I thought for a change I’d write on a very well owned Australian stock that I am cautious on: Ramsay Healthcare (RHC).

To set the scene I think it’s worth reminding ourselves of high P/E stocks that have recently suffered material share price setbacks in Australia. The list would include Domino’s Pizza (DMP), Brambles (BXB), TPG Telecom (TPM), Vocus Group (VOC), Healthscope (HSO), Estia Health (EHE), Mayne Pharma (MYX), Sirtex Medical (SRX), Bellamy’s (BAL), Blackmore’s (BKL), IPH (IPH which I now recommend buying), Virtus Health (VRT), Monash IVF (MVF) and Japara Healthcare (JHC).

This list above is not all encompassing but just note how many so called “defensive” healthcare stocks are in this list of de-rated companies.

The true ‘defensiveness’ of an investment is basically a function of the price you pay for the company, not simply the sector it operates in. Quite frankly, most of the least “defensive” in price stocks are in so called ‘defensive’ sectors.

Over the last few years of ultra-low interest rates and QE, investors paid a higher and higher price (P/E, price to book) for so called “defensive” companies. This continued re-rating made defensive companies in reality quite risky, because the higher multiples meant the expectations on these companies grew higher and higher.

When expectations are high (in terms of very high P/E’s etc.), the risk of disappointment and capital losses increases. When you are priced for perfection you need to consistently deliver nothing less than perfection.

Australia is blessed with the fourth largest retirement savings pool in the world. However, we have the 17Th largest share market. The ASX200 is one of the most concentrated in the world, with 20 stocks making up 75% of the benchmark index. We then have 200 odd ore more Australian institutional investors trying to beat the index, and each other, on a daily basis.

What this all drives is extreme short-termism and a massive premium being paid for those companies “in vogue” and a massive discount being applied to those companies “not in vogue”. Similarly, analysts all recommend buying the “loved” and selling the “un-loved”.

All the stocks I list above were previously “in vogue”, yet failed to deliver the markets extremely lofty expectations. They are now in the “sin bin” as such and command share prices -25% to 75% below recent highs.

You all need to understand that the share price difference between being “in vogue” and the “sin bin” can be anywhere between -25% and -75%. The punishment for “small crimes” on the ASX is enormous. “Great” companies can become “hated” overnight. Think about it: -20% profit downgrade + -20% P/E de-rating = -40% share price (in a day).

Obviously at AIM, we do invest in some higher P/E ‘great’ Australian companies, Aristocrat (ALL) and Treasury Wine Estates (TWE) are two examples, because the AIM investment team and I have extremely strong conviction in the earnings outlook and management’s ability to execute. We also see low regulatory risk in those companies. Regulatory risk is the “black swan” that can truly sideswipe a higher P/E stock.

It would therefore be no great surprise that the Australian Healthcare sector has seen the most share price “blow ups” in recent times. Yes, we have the bullish narrative of the ageing population, but we have the perhaps more bearish narrative of private health insurance numbers dropping and highly indebted governments looking for budget cost savings. It’s fair to say any sector that is broadly reliant on government spending has regulatory risk in the current environment, and there’s no bigger cost for government than healthcare.

That brings me to Ramsay Healthcare (RHC), the $13.3b market cap leader of the Australian private hospital sector.

There are currently 8 buys, 4 holds and no sells on RHC from the analyst community. The “love” index is strong, based on historic performance.

Firstly, my argument isn’t that RHC is a “bad company”, far from it. My argument is that RHC shares currently do not reflect the growing risks to its earnings growth profile and P/E. I think there’s every chance RHC shares will be cheaper in six to 12 months’ time and the company has many similar characteristics to the examples above that experienced de-ratings.

Below are the four key reasons we are cautious on RHC.

[1]

[1]1. Valuation

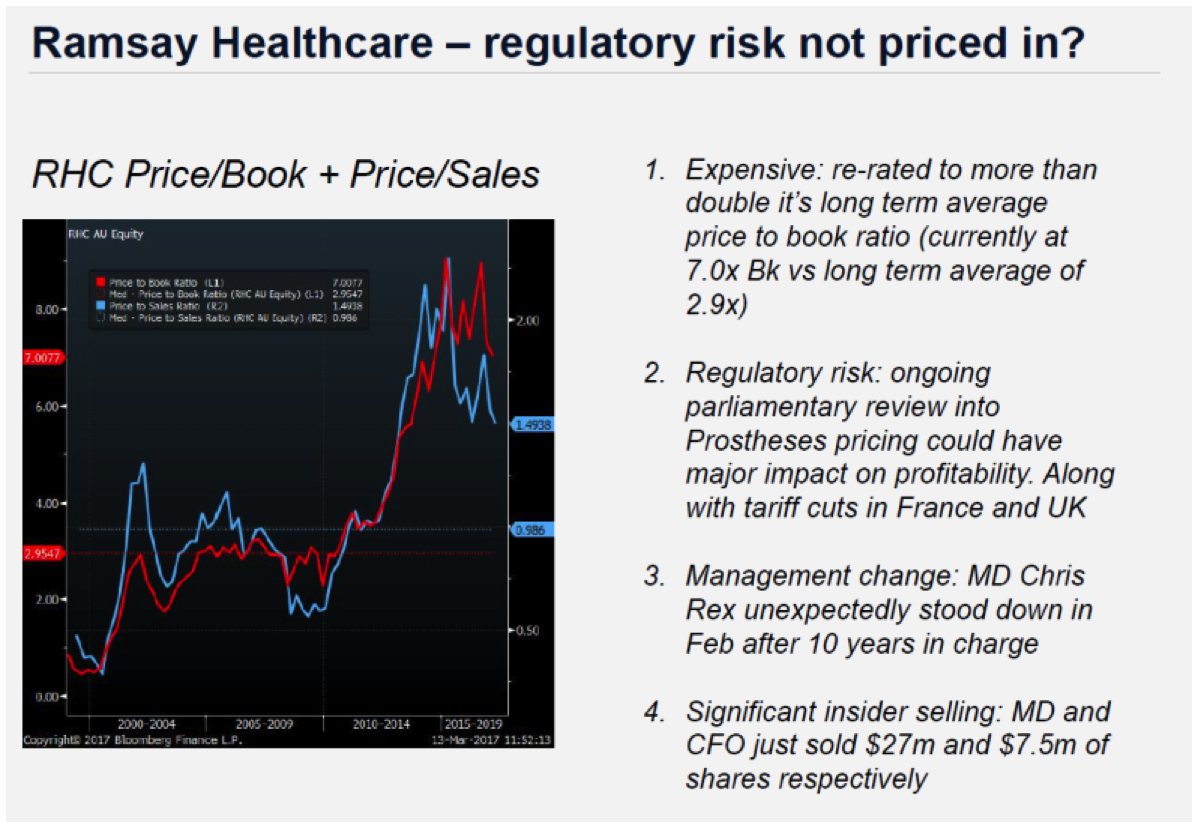

RHC trades at a significant premium to the market and a significant premium to its own historic trading range. Since listing RHC has traded at an average Price to Book of 2.95x – at current prices RHC is trading at 7.3x Price / Book. This re-rating has been driven partly by improving returns in its Australian hospitals division, but also by the market’s willingness to pay premium multiples for stocks with perceived defensive growth in a low growth/low interest rate environment.

RHC price to book since listing

[2]

[2]2. Regulatory change

We believe the very high returns RHC generates from its hospitals are under threat. We have seen tariff cuts implemented in the UK and France, which are pressuring returns from RHC’s foreign assets. We now believe increased regulatory scrutiny in Australia may have the same effect on RHC’s highly profitable Australian hospitals.

Specifically, we are following closely the current parliamentary review into prosthesis pricing in Australian private hospitals, which we believe has the potential to have a material negative impact on RHC’s earnings.

Prosthesis pricing regulations in Australia are complicated (to put it mildly). Prices for prostheses for privately insured patients in Australia are government regulated (fixed) and private health insurers must reimburse at this fixed rate. There is plenty of evidence to suggest that these regulated prices are, in many cases, significantly higher than market based prices paid in comparable markets. And there is also evidence to suggest that private hospital operators accept rebates from device manufacturers, which allows them to share the benefit of these inflated prices, at the cost of higher insurance premiums (or ultimately Australian taxpayers). This opaque earnings stream is in jeopardy from potential regulatory change.

3. Unexpected management change (industry-wide)

In the past two months we have seen long standing Managing Directors step down from both of the listed private hospital operators, at a time when regulatory change seems to be accelerated.

In February, the highly regarded Chris Rex unexpectedly stepped down as MD of RHC after a decade in charge. This week we have seen Robin Cooke, the MD of Healthscope (HSO), follow Rex’s lead and step down from the position he has held for the past seven years. So in the space of two months, two MDs of Australia’s listed private hospital operators have both stepped down. Whilst we respect the right of both to make life decisions, it is often a red flag for us to see management change in business/industries.

4. Insider selling (industry-wide)

In addition to management change we have seen significant inside selling at both Ramsay and Healthscope. In April 2017, outgoing MD Chris Rex sold approximately $27m worth of shares whilst CFO Bruce Soden also sold approximately $7.5m worth. Admittedly, Chris Rex retains a significant holding in Ramsay. In August last year, before the profit warning, Healthscope MD Robert Cooke sold $4.3m worth of HSO shares (around 80% of his holding at the time). This is often another red flag and was also evident in several of the highly published de-ratings in the list mentioned above.

I understand most holders of RHC are sitting on huge capital gains (and potential tax bills), but so were many of the shareholders of the companies I mention at the top of the note. A potential CGT bill is never a good reason not to take some profits.

My view is there are clear, fundamental catalysts for RHC’s premium rating to come down a notch or two in the months and years ahead. It’s worth remembering that its largest competitor, Healthscope (HSO), recently fell -50%.

Finally, from a technical perspective, RHC recent broke down through it’s 50-, 100-, and 200-day moving averages.

RHC is a large cap Australian stock I am cautious on at current prices. Historic performance is not always a guide to future performance.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.