[table “275” not found /]

Those who might be worried about the US economy as the first domino to fall in what becomes a chain reaction of economic and market collapses in 2017, need to put away the worry beads, with the US job-making machine back in business in April!

US markets were up overnight, and while the Dow was limited by IBM, which disappointed, the other indexes reacted positively to the 211,000 jobs created last month, which pushed unemployment down to a low 4.4%!

Better still, average wages rose 0.3% and, all up, this number trumps the disappointing result in March. And if you add that bad job result to the weaker than expected annualised economic growth figure of 0.7% for the first quarter, then you have reason to start doubting the outlook for the Yanks.

The following sums up the sensible take on the US labour market and economy:

“Today’s numbers from the jobs report represent a strong bounce-back, following the disappointing figures recorded the month prior and is [a] testament to a growing economy,” said Kully Samra, managing director at Charles Schwab to CNBC.

Couldn’t have said it better myself. And it gives more certainty to the notion that the Fed will raise interest rates at least twice this year, which again reinforces the optimist’s view that stocks are the go for 2017, even if there’s a little bit of “sell in May and creep away tendencies”.

On the local front, it has been four days of losses and the elusive 6000 level on the S&P/ASX 200 index (after reaching 5956.5 on Monday – a two-year high) keeps defying Aussie investors, as lower oil and iron ore prices continue to help gravity exert itself on the index.

In case you missed it, the materials sector slumped 4.4% and iron ore had a shocker on Thursday night, giving up 5% to get as low as $US65.20! However, this chart does show that you need to keep this iron ore price fall into perspective.

I don’t like what I see and Treasurer Scott Morrison would like it less, as iron ore prices affect the profits and the taxes he gets from the likes of BHP and Rio.

Only this week, we learnt that he wants to keep BHP as the Big Australian, defying the US hedge fund, Elliot Associates, which wants to break it up and have it exclusively listed on the UK stock market.

Apart from employing 16,000 Aussies here, the company has paid $65 billion in taxes over the past decade!

That said, companies delivering good news (such as Macquarie) show what happens when a company beats expectations. The Big Mac finished up over $3 for the day to be pressing the $95 level.

Adding pressure is the old “sell in May” rule that coincides with our market’s 12-month forward price-earnings ratio, still at 15.4 times, while our long-term average is only 13.9!

This week I asked AMP Capital’s Shane Oliver if this market weakness is linked to current or pending economic weakness but he pretty well hit that idea to the boundary. And even News Limited’s Terry McCrann, who doesn’t do positivity easily, also admitted that he is becoming more positive about our economic outlook and that of the globe.

Summing it up neatly was Bell Potter’s Richard Coppleson, who recommended “sell the banks” early in the week but he quickly added that he thought they would be higher by year’s end!

Apart from Macquarie, the banking story was not great reading, though I think there was an overreaction but heck, stock markets do that, don’t they? ANZ and NAB lost 6.4% and 4.4% respectively, while the CBA and Westpac lost 3.4%.

Right now, I have no deep confidence about what the market does in coming weeks but I do believe in Coppo’s call that the banks will be higher. The same goes for the overall market.

What I liked

- Paul Rickard’s table showing that April saw the mid-cap stocks up 1.7% and 7.1% for the year to date. You might recall when the big caps took off last year and into the early part of this year, I suggested eventually unfairly dumped smaller quality stocks had to make a recovery. I bet small caps show some form later in the year, as they are up only 1.2% for the year to date and were down 0.3%!

- Telstra shares rising 4.3% for the week – its dumping has been excessive and I bet with June 30 looming and the new super rules encouraging would-be retirees to get $580,000 into their funds before it’s too late, it could help some big name stocks that SMSF trustees like.

- The euro going higher on the likelihood of Emmanuel Macron’s likely win in the French election this weekend, though it will make upcoming holidays to Italy more expensive! The economist in me has outweighed the money-conscious traveller I can be, much to the annoyance of my life-loving wife!

- The RBA increased its economic growth forecast for the Oz economy to 2.75-3.75% in June 2018, which is around a quarter of one percentage point higher than previous forecasts.

- This Craig James of CommSec take on the RBA ‘no rate change’ decision on Tuesday: “The Reserve Bank Board was seemingly a little downbeat on the economy at the April meeting. Not so at the May meeting. The Reserve Bank has confirmed that economic growth will strengthen over the next couple of years to above 3 per cent – faster than the “speed limit” of just under 3 per cent. And inflation will increase as the economy strengthens. In short, don’t expect a cut in official rates.”

- The local Performance of Services index rose by 1.3 points to 53 in April. The index remains over 50, signifying expansion of the services sector.

- The Performance of Manufacturing index rose by 1.7 points to 59.2 in April – a reading just below 15-year highs. A reading above 50 indicates that the sector is expanding. This was the seventh consecutive month of expansion.

- The CoreLogic home price data showed a slowing in Sydney and Melbourne in April, with falling prices for units suggesting that these two property markets may be starting to cool.

- The Euro-zone PMI data showed that factory activity hit a six-year high in April.

- The US House of Representatives narrowly voted to repeal major portions of Obamacare and replace it with a Republican healthcare plan, now sending it to the Senate. This is a plus for those hoping that President Trump can hold sway over the Congress on tax.

- The US Federal Reserve kept the fed funds rate unchanged at 0.75%-1.00%. The accompanying FOMC statement said the slowdown in March quarter economic growth is likely to be “transitory”. The Fed still expects the economy to expand at a moderate pace, noting that business investment has firmed and job gains are solid. (CommSec)

- US factory orders rose 0.2% in March.

- According to Thompson Reuters, as the European earnings season nears the halfway mark, 80% of companies have beaten analyst expectations for revenue.

What I didn’t like

- New motor vehicle sales totaled 83,135 in April, down 5.1% on a year ago but the result was affected by the timing of Easter holidays. These car sales have been in record high territory for some time, so I’m not too worried.

- The manufacturing Purchasing Managers’ Index in China eased from 51.8 to 51.2 in April (forecast 51.6). The services index eased from 55.1 to 54.0. These are still OK and sector expanding numbers but they partly explain softer commodity prices as “is China slowing” questions re-emerge, as they always do.

A final like

It’s Budget week ahead and, apart from the fact that time is seemingly moving at a too fast pace, as someone who loves this annual economic show-and-tell from Canberra, I can’t wait for the adrenaline pump of it all!

Beam us up, Scotty!

The week in review:

- I explained why it might be a “buy in May and stay [1]’’ year for stocks!

- Both the income and growth portfolios returned around 1% in April and more than 5% for the first four months of the year. Read Paul Rickard’s portfolio recap here [2].

- James Dunn revealed 5 ETFs [3] for investors looking for European exposure.

- The brokers placed BHP Billiton [4] in the good books this week, while Blackmores was downgraded.

- The Super Stock Selectors liked Fisher & Paykel Healthcare [5] this week, but not Whitehaven Coal.

- Charlie Aitken explained why he thinks one of the biggest companies in the world, Apple, is caught in a “passive bubble [6]”.

- Tony Featherstone [7] considered whether poultry stocks have wings.

- In our second broker report, RCG Corporation was in the good books while ResMed [8] was in the not-so-good books.

- And Switzer Super Report subscriber Jeffrey Tripp gave us a sneak peek into his very own SMSF [9].

Top stocks – how they fared

What moved the market?

- Earnings results from the major banks. ANZ’s half-year cash profit came in slightly weaker-than-expected, while NAB’s results were in line with expectations.

- Falls by the miners on the back of softer commodity and oil prices.

- The FOMC minutes, which reaffirmed expectations that the US Fed will hike rates twice in 2017.

- And US earnings results.

Calls of the week

- The ACCC announced that it won’t be regulating mobile roaming – a much-needed win for Telstra!

- The Fed Government announced that it would build Sydney’s second airport at Badgerys Creek after Sydney Airport declined the Government’s offer for the project. Read why Paul Rickard thinks Sydney Airport [10] is a long-term sell.

- And as widely expected, the Reserve Bank kept the cash rate on hold at 1.5%. The US Fed also kept interest rates steady, in their target band of 0.75% to 1%.

The week ahead

Australia

- Monday May 8 – Building approvals (March)

- Monday May 8 – ANZ Job advertisements

- Tuesday May 9 – Weekly consumer confidence

- Tuesday May 9 – Federal Budget

- Tuesday May 9 – NAB Business survey (April)

- Tuesday May 9 – Retail trade (March)

- Friday May 12 – Tourist arrivals (March)

- Friday May 12 – Credit & debit card data (March)

Overseas

- Monday May 8 – US Employment trends (April)

- Monday May 8 – China trade (April)

- Tuesday May 9 – US NFIB business optimism (April)

- Tuesday May 9 – US JOLTS job openings (March)

- Wednesday May 10 – US Trade prices (April)

- Wednesday May 10 – China inflation (April)

- Thursday May 11 – US Producer prices (April)

- Friday May 12 – US Consumer prices (April)

- Friday May 12 – US Retail sales (April)

Food for thought

- It always seems impossible until it’s done.

Nelson Mandela

Last week’s TV roundup

- Is the stock market going to kick through 6000 soon? For a look at the market, the banks, Woolworths and more, Contango Asset Management’s George Boubouras joins the show [11].

- Simon Bond [12] from Morgans joins the show to discuss the tech and telco stocks he’s watching right now.

- With iron ore prices falling and some softer economic data out of China, has our economic optimism been slightly misplaced? AMP Capital’s Shane Oliver joins the show [13].

- David Buckland [14] from Montgomery Investment Management joins Super TV for a look at the stocks he’s watching and how the market is performing right now.

Stocks shorted

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

This week the biggest mover was Vocus Group, with the proportion of its shares sold short increasing by 1.30 percentage points to 14.27%.

[15]

[15]Source: ASIC

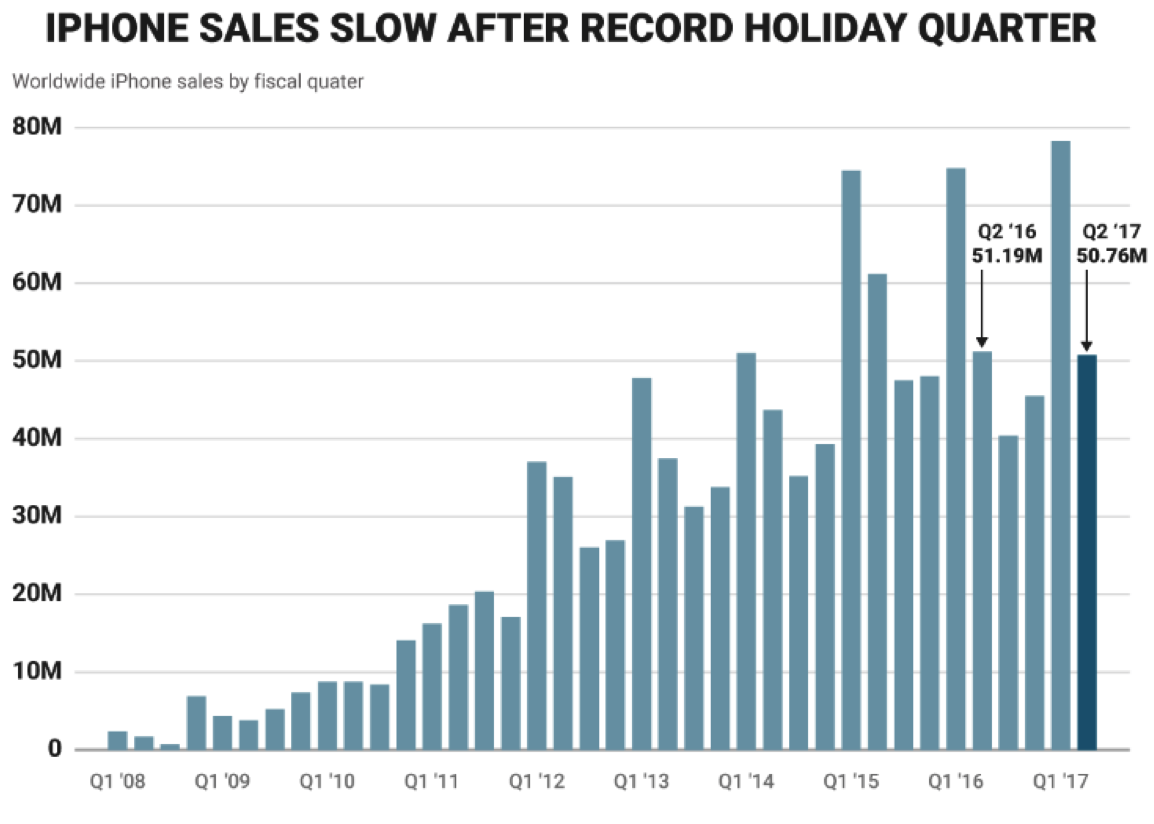

Chart of the week

[16]

[16]Source: Apple, Statista, Business Insider

Apple sold 50.8 million iPhones during the latest quarter, just below expectations of around 52 million, and flat year-over-year. Are we at “peak smartphone”, as Charlie Aitken suggests? Read his article here [6].

Top five most clicked stories

- Peter Switzer: Maybe it’s a ‘buy in May and stay’ year for stocks! [1]

- Paul Rickard: Portfolios up in April [2]

- Rudi Filapek-Vandyck: Buy, Sell, Hold – BHP upgraded [4]

- Charlie Aitken: Apple and the “Passive Bubble” [6]

- Staff Reporter: Buy, Sell, Hold – what the brokers say [8]

Recent Switzer Super Reports

- Thursday 4 May 2017: Beware Apple? [17]

- Monday 1 May 2017: Stay in May? [18]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.