The largest IPO to hit the Australian market in some time, Viva Energy, kicks off this week. Viva Energy, which is largely Shell Australia’s old downstream energy assets including petrol service stations and the Geelong refinery, is seeking to raise almost $3 billion from investors. Upon listing, Viva Energy will have a market capitalisation of around $5 billion.

Here is what I think of the IPO.

Viva Energy

Viva Energy is one of Australia’s leading integrated downstream petroleum companies. Its underlying operations were formerly part of the Shell group, which has operated in Australia for over 110 years.

In 2014, Swiss based energy and trading commodities company Vitol, via its consortium Vitol Investment Partnership, acquired the Shell Australia downstream business and renamed the business Viva Energy.

[1]

[1]

Viva Energy operates across two main business segments. The Retail, Fuels and Marketing segment consists of retail and commercial operations. In retail, Viva Energy supplies and markets fuel products through a national network of 1,165 retail service stations and sites. This includes 713 Coles Express sites, 161 Shell branded sites and 192 Liberty branded sites. By number of sites, it ranks third (Caltex is number one with approximately. 1,900 sites, BP is second with approximately 1,400).

In commercial, Viva Energy is a supplier of fuel, lubricants and specialty products to commercial customers in the aviation, marine, transport, resources, construction and manufacturing industries. It has a 37% market share in aviation fuels and 48% market share of marine fuels.

The second business segment is refining where Viva operates the Geelong refinery, one of four remaining refineries in Australia. The Geelong refinery converts imported and locally sourced crude oil into petroleum products including gasoline, diesel, jet fuel, aviation gasoline, gas, solvents, bitumen and other specialty products. The Geelong refinery supplies about 11% of Australia’s total fuel demand or approximately 50% of Victoria’s total demand.

Excluding the supply, corporate and overheads segment, relative contributions to Group EBITDA in FY17 were:

- Retail fuels and marketing: 51%

- Commercial: 26%

- Refining: 23%

Viva also owns 38% of Viva Energy REIT (ASX: VVR) – a $1.5 billion market cap property trust that owns service station property assets that it predominantly leases to Viva Energy – and 50% of Liberty Oil, an independent fuel retailer and wholesale distributor in Australia with a strong presence in regional markets.

Investment thesis

The thesis for investing in Viva Energy is as follows:

- Australia is an attractive fuels market supported by stable fuel demand and sustained convenience market growth. Viva supplies approximately one quarter of Australia’s fuel needs;

- Viva has a leading retail network with strong brand recognition. Network scale and strategic relationships with Coles and Shell support earnings stability;

- Viva employs a “capital-light” and shared risk operating model for its retail network, with many of the sites leased from Viva Energy REIT or other third-party owners;

- It has a diversified revenue base in its commercial and specialty businesses with strong market positions in key industry sectors;

- It owns and operates the second largest refinery in Australia, which is adjacent to one of the larger fuel markets. The refinery has been profitable since acquisition;

- It has control of critical chain supply infrastructure, allowing it to operate a cost-efficient supply chain;

- An experienced and capable management team led by CEO Scott Wyatt; and

- A track record of strong financial performance. Underlying pro-forma EBITDA has grown from $535.2 million in FY15 to $634.3 million in FY17 and is forecast to grow to $661.3 million for the 12 months ending 30 June 2019.

In terms of growth, Viva cites the following opportunities/initiatives:

- Extension of the retail petrol site network to fill current network gaps and provide access to population growth corridors;

- Grow the fuel margin, through the provision of loyalty offers, product mix and premium fuels, and operation under premium branding;

- Grow the convenience and non-fuel margin;

- Expansion of commercial markets; and

- Improving the refining potential by improving reliability.

On the risks side, the directors of Viva don’t seem that concerned about the rise of electric vehicles, citing research from Wood Mackenzie Australia that estimates that electric vehicle penetration in Australia in 2020 will only represent 0.3% of the total vehicle fleet.

The offer

The offer is a sell-down by the Vitol Investment Partnership, which purchased the business from Shell in 2014. After selling between 50% and 60% of the company, they will keep 50% to 40% and have two appointees on the board.

All the proceeds of the offer of $2.4 billion to $3.1 billion, less costs of circa $100 million, will be paid to Vitol.

While Vitol has said that its retained investment in Viva is “strategically significant to it and that it has no current intention to reduce the extent of it”, its remaining shares are not subject to any escrow arrangements and potentially could be sold at any time.

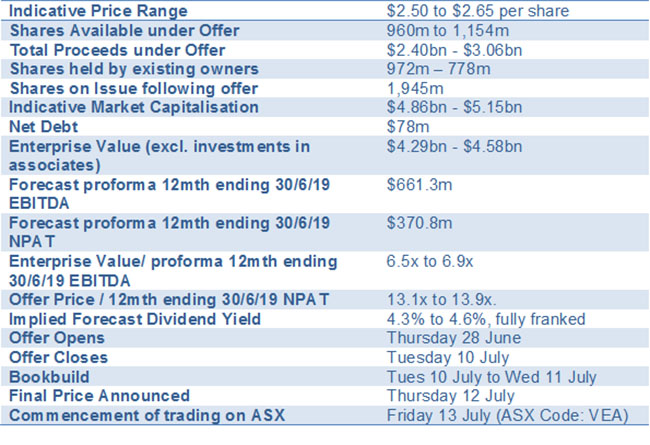

The offer is due to open on Thursday. An indicative price range of $2.50 to $2.65 per share has been set, with the final price determined in an institutional book-build on 10 July. All applicants will pay the final price, with retail applicants bidding a dollar value (minimum $2,000 and then in multiples of $500) and advised after the final price has been set how many shares they are to receive.

Details of the offer are as follows:

[2]

[2]

Pricing

As the table above shows, the offer is being priced at a multiple of around 6.5 times to 6.9 times the next 12 months’ earnings (enterprise value to EBITDA). This is said to be a discount to its nearest listed competitor, Caltex, which is trading around 7.6 times. When tax, interest, amortisation and depreciation are considered, Viva is being priced at a multiple of 13.1 to 13.9 times earnings (Caltex is trading at 13.2 times).

The directors are forecasting a dividend yield of 4.3% to 4.6%, which is expected to be fully franked. This is based on a payout ratio of 60% of underlying NPAT. Caltex, which has a payout ratio of 50%, is forecast to yield 3.7% (also fully franked).

In terms of earnings’ sensitivities, the PDS identifies six key factors that could impact profit: fuel volumes, fuel margin, refining margin, exchange rates, crude oil prices and operating expenses.

My view

Viva is being sold as a solid, reasonably low-risk business with a track record of financial performance. It is priced at a discount to its nearest competitor, Caltex. It has almost no debt, and strong cash flow post capex to sustain a dividend payout ratio of around 60% (and reasonably attractive dividend yield).

This all said, I just can’t get that excited by the investment thesis and If I don’t participate, I am not going to shed too many tears. It is a big IPO, and while S&P/ASX 200 inclusion in due course means that the index funds will need to participate, my hunch is that investors will demand more of a discount and it will price at the bottom end of the range.

The offer opens on Thursday. Brokers involved include Merrill Lynch, Deutsche Bank, UBS, Morgans, Bell Potter, JB Were, Ord Minnett and Wilsons.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.