A relatively uninspiring company reporting season, together with a negative lead from the USA, led to the market retreating in February. This came after a very strong start to the year.

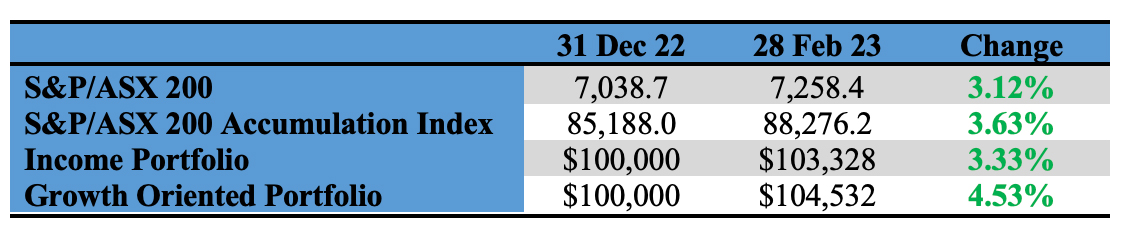

Although giving back some of their earlier gains, our model portfolios outperformed in February. Both are showing solid returns for the year, with the growth portfolio currently outperforming the benchmark index by 0.90%.

There are two model portfolios – an income-oriented portfolio and a growth portfolio.

The objectives, methodology, construction rules and underlying economic assumptions can be referenced here: (see: https://switzerreport.com.au/our-portfolios-for-2023/ [1]

These are long-only model portfolios, and as such, they are assumed to be fully invested at all times. They are not “actively managed”, although adjustments are made from time to time.

In this article, we look at how they have performed so far in 2023. To do so, we will start by examining how the overall market has fared.

All sectors up for the year

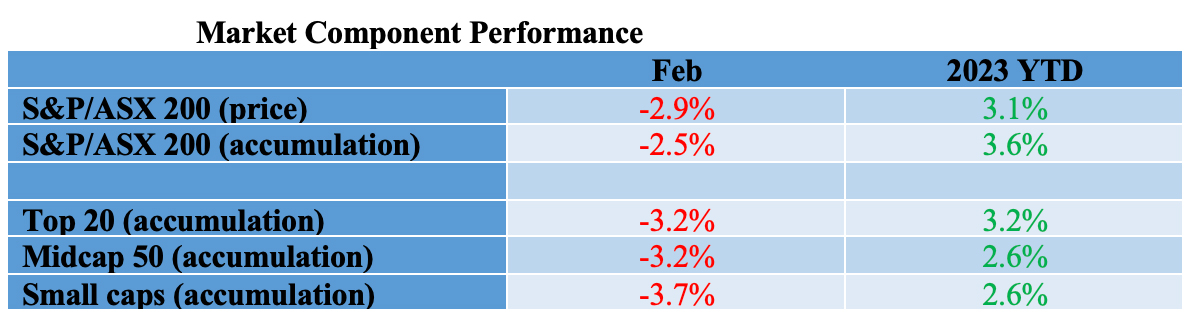

The tables below show the performances in February and for the calendar year to date for the components and industry sector that make up the Australian market. Overall, the market (as measured by the benchmark S&P/ASX 200) is up by 3.1% and when dividends are included, by 3.6%. In February, the market lost almost 3.0%.

The top 20 stocks (which includes the 4 major banks, Macquarie, Woolworths and major miners in BHP, Rio and Fortescue) lost 3.2% in February. Small caps, which measures the performance of stocks ranked 101st to 300th by market capitalization, lost 3.7% in February. For the year, it is marginally behind the overall market with a return of 2.6%.

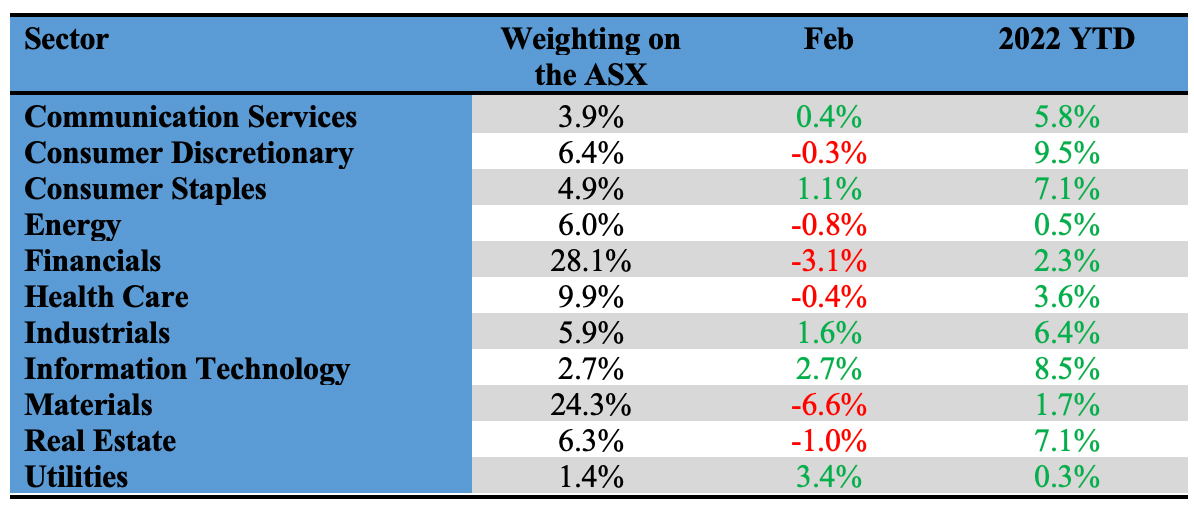

With the industry sectors, all are up on a year to date basis. Consumer discretionary leads with a return of 9.5% followed by information technology with 8.5%. The very small utilities sector and the energy sector are the laggards with returns of 0.3% and 0.5% respectively.

The largest sector on the ASX, financials, which makes up 28.1% by weighting, lost 3.1% in February to be up 2.3% in 2023. The second largest, materials, lost 6.6% in the month. Interestingly, most of the February loss was reversed in the first three days of March.

Industry Sector Weighting & Performance

Portfolio Performance in 2023

The income portfolio to 28 February has returned 3.33% and the growth oriented portfolio has returned 4.53% (see tables at the end). Compared to the benchmark S&P/ASX 200 Accumulation Index (which adds back income from dividends), the income portfolio has underperformed by 0.30% and the growth portfolio has outperformed by 0.90%.

Income Portfolio

The objective of the income portfolio is to deliver tax advantaged income whilst broadly tracking the S&P/ASX 200.

The income portfolio is forecast to deliver an income return of 5.0% (based on its opening value at the start of the year), franked to 80.3%. Dividends declared during the February reporting season were marginally better than forecast.

In the month of February, the income portfolio returned -1.80%. This outperformed the benchmark index by approximately 0.65%. For the year, it has returned 3.33%, which is 0.30% behind the index.

The portfolio is moderately overweight financial stocks and underweight the more growth oriented sectors such as information technology and health care. In a strong bull market, the income portfolio will typically lag the market, and in a bear market, it is likely to outperform.

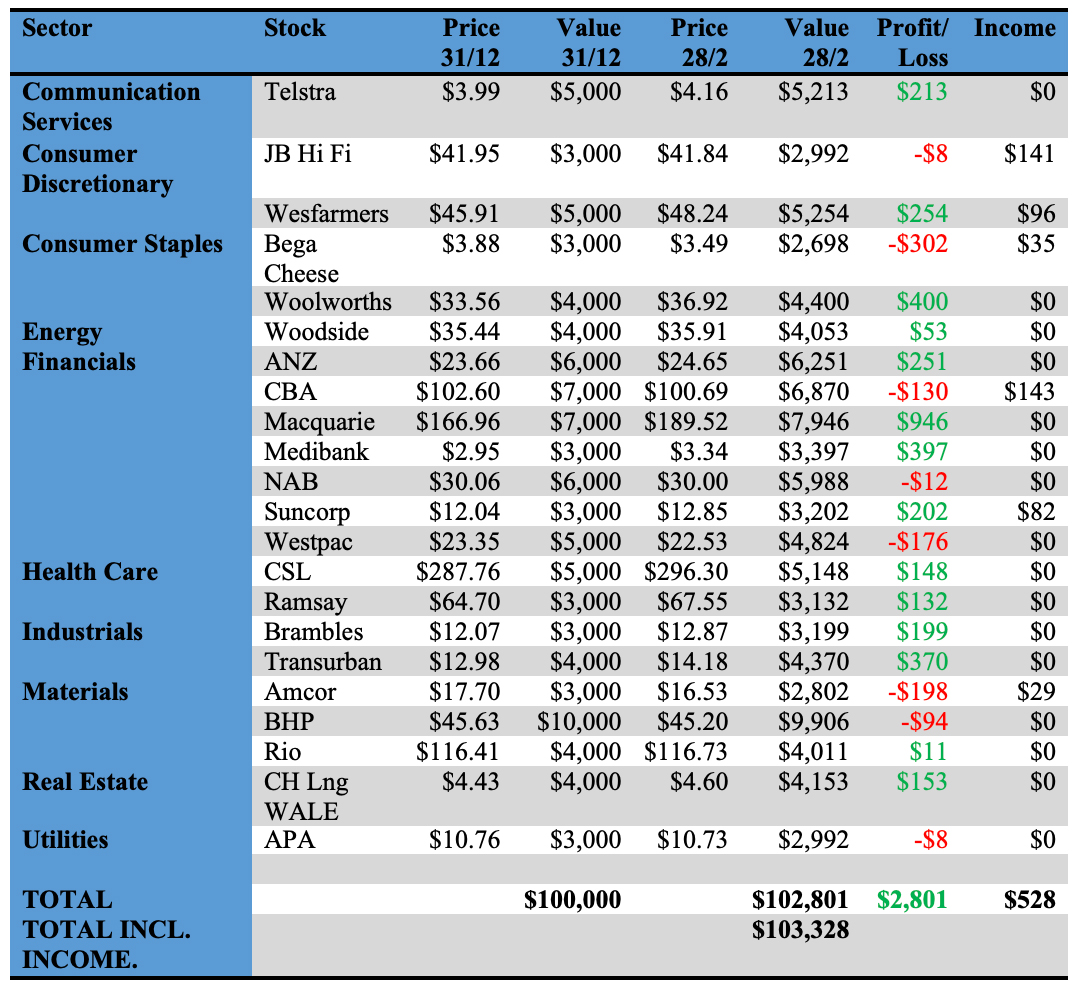

The income biased portfolio per $100,000 invested (using prices as at the close of business on 28 February 2023) is as follows:

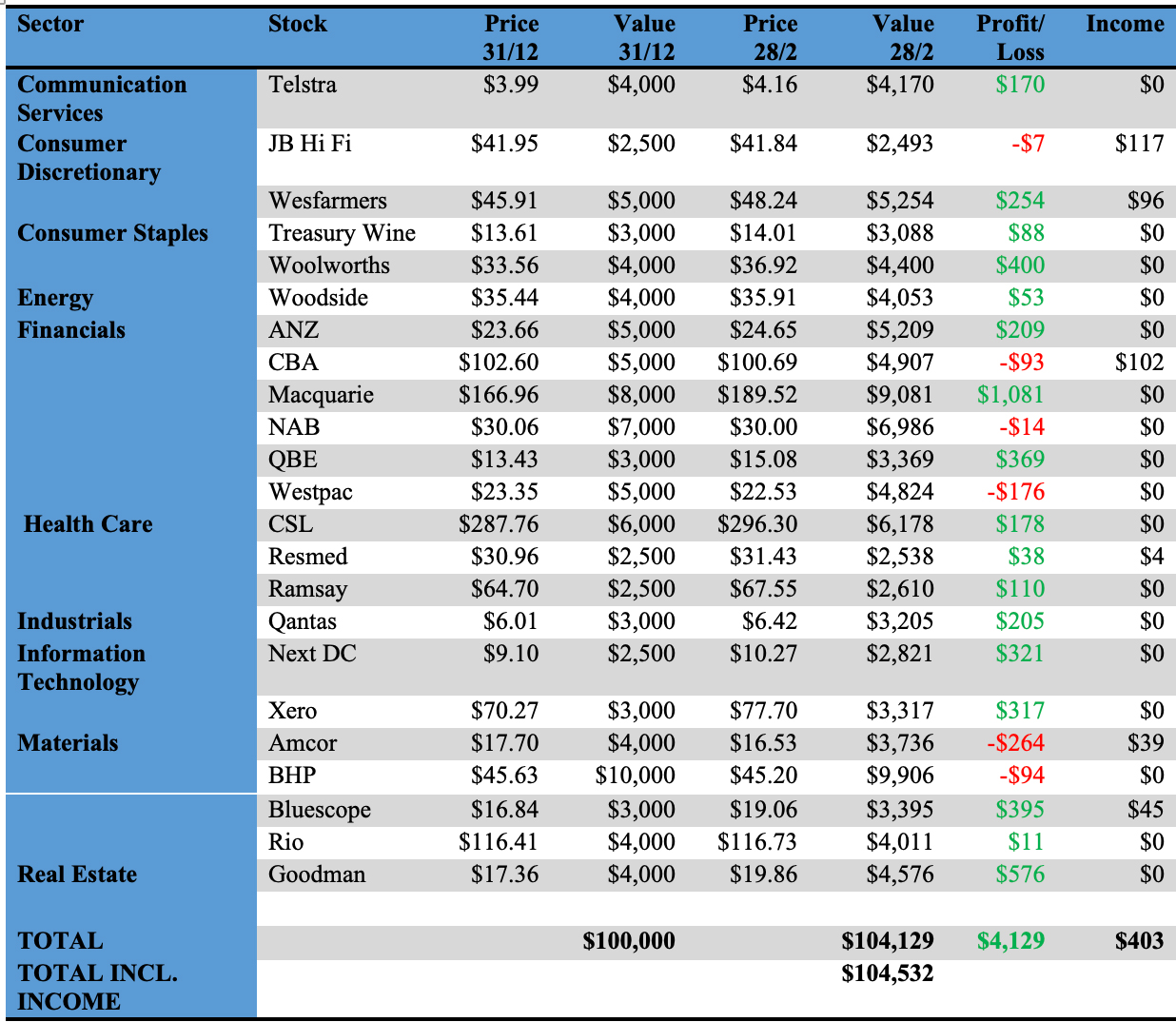

Growth Portfolio

The objective of the growth portfolio is to outperform the S&P/ASX 200 market over the medium term, whilst closely tracking the index.

In February, the growth portfolio delivered a return of -2.00% to outperform the benchmark index by 0.45%. Year to date, it has returned 4.53%, outperforming the benchmark by 0.90%.

The portfolio is moderately overweight financials, health care and information technology. It is moderately underweight industrials, real estate and utilities. Overall, the sector biases are not strong.

Our growth-oriented portfolio per $100,000 invested (using prices as at the close of business on 28 February 2023) is as follows:

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.