[table “263” not found /]

Great US job news resulted in Wall Street gains turning to small losses with a couple of hours before the closing bell. However the likely cause of any negativity was profit-taking, ahead of the Fed meeting on interest rates next week. If Janet Yellen doesn’t raise rates next week, some will argue she never will!

Let’s look at the employment story for the Yanks across February, with the headline being that 235,000 jobs showed up and the unemployment rate fell to 4.7%. Donald Trump is starting to look like Homer Simpson’s beloved doughnut. In case you haven’t been a Simpsons’ fan, this was his view on the little treat: “Donuts – is there anything they can’t do?”

Not surprisingly, the President was soon pointing to the scoreboard, showing how the economic points scored since his election has been down to him. Of course that is an exaggeration. We were expecting an improving US economy and at least three rate rises over 2017 but he definitely has made that more certain. The Trump effect has been like a turbo-charging to not only the US economy. It has helped the overall global economic outlook, with his talk about lower taxes and regulation as well as infrastructure spending resonating with governments and political debates around the world.

If you need convincing about these job stats making a rate rise a shoe in, then take in these observations from Scott Clemons, chief investment strategist at Brown Brothers Harriman. “I don’t see any bad numbers in this report. The Fed didn’t need permission from the labor market to raise rates next week, but it got it anyway.” (CNBC)

A rate rise in the US and lower commodity prices could make stock price action notable this week, with outfits such as Capital Economics predicting iron ore at US$45 a tonne by year’s end. If that’s right, then that would be nearly a 50% drop from recent levels! But don’t panic because Morgan’s chief economist, Michael Knox, who’s good with commodity calls, is a lot more optimistic.

Looking back at the week, the S&P/ASX 200 index was up 0.6% for the week to finish at 5775.6 with banks, healthcare, consumer staples and tech companies finding friends on the market. I love this market optimism but it still seems unusual that there hasn’t been a sell off even to a small degree.

Clearly, there have been some small index drops but they’ve been so shallow that I couldn’t use my old “buy the dips” strategy! With rate rises and softer commodity prices, next week should be an interesting test but then again you have the optimism that the US economy is proving to be as good as it promised.

And even though President Trump provides great fodder for the media with his daily tweets, he hasn’t spooked the stock market with his policies. In fact, his attack on government regulations has shocked a lot of people and each change to rules governing society and the economy creates a stock price opportunity. For example, did you know that in Trumpland, hunters can use lead bullets again in areas where once they were banned for environmental reasons? (Did I not compare Donald to doughnuts?)

Commodity prices are going to be an important issue for our stock market as we approach the old “sell in May and go away” time of the year, with speculation over China’s economic growth, which now looks better than expected, the country’s possible assault on credit growth and excess supply of iron ore and oil likely to create some challenges for stocks in the resource space.

That said, a lot of analysts are backing South 32 to have a good year and, earlier this week, James Dunn in this very Report explained why.

On the local economy, I have to share this from CommSec’s Craig James on the RBA’s take on our economy: “Australia is in the midst of the world’s longest economic expansion and the Reserve Bank doesn’t see that ending any time soon. The Reserve Bank has issued a very stodgy, balanced commentary on the economy. Some might say boring. But boring is good in the current environment. Because the Reserve Bank certainly isn’t suggesting that more stimulus needs to be applied to the economy, nor do interest rates need to go up. Inflation is low and rising only gradually; economic growth is expected to pick up over the year; some global economies may experience above-trend growth; and domestic housing and labour markets are mixed.”

The bottom line is optimists on the Oz economy have the RBA on their side.

Next week could deliver some interesting economic revelations here and abroad, with business and consumer confidence readings and our latest jobless reading bound to be closely scrutinized. However, the Fed meeting and the expected rate rise and how the market responds could show what a different world we live in post ‘Donald the donut’ (US spelling!). A couple of years ago, the very mentioning of a rate rise led to market sell offs, so that’s measurable progress!

What I liked

- The RBA’s no change to its decision on rates and all the language that confirms my view that the Bank thinks the economy is going well and doesn’t need any rate cuts.

- The Performance of Construction index rose by 5.4 points to 53.1 in February. Anything over 50 means the sector is expanding.

- The number of loans (commitments) for budding home owners (owner-occupiers) rose by 0.5% in January, the third consecutive rise. But the increase was wholly due to a 5% lift in refinancing. The number of loans by non-bank lenders rose by 4.7% in January after a 6.2% lift in December – the strongest back-to-back gain in 32 months. This is a good omen for confidence in the economy.

- Dividends totaling $17.4 billion will be paid out by listed companies to their shareholders in the three weeks beginning March 27, which should be a bonus for the economy.

- In 2016, 37.6 million passengers were carried on international carriers in Australia, up 7.9% on a year ago and nearly the fastest rate in 5½ years.

- US factory orders rose by 1.2% in January (forecast +1.0%). Durable goods orders were up 2% (ex-defence +1.6%). So the good economic news rolls on under President DT!

- Europe’s central bank policymakers discussed whether interest rates can rise before their asset-buying program ends. Who would’ve thought that possible? The Eurozone economy is looking better than expected. Let’s hope the Dutch election next week and the ones that follow in France and Germany over the rest of the year don’t spoil this improving economic picture.

- Chinese exports fell by 1.3% in the year to February (forecast +12.3%), with imports up 38.1% (forecast +20%). The export numbers weren’t great but big imports is good news for Chinese economic growth.

What I didn’t like

- Oil prices have dropped for most of the week and I don’t want to see another sustained slide. I’d like a stable oil price but US oil producers could be the fly in the ointment for supply. Some small-cap exploration and production companies saw their stock slump more than 30% this week! US drillers added eight oil rigs in the latest week, bringing the total count up to 617, or 60% more than a year ago.

- Iron ore’s rally is showing signs of cracking. The commodity posted the biggest weekly slump in almost four months. In Qingdao (China), ore with 62% content (which hit $US94.86 a tonne on February 21 – the highest since August 2014) lost 5% this week to $US86.72. (Metal Bulletin)

- The Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES) forecasts for the rural sector were released on Tuesday. Real net farm cash income is tipped to fall 11% in 2017/18 after a similar-sized gain in 2016/17.

Love a contrarian

Thought I’d give optimists on BHP and Rio a positive pearl for the weekend. In case you missed it, this week UBS upgraded its call on the iron ore price for 2017 from US$56 a ton to US$71, based on strong demand and good steel margins. Go UBS!

The Switzer Investor Strategy Day

Tickets are now on sale for the Switzer Investor Strategy Day. This year, we are holding events in Sydney (April 4), Melbourne (April 11) and Brisbane (April 12) and as a subscriber you are entitled to $100 off the price of your ticket. Click here to learn more [1]. To claim your discount, remember to enter the promotion code SSROFFER before you check out.

The week in review:

- I discussed why business killers like Amazon [2] make me wary about going long retail beyond a short-term play!

- Paul Rickard recapped the performance of the model income and growth portfolios [3] in February. And they are both back in the black.

- James Dunn [4] revealed five good value stocks.

- The brokers upgraded [5] South32 this week, but Bank of Queensland was in the not-so-good books.

- The Super Stock Selectors liked Bapcor and Fortescue Metals Group [6], but were not as keen on APN Outdoor and Flight Centre.

- Could QBE join the likes of Qantas, Bluescope and Perpetual in the hall of impressive turnaround stories [7]? Tony Featherstone posed the question in this week’s Switzer Super Report.

- Charlie Aitken revealed a small cap growth stock with a big fully-franked yield [8].

- In this week’s Professional’s Pick, ST Wong explained why he likes Caltex [9].

- And in our second broker report, the brokers upgraded Boral while Westfield was downgraded [10].

Top stocks – how they fared

What moved the market?

- The drop in iron ore and oil prices, which hurt resource and energy stocks. BHP and South32 also traded ex-dividend.

- Trump’s love affair with Twitter. This week, he tweeted about his desire for more competitive drug prices.

Calls of the week

- The RBA kept the cash rate on hold at 1.5%.

- Tony Featherstone said QBE is starting to get its mojo back! Find out why [7].

- Paul Rickard said Victoria’s new solution to housing affordability is bad news for investors. Read more on Switzer Daily [11].

- And Pauline Hanson made the call to apologise for her controversial comments on vaccination tests.

The week ahead

Australia

- Monday March 13 – Credit & debit card lending (January)

- Tuesday March 14 – Overseas arrivals & departures (January)

- Tuesday March 14 – NAB Business survey (February)

- Tuesday March 14 – Speech by Reserve Bank official

- Wednesday March 15 – Monthly consumer confidence

- Wednesday March 15 – New vehicle sales (February)

- Wednesday March 15 – Lending finance (January)

- Thursday March 16 – Employment/unemployment (February)

Overseas

- Tuesday March 14 – US Producer prices (January)

- Tuesday March 14 – US NFIB Business Optimism (February)

- Tuesday March 14 – China monthly data (January/February)

- Wednesday March 15 – US Federal Reserve rates decision

- Wednesday March 15 – US Retail sales (February)

- Wednesday March 15 – US Consumer prices (February)

- Wednesday March 15 – Netherlands general election

- Thursday March 16 – US Housing starts (February)

- Thursday March 16 – US Philadelphia Fed index (March)

- Friday March 17 – US Industrial production (February)

- Friday March 17 – US Leading index (February)

- Friday March 17 – US Consumer sentiment (March)

Food for thought

Perfection is not attainable, but if we chase perfection we can catch excellence

– Vince Lombardi

Last week’s TV roundup

- To discuss the RBA’s rate decision this week, the upcoming jobs numbers, what the elections in Europe could mean for the global economic outlook and more, AMP Capital’s Shane Oliver joins Super TV [12].

- What factors are impacting the market other than Trump? To answer this and more, Marcel von Pfyffer from Arminius Capital joins the show [13].

- The expected stock market sell-off is yet to materialise, so to discuss where the market might be headed, Contango Asset Management’s George Boubouras joins the show [14].

- Which sectors did well in February, and what does it mean for the stock market in the year ahead? Paul Rickard joins Super TV [15].

Stocks shorted

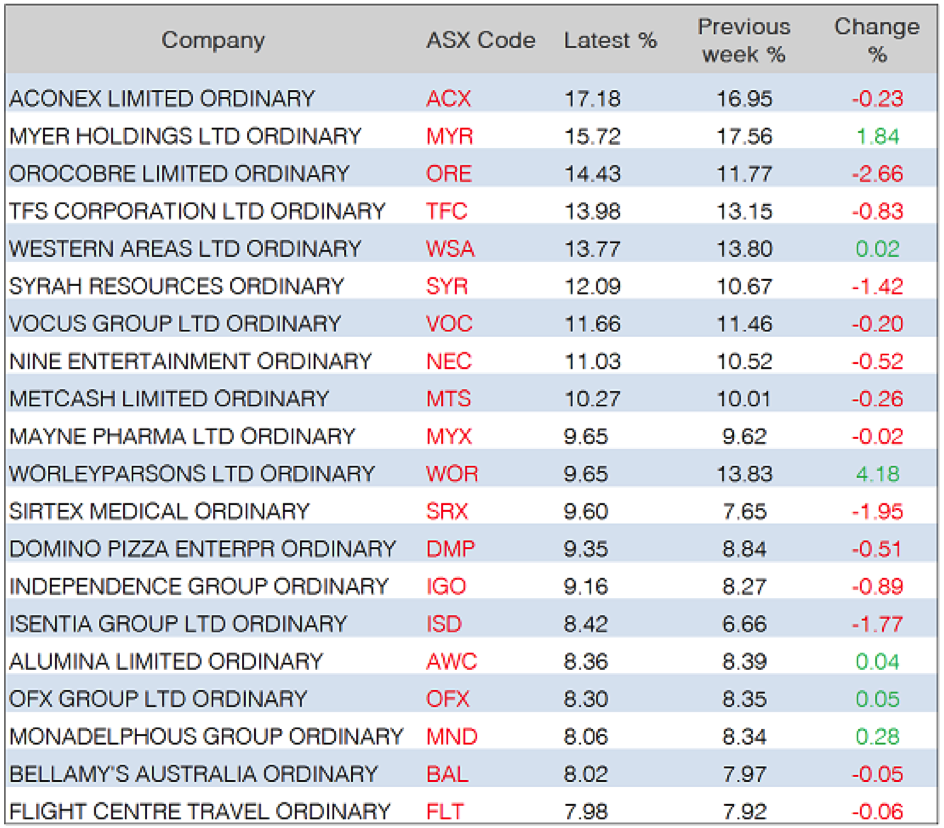

ASIC releases data daily on the major short positions in the market. These are the stocks with the highest proportion of their ordinary shares that have been sold short, which could suggest investors are expecting the price to come down. The table shows how this has changed compared to the week before.

This week the biggest mover was Orocobre with a 2.66 percentage point increase in the amount of its shares sold short to 14.43%. WorleyParsons went the other way, with its short position decreasing by 4.18 percentage points to 9.65%.

[16]

[16]Source: ASIC

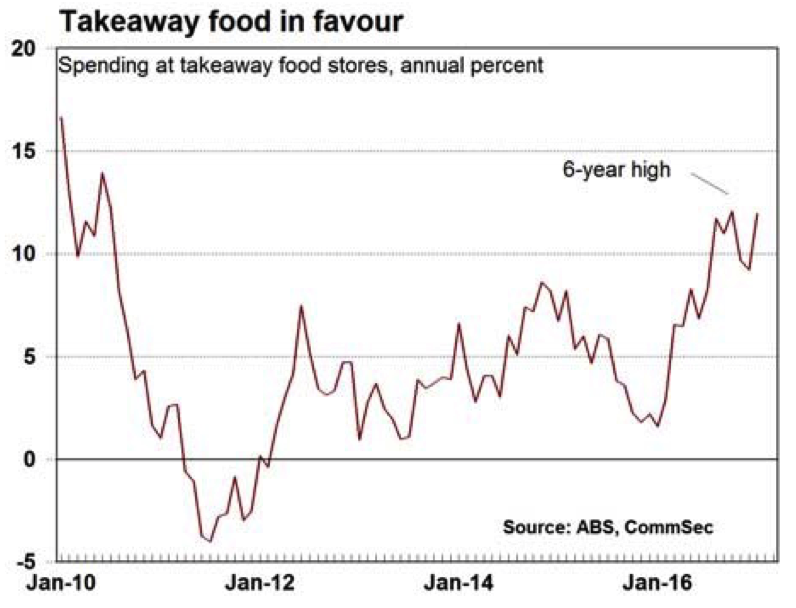

Chart of the week

[17]

[17]Source: CommSec, ABS

Check out this chart, which shows spending at takeaway food stores went up 11.9% on a year ago! CommSec says the increased range of healthier takeaway options is contributing to the trend.

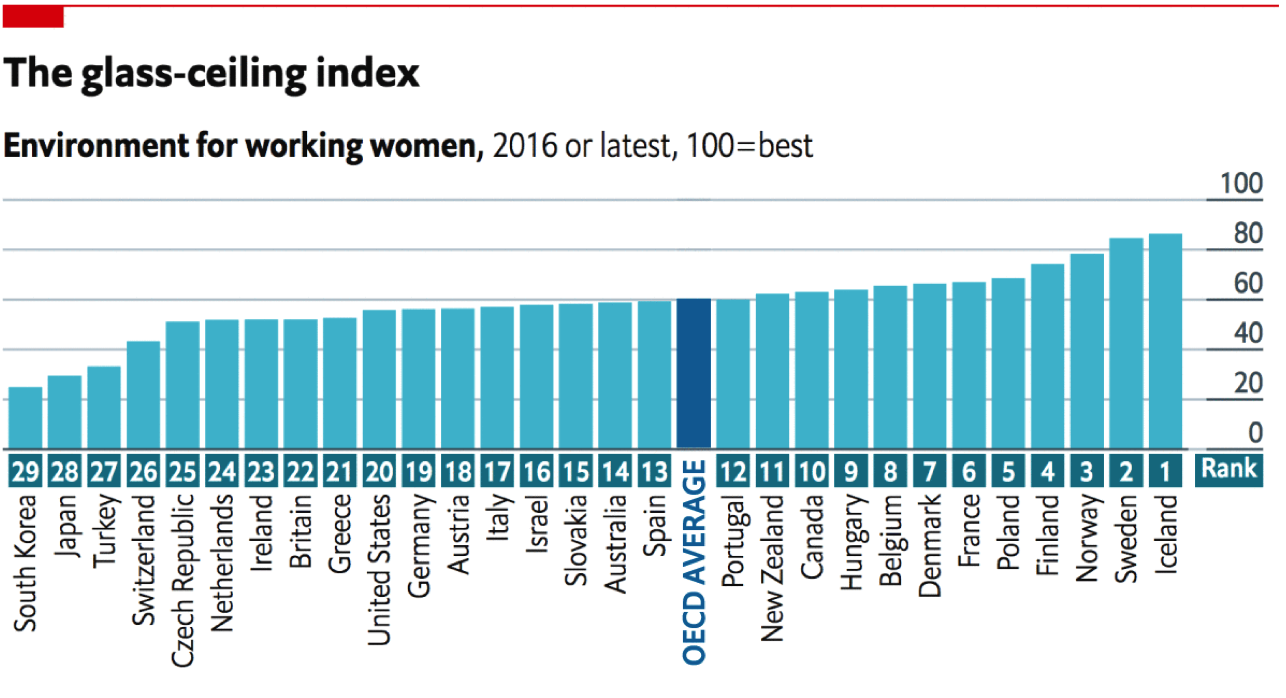

[18]

[18]Source: The Economist

To coincide with International Women’s Day, The Economist published this ‘glass-ceiling index’ which “combines data on higher education, workforce participation, pay, child-care costs, maternity and paternity rights …” – and more – into a single measure for gender equality in the labour market. Scores reflect a weighted average of the country’s performance on ten indicators. Nordic countries lead the way.

Top five most clicked stories

- Charlie Aitken: A small cap growth stock with a big fully franked yield [8]

- James Dunn: 5 good value stocks [4]

- Peter Switzer: Which retailers will be killed by Amazon? [2]

- Rudi Filapek-Vandyck: Buy, Sell, Hold – what the brokers say [5]

- Paul Rickard: Portfolios track market higher in February [3]

Recent Switzer Super Reports

- Thursday 9 March 2017: Turnaround story? [19]

- Monday 6 March 2017: Storm brewing [20]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.