The biggest investment surprise of 2016 was the turnaround in commodity prices and ipso facto, resource stocks. I am struggling to think of any broker analyst or expert commentator who predicted the sudden rebound in the iron ore and other metal prices.

Almost exactly a year ago today, Rio Tinto (RIO) was trading at $39.60. On Friday, it closed at $65.95, a gain of 67%. BHP has done even better, with Friday’s $25.88 up 73% on the low point last February of $14.95.

Sure, we can all rationalise what happened “after the event” and say that Chinese demand for metals such as iron ore didn’t fall away, but who really understands what is happening in China, let alone the iron ore price?

So given these challenges, how should a private investor play the resource majors like Rio Tinto? Well, before coming back to this question, let’s take a look at the company, which reported full year earnings last Thursday.

Rio’s strong full year result

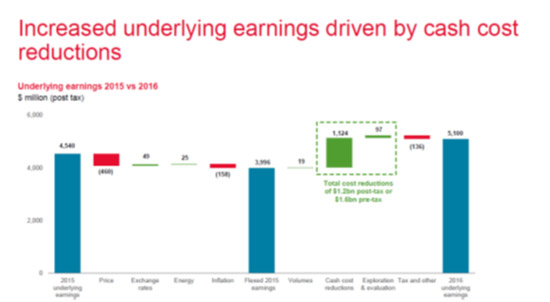

The most interesting part of RIO’s FY16 result was that all the improvement in earnings was driven by lowering the cost of production, a staggering $1.2bn ($1.6bn pre-tax) of cost savings. In fact, while commodity prices recovered in 2016, they were lower in aggregate than in 2015, and as the following chart shows, reduced earnings by $460m.

[1]

[1]

Underlying earnings of US$5.1bn for the year (RIO works on calendar years) were up 12% on the US$4.5bn in FY15. This was concentrated in the second half, as the impact of higher prices started to come through.

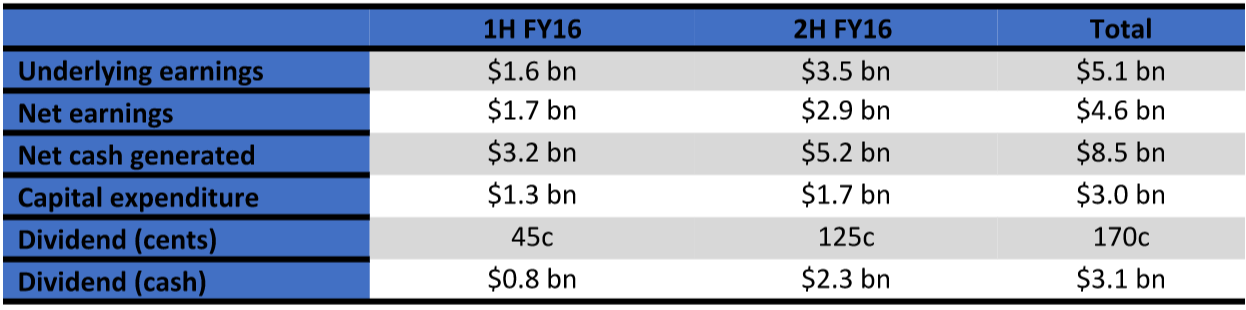

[2]

[2]

RIO lifted its dividend to US 125c in the second half, taking the full year payout to US 170c. At an exchange rate of 76.5 US cents and using Friday’s closing price of $65.95, this is an effective yield of 3.4%. The company also announced an on-market buyback of US$0.5bn, which will be used to buy back RIO shares that are listed on the London Exchange.

The cash generated from operations, together with some asset sales, allowed RIO to reduce net debt by US$4.2bn. Gearing now sits at a very comfortable 17%.

Pilbara iron ore largely drives RIO’s earnings, with the iron ore product group accounting for 76% of the group’s earnings. Aluminium contributed 16%, energy & minerals 10%, while the copper & diamonds product group slipped to a loss for 2016.

RIO has provided guidance that capital expenditure of $5.0bn will be incurred in FY17 and $5.5bn in each of FY18 and FY19, as it invests in three major growth projects – the Silvergrass iron ore expansion in the Pilbara, the Oyu Tolgoi underground copper mine in Mongolia and the Amrun bauxite project in Queensland. It says that it will generate additional free cash flow of US$5.0bn by the end of 2021 from productivity improvements.

What do the broker’s say?

As a group, the brokers are quite positive on RIO. According to FN Arena, they forecast earnings in 2017 of 417.7 US cents per share (up from 256.7 US cents in FY16), and have the dividend rising from 170 US cents to 240.5 US cents, a forecast yield of 4.8%. The consensus target price is $71.36, about an 8.2% premium to the current share price.

[3]

[3]

To be brutally honest, I don’t pay too much attention to broker target prices when it comes to resource companies, because they are so sensitive to the underlying commodity price forecast. And the brokers’ collective track record in forecasting commodity prices is not that strong.

However, there are two positives that can be taken away from this data. Perhaps most importantly, they don’t see any specific company issues. They believe that RIO is a well- managed company. And secondly, they see slightly more upside in RIO than its main Australian rivals, BHP or Fortescue.

How to play

Given the unpredictable and volatile nature of commodity prices, I think private investors have three main options when it comes to investing in resource companies.

Firstly, don’t invest. Choosing this option means that you accept that your portfolio will probably underperform in markets when commodity prices rise (as is likely to be the case if you have been underweight material stocks over the last 12 months). Conversely, your portfolio will probably outperform when commodity prices fall.

Secondly, take a “punt” on commodity prices and invest (or disinvest) as you see commodity prices changing. If you think the iron ore price is going to stay well supported, buy RIO.

Thirdly, take a neutral position and effectively have an index weight holding in the major miners like RIO. For example, RIO’s current weighting in the S&P/ASX 200 is 1.9%, while BHP is 5.4% and Fortescue is 0.7% – about 8% all up. There are also some second tier miners. To be neutral, you would have around 8% to 10% of your portfolio in these stocks (you probably don’t need all three).

I think you should discount the second option. You may have a bit of a punt when the stocks are being trashed (because you know the market almost always overdoes it), but generally, you leave any “punting” to something that is arguably a little more predictable.

Both the first and third options are valid, it just depends on your risk appetite. I prefer option 3 now that the companies have abandoned their crazy progressive dividend policies, because they are world-class producers, right at the bottom of the cost curve.

And I will probably stick to option 3, unless they go mad with acquisitions. Unfortunately, history shows that like many investors, these companies are hopeless at predicting commodity prices and they buy assets towards the top of the market and sell assets near the bottom.

If you are considering option 3, despite having a less diversified portfolio, RIO has to be right up there.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.