There was a story last year about an elite Sydney private school using a hypoxic chamber that can simulate training at up to 3,000 metres above sea level. Like elite sporting clubs, the school is using latest technology to help its star athletes train and recover.

Critics lambasted the school’s excessive facilities and government funding. Nobody gave a second thought to schools and junior clubs using increasingly sophisticated sporting equipment – the type professional clubs have used for the past decade.

This is a powerful trend for Catapult Group International (ASX: CAT), a leading provider of athlete monitoring and analytics that listed on the ASX in late 2014. And further confirmation that fitness technology, clothing and services have terrific long-term growth prospects, as communities become more active in the fight against obesity.

Technology researcher IDC this week predicted wearables – smart watches, smart clothing, “hearables” (smart headphones) and other gadgets – will become a “hyper segment”. IDC forecasts global wearables sales will double by 2021, underpinned by growth in smart watches, and expects compound annual growth of 18.3% over five years – a growth rate most industries would kill for in this economy.

Parents with sporty children know how much money is involved: weekend trips to Super Retail Group’s (SUL) Rebel and AMart sports chains to buy and upgrade sporting equipment; kids wearing high-tech sport shirts, leggings and shoes; fitness trackers bought as birthday presents, and so on.

Witness the success of RCG Corporation (RCG), owner of The Athlete’s Footchain and key beneficiary of rising demand for sporting and walking shoes, or the privately held Lorna Jane Australia in the booming active wear clothing segment.

Notice how many retailers are adding active wear – gear that used to be worn only in gyms – to their range (or how many mums get around in gym gear). Uniqlo, for example, has gone into active wear in a big way through tennis sponsorships. The segment is a rare bright spot in a depressed retail sector.

Consumers are paying up for high-tech active wear. The privately owned 2XU, a provider of compression sportswear, has a loyal following who love its upmarket leggings and activewear. As with Lorna Jane, 2XU was a mooted Initial Public Offering (IPO) but it never happened.

Like Catapult, 2XU has benefited from the “consumerisation” of high-tech sporting equipment. Its high-tech compression wear – once used mostly by elite athletes, sporting clubs and other early adopters – has found its way into mainstream retail.

The concept of “prosumers” (keen amateurs) has great potential. From middle-aged men in lycra (MAMILs) spending thousands on the latest push bike, to avid runners spending hundreds on the latest sports watch … these amateurs want the same equipment, or a variation of it, that the pros use, to lift their performance.

Catapult is ideally placed to exploit this trend, given its credibility in elite sports. More than 1,000 sporting clubs worldwide, including those in the NFL, English Premier League, National Rugby League and Australian Football League, use its products.

Several of the world’s iconic sporting clubs rely on Catapult technology, making it one of Australia’s emerging software success stories.

Growth in the “prosumer” sporting market is the key to Catapult’s long-term fortunes and a reason why it looks undervalued at the current price. The untapped market is schools using the same sporting equipment elite athletes and prosumers favour.

Catapult ready for its second wind

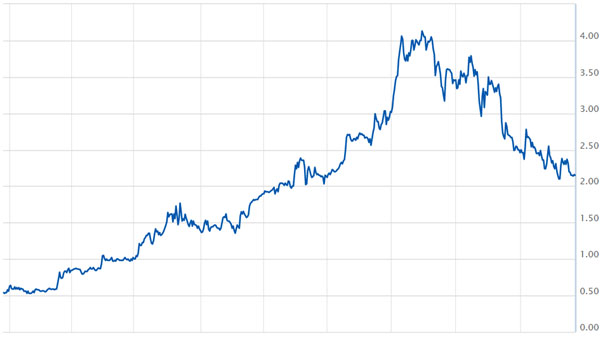

To recap, Catapult raised $12 million through a December 2014 Initial Public offering (IPO) to develop new technology that combines wearables hardware with analytical software. Its 55-cent issued shares peaked at $4.05 in August 2015, before tumbling to $2.09.

Chart 1: Catapult Group International

[1]

[1]Source: ASX

Like other high-growth small caps, Catapult was punished during sector rotation in the fourth quarter of 2016. Fund managers sold overheated small-cap stocks and bought blue-chip growth sectors as they bet on global reflation after Donald Trump won the US Presidency.

Moreover, the market underestimated Catapult’s 2016 acquisitions of XOS Technologies and Kodaplay Limited, which trades as Playertek. A $100 million institutional and retail placement last year preceded the acquisition; some fund managers would have preferred Catapult to reinvest less in the business and move faster towards profitability.

Both acquisitions are smart long-term moves. XOS Technologies, a market leader in innovative digital and video analytic software for elite sports teams in the US, is a natural fit with Catapult. The expanded group can offer wearables technology and video software to the same group of elite sporting teams, boosting revenue and customer retention. Selling two products rather than one to the same customer group makes sense.

Ireland-based Playertek, a leading developer of wearable analytics software in the prosumer market, gives Catapult a platform to enter this global market. Playertek enables amateur athletes to use low-cost wearables software to measure their performance.

Its technology, for example, measures players’ performance during the game using a range of metrics, analyses their game impact and even compares their performance with pro athletes. That aids performance improvements over a season and guides training loads.

These acquisitions will drive the next phase of Catapult’s growth. The company was profitable on an underlying EBITDA basis and cash flow positive for the first time in its FY2017 interim result – an important inflexion point in its journey so far. The company’s elite wearables subscription base and revenues are growing strongly.

Catapult’s strategy has three pillars: own the performance-technology segment for elite sport; commercialise elite wearables and video data; and leverage its elite brand into the prosumer market. Elite sporting-team customers provide a high degree of visible, recurring revenue, but it is the prosumer market that has the big upside.

Catapult estimates the prosumer market is around 10-20 times larger than the elite sporting-club market. A range of new prosumer products is due for launch in FY18, as Catapult takes elite sporting technology to semi-professionals and keen amateurs.

Catapult’s distribution strategy and pricing are critical in the prosumer market. Expect it to focus on selling wearables technology to schools and junior sporting clubs, using a low-cost monthly-subscription-model, per player, e.g. a top private school paying $20 per month, per player, to use Catapult’s performance technology for its First XV or or First XVIII.

The US schools and universities market is fertile ground for elite sporting technology, given the obsession with gridiron, baseball, basketball and other sports. A rising duty of care to prevent sporting injuries in young athletes adds to the case to use Catapult technology, which helps manage injuries by providing athlete performance data.

Catapult signed two US schools last year for its technology – a small step, but validation nonetheless of its appeal in this market. One can see the potential of Catapult signing up more schools and charging on a per-player/per-month basis. That’s creates recurring revenue and schools are likely to stick with the one technology provider.

The main threat is competitors offering cheaper products. Price-sensitive schools might favour low-cost options, but my view is that star young athletes and older keen amateurs will want the same technology that professionals use.

Also, Catapult dominates a fragmented market in elite wearables technology. Its global market share is larger than all its main competitors combined, meaning reduced risk of an industry behemoth undercutting Catapult with lower prices.

I like Catapult’s integration strategy: expand horizontally by introducing new technology, such as video analysis; and push into new verticals, such as prosumers. And base everything on a subscription pricing model that mushrooms as more customers sign up, and provides high profits margins and good earnings visibility.

As a loss-making small cap (on an NPAT basis), Catapult clearly suits experienced investors who are comfortable with higher risks. They need a long-term view with this stock.

Catapult ran too far, too fast when it breached $4 and hype abounded about its prospects. The stock has almost halved, despite its long-term prospects improving with some clever acquisitions and further confirmation of growth in wearables technology.

Tony Featherstone is a former managing editor of BRW and Shares magazines. All prices and analysis at March 21, 2017.

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.