The best thing about being a global fund manager is the ability to invest for Australians outside of Australia in stocks and sectors they simply can’t get exposure to in the domestic equity market. The biggest sector missing in the domestic equity market is technology, with the vast bulk of the world’s most important and most profitable technology companies listed in the USA.

Last year I introduced you to the concept of the “MAFIA”. That being Microsoft (MSFT), Alphabet (GOOGL), Facebook (FB), IBM (IBM) and Amazon (AMZN). I believed then and I believe now these are must own companies for any portfolio that seeks to replicate the future, not the past.

Interestingly, many Australians I speak to say “how could you own any of those US tech stocks, my broker says they are SO EXPENSIVE”. Ahh, they are ‘expensive’ at a historic P/E level because they are GROWING so fast at the top line.

However, the way I look at stocks they certainly aren’t expensive if they continue to deliver the growth the market expects from them. These companies are becoming more and more dominant and extracting more and more economic rent at very high margins from global consumers and global businesses.

To put this in context, the ASX is the home of stupidly expensive industrial stocks. Lets be clear, there is way too much money (compulsory superannuation) chasing way to little growth, driving huge P/E premiums for anything that has short-term growth.

The problem with that, as we have seen recently, is if an ASX listed “growth stock” even puts the slightest foot wrong, they get absolutely smashed. Recent examples would be Aconex (ACX), Brambles (BXB), TPG Telecom (TPM), Vocus (VOC) and Sirtex (SRX) to name a few.

On the ASX we are so devoid of true “technology companies” that a fast food company, Domino’s (DMP), is considered a “tech stock”. That’s actually a dangerous joke. Sure, DMP has used technology to enhance its product and win greater market share, but it’s not like DMP invented GPS tracking and receives royalties!

Don’t get me wrong, DMP management have executed brilliantly but they are now priced for it. If the market one day woke up and decided DMP was a consumer discretionary stock and not a technology stock, the share price would be 50% lower. That’s the risk you take by limiting yourself to the domestic equity market.

At least when I am investing in the US tech “MAFIA” for my unit holders, I know I’m not going to wake up and find one of those stocks de-rated to some other sector!

Last week Microsoft, Amazon, IBM and Facebook all delivered great quarterly numbers. They were just excellent on all fronts and it seems analysts continue to underestimate the revenue power of cloud storage and social media platforms.

Today I thought I’d give a summary of the Facebook result. I’ve also included the PDF of the FB investor presentation that you may find interesting.

Facebook (FB.US)

[1]

[1]Once again (for the fifth time in a row) Facebook posted >50% YoY (year on year) top line growth and in so doing beat street estimates. And it is highly profitable, turning 52c of every dollar of revenue into operating profit (GAAP), a record. KPIs continue to impress with DAUs (Daily Average Users) now reaching 1.227B people, growth of 18% YoY, and of this 93% are mobile DAUs, growing 23% YoY. MAUs (Monthly Average Users) now total 1.86B and on track to hit 2 billion people in the second half of this year.

These metrics, not dissimilar to the revenue trajectory, all accelerated for the fourth quarter in a row. 4Q advertising revenues of $8.63B beat consensus (Factset) $8.31B, with Mobile advertising revenues of $7.25B beat consensus $7.12B. Non-GAAP operating margin is 63.5% above consensus 60.4%, and cash from operations of $4.93B is above estimates of $4.4B.

So, and even with difficult comps given the strong F4Q15 numbers, Facebook is enjoying strong consumer engagement and advertiser demand. Mobile advertising is the growth driver and the key platform monetisation tool and this is evident from the simple fact mobile ads are now 84% of total ad revenue. This in itself represents staggering +61% YoY growth with the triple-headed strategy of ad format innovation, targeting and measurement continuing to deliver strong ROI for advertisers on the demand side. The usage stats of user growth and time spent combined with ad load management contributed to Facebook’s strong performance on the supply side. Within the strategy, Facebook is now attacking the video opportunity much like it did in mobile originally. Video is the new file format for delivering richer kinds of content on mobile. Made possible by the large installed base of active smartphones, fast processors, fast networks and unlimited data, video becomes the easiest content to consume and offers deep engagement.

So much mobile browsing now happens on the Facebook news feed it is essentially the primary mobile web browser and video can become the preferred method of content and context in a social setting. Instagram stories has already reached 25% penetration rate of the Instagram install base after just five months of launch. WhatsApp continues to grow quickly, recently hitting 1.2B active users, 50B messages sent per day (more than all SMS messages across the globe) and has just added video calling to the service. Management is approaching video monetisation carefully, which reminds us of the exact policy deployed on mobile and on Instagram, which ultimately proved highly monetisable. New formats such as mid-roll video ads could be highly successful given the engagement opportunities referenced above in our view.

Tempered stock price reaction is likely the result of 2017 set as an “aggressive investment year” with non-GAAP expenses to grow 47-57% YoY with increased investment across R&D, content, sales and marketing. But then 2016 was set up as a significant investment year also, and delivered incredible growth, monetisation, user engagement and record profits.

Facebook’s focus on remaining at the forefront of the innovation curve is the right one in our view and given our views on the opportunities for changing media consumption, the rise of Artificial Intelligence, voice AI interfaces, and VR applications, it is essential for leading technology companies to remain at this end of that innovation curve. And remember, five years ago, Facebook wasn’t even a public company.

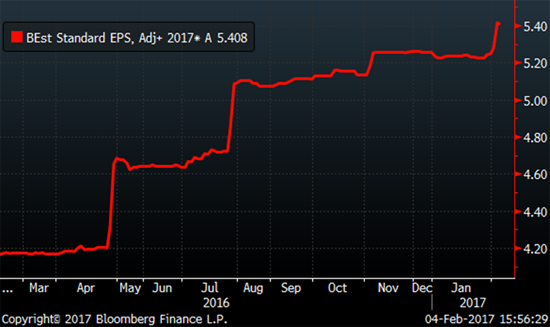

The stock remains in an earnings upgrade cycle. Below is the 2017 consensus EPS estimate.

[2]

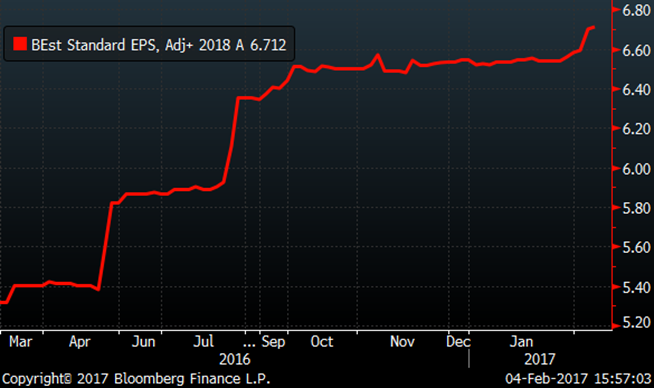

[2]2018 consensus EPS is also being revised up.

[3]

[3]On consensus forecasts alone the view is FB will deliver +25% EPS growth. That is great growth for a $400b market cap company.

The 2017 P/E is 24.2x, which would appear cheap versus Domino’s (DMP) 44x P/E for FY17!

The “MAFIA” continues to deliver. Do you own any exposure? The tables below remind you of FB’s structural growth and cash generation.

[4]

[4] [5]

[5] [6]

[6]Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.