is still a bear and so is the Fed, as we saw with Waller this week, and you can’t rule out the bearish implication of the Middle East and Ukraine. But these all look like shorter-term threats rather than long-term reasons to run away from stocks.

By year’s end I could have a different view if Donald Trump regains the presidency and is threatening China with another trade war. However, for 2024, I remain a buyer of tech, growth stocks and small cap companies/funds. (On Monday’s TV show I interview Ben Griffiths, the portfolio manager of a good small cap fund Eley Griffiths.)

On this year, UBS is in my optimistic court, with CNBC reporting the following: “The S&P 500 [1] is in for yet another strong year, according to UBS. The firm lifted its year-end target on the S&P 500 from 4850 to 5150, representing 7.7% upside for the benchmark stock index from Friday’s close. The S&P 500 ended last week at 4783.83.”

UBS strategist Jonathan Golub says earnings should drive 2024 returns but “falling interest rates should support incrementally higher multiples.”

Importantly, next week is a biggie for US company reporting and will have a big impact on what markets do over the next few weeks.

Interestingly, history says the first half of a US election year can be slower than the second half, so this might not be a “sell in May and go away” year. Here’s CNBC again: “The broad index has climbed an average of 7.5% in a presidential election year and has finished higher in three out of every four, according to firm data of relevant years between 1928 and 2020. But there’s typically a pause in the first six months before a rally in the second half, said Stephen Suttmeier, a technical research strategist at the bank.”

Wall Street again was positive on Friday and that should help our market next week, but what about the local story for the past five days?

We were down for four days on a trot, until Wall Street’s tech-led rebound met a surge in buying for coal stocks. The S&P/ASX 200 lost 77.1 (or 1.03%) for the week to finish at 7421.20 but it would’ve been bloodier if we didn’t see a big kickback for out-of-favour lesser, local tech stocks. This is how the AFR reported it: “Ten out of the index’s 11 sectors notched gains, with tech the big winner, up 3 per cent. Zip flew 11.42 per cent higher to 63.5 cents, EML Payments jumped nearly 10 per cent to $1 and Xero shot up 4.8 per cent to $114.73.”

The table below will show you how the top stocks fared over the week, but the surprise story was Whitehaven, which rose 3.8% to $8.11 after retaining full-year coal production guidance. And for long-term Mesoblast believers, there was some good news with the share price up 13.21% to 30 cents after the US FDA gave a thumbs up to a treatment for a paediatric disease.

What I liked

- The local jobs report that saw the loss of 65,100 jobs. Of course, while I’m not happy about that for those who are unemployed, as an economist I know it shows rate rises are working and should stop the RBA from more excessive rate rises.

- Unemployment stayed at 3.9% in December, which was the good news in this labour market report.

- This from Jarek Kowcza, senior economist at St. George Economics: “52% of consumers expect the Reserve Bank (RBA) to continue hiking, down from 60% in December. The chance of further hikes has reduced as inflation and other recent data have surprised to the downside.”

- The University of Michigan’s Survey of Consumers [2] for January showed a 21.4% year-over-year jump to reach its highest level since July 2021.

What I didn’t like

- The Westpac-Melbourne Institute consumer confidence index fell 1.3% in January to 81. Any Christmas cheer was short lived as consumers remain deeply pessimistic.

- Locally, dwelling commencements fell by 10.4% to 37,116 in the third quarter of 2023, the lowest level in a decade. Not great for the economy and house prices going forward.

- U.K. retail sales volumes fell by 3.2% in December after a poll by Reuters suggested an expected drop of just 0.5%. The reading “increases the chances the economy may have ended 2023 in the mildest of mild recessions,” said Alex Kerr, assistant economist at Capital Economics.

The US is the home of optimists, Jamie!

Not only did US consumer sentiment rise in January, retail sales increased 0.6% in December, buoyed by a pickup in clothing and accessory stores, as well as online non-store businesses. Economists expected a rise of 0.4%. Meanwhile, initial filings for US unemployment insurance totalled 187,000 for the week ending January 13, the lowest level since September 24, 2022. This good news (despite 11 big rate rises from the Fed) really makes the case that the US will avoid a recession and have a soft landing that could easily help Goldilocks investors have a nice rest from worrying about their stocks and market bears.

Switzer This Week

Switzer Investing TV

- Boom Doom Zoom: [3] Peter Switzer and Paul Rickard answers your questions on BHP, WDS, SIG & more

- SwitzerTV Investing: [4]Jun Bei Liu gives us 5 hot small cap stocks for 2024

Switzer Report

- Two well-placed small-cap retailers well-placed [5]

- 3 large-cap elite [6]

- “HOT” stock: Champion Iron (CIA) [7]

- Questions of the Week [8]

- 2024 set to be a good year, and here’s why… [9]

- Our portfolios for 2024 [10]

- HOT stock: Super Retail Group (SRG) [11]

- Lessons I’ve learned from investing in shares [12]

- 7 positive characteristics that set stocks apart [13]

- Buy, Hold, Sell — What the Brokers Say [14]

Switzer Daily

- Rate cuts on their way! [15]

- Australians worried about less money retirement won’t pay to fix it! [16]

- Should the RBA stop watching inflation and start looking at insolvencies? [17]

- Common sense judge gives gas project the thumbs up [18]

- Albo’s losing friends & voters, so tax cuts are coming! [19]

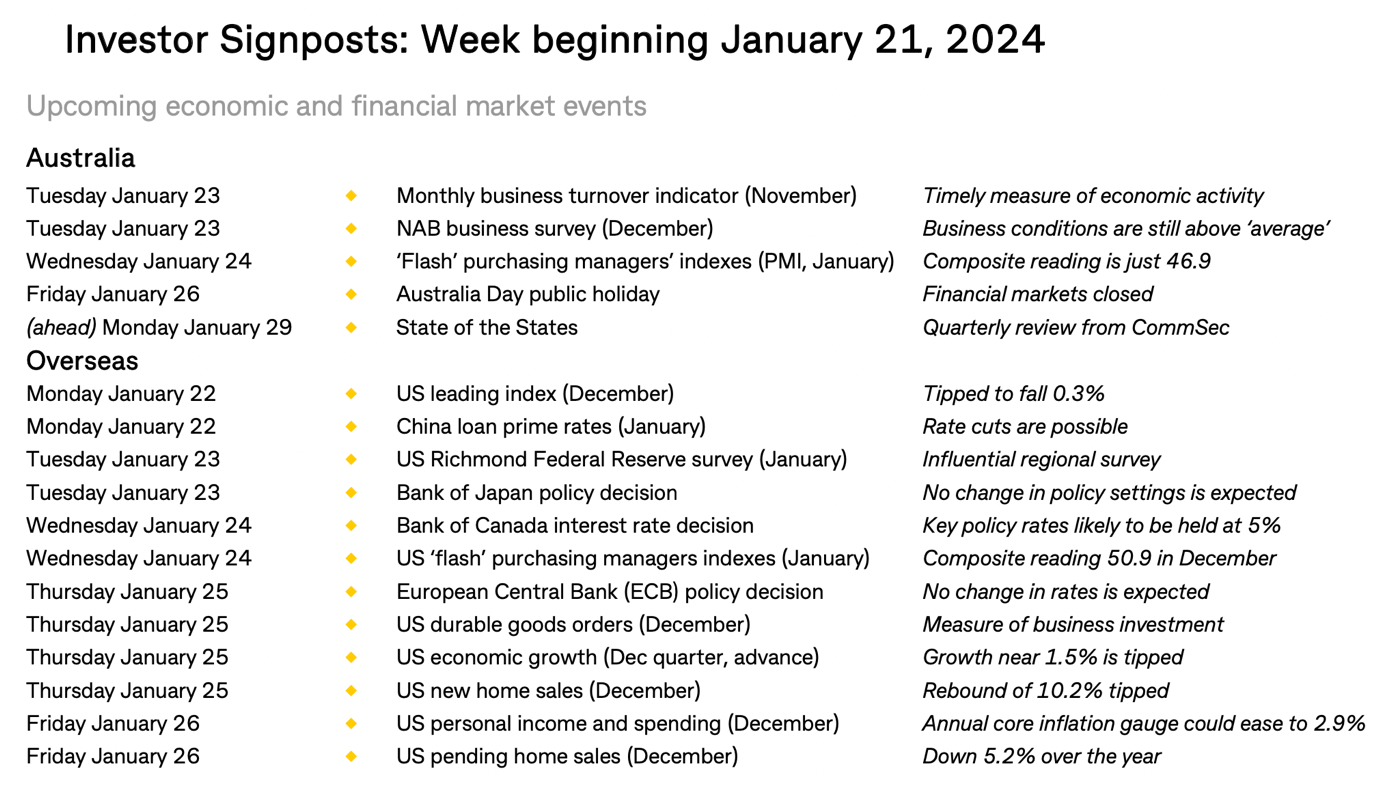

The Week Ahead

Top Stocks — how they fared

Most Shorted Stocks

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before

Chart of the Week

Is the job market telling us rate rises are over and cuts are coming?

Quote of the Week

“Make no mistake, the labour market is cooling, and following a recent run of softer inflation data, RBA rate cuts are coming.” (IG market analyst Tony Sycamore)

Disclaimer

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.