The most important news last week was the Commonwealth Bank’s move to increase its interim dividend by 1c to 199c per share. While the increase in itself was immaterial, it signaled that the Bank believes that it has enough capital and won’t need to undertake a further dilutive capital raising.

Of course, the Bank said it was all about maintaining a dividend payout ratio at 70%, but in an environment where most analysts have been forecasting reducing dividends, any action to increase the dividend, however small, was a big statement.

And it came less than a week after APRA Chairman, Wayne Byres, said in a prepared speech that “the main policy item on our agenda in 2017…is to set capital standards so that the capital ratios of our deposit-takers are ‘unquestionably strong’…We will have more to say in the coming months about how we propose to give effect to the concept of unquestionably strong”. He went on to say that “The major banks have added in the order of 150 basis points to their CET1 ratios over the past couple of years. Assuming the industry continues to steadily build its capital, we expect it will be well placed to respond to future policy changes in an orderly manner.”

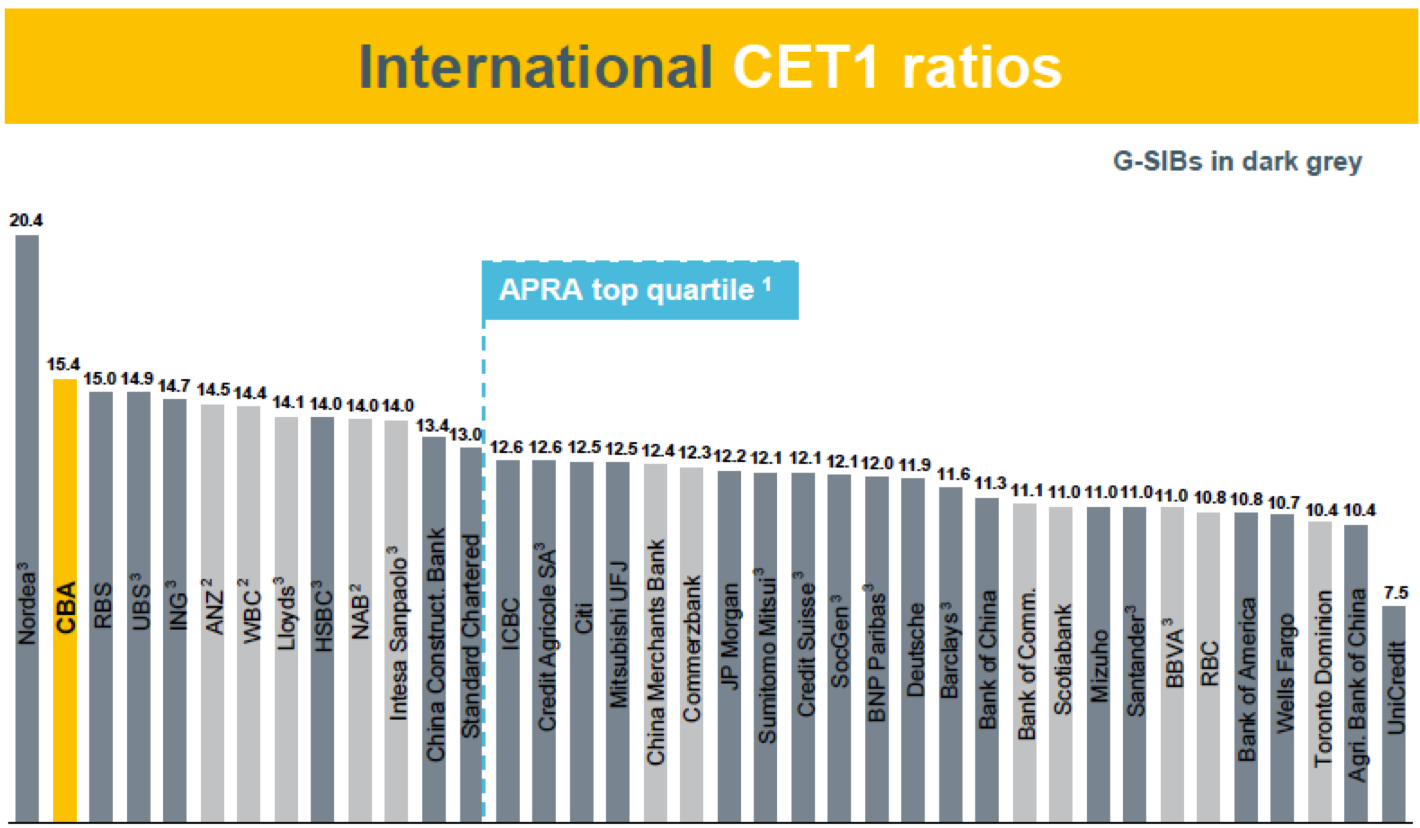

Commonwealth Bank produced the following chart to show that on an internationally comparable basis, it has the second highest CET1 (Common Equity Tier 1) ratio of any major global bank at 15.4%. This places it in the top quartile of the top quartile.

[1]

[1]Source: CBA Investor Briefing

There is little doubt that the banks will work to further improve their capital ratios, but they won’t be undertaking dilutive issues and dividend cuts are now largely off the agenda. This is what the market celebrated, with CBA and the other major banks rising strongly. Since CBA’s announcement on Wednesday, it has put on $2.76 or 3.34%, closing Friday at $85.39.

A strong half year

CBA’s cash profit of $4.91bn was up 2% on the corresponding half of 2016. Most importantly, it was able to demonstrate revenue growth of 3%, while operating expenses grew by only 1%. This gave it “positive jaws” (income growing faster than expenses), with operating performance up by 4%.

Revenue growth was achieved in an environment where margins continued to come under pressure, with group NIM (net interest margin) down by 4bp to 211bp, or down by 3bp, when compared to the half year ending 30 June 16. Although pressure on NIM is moderating, CBA said that it expects it to keep trending down.

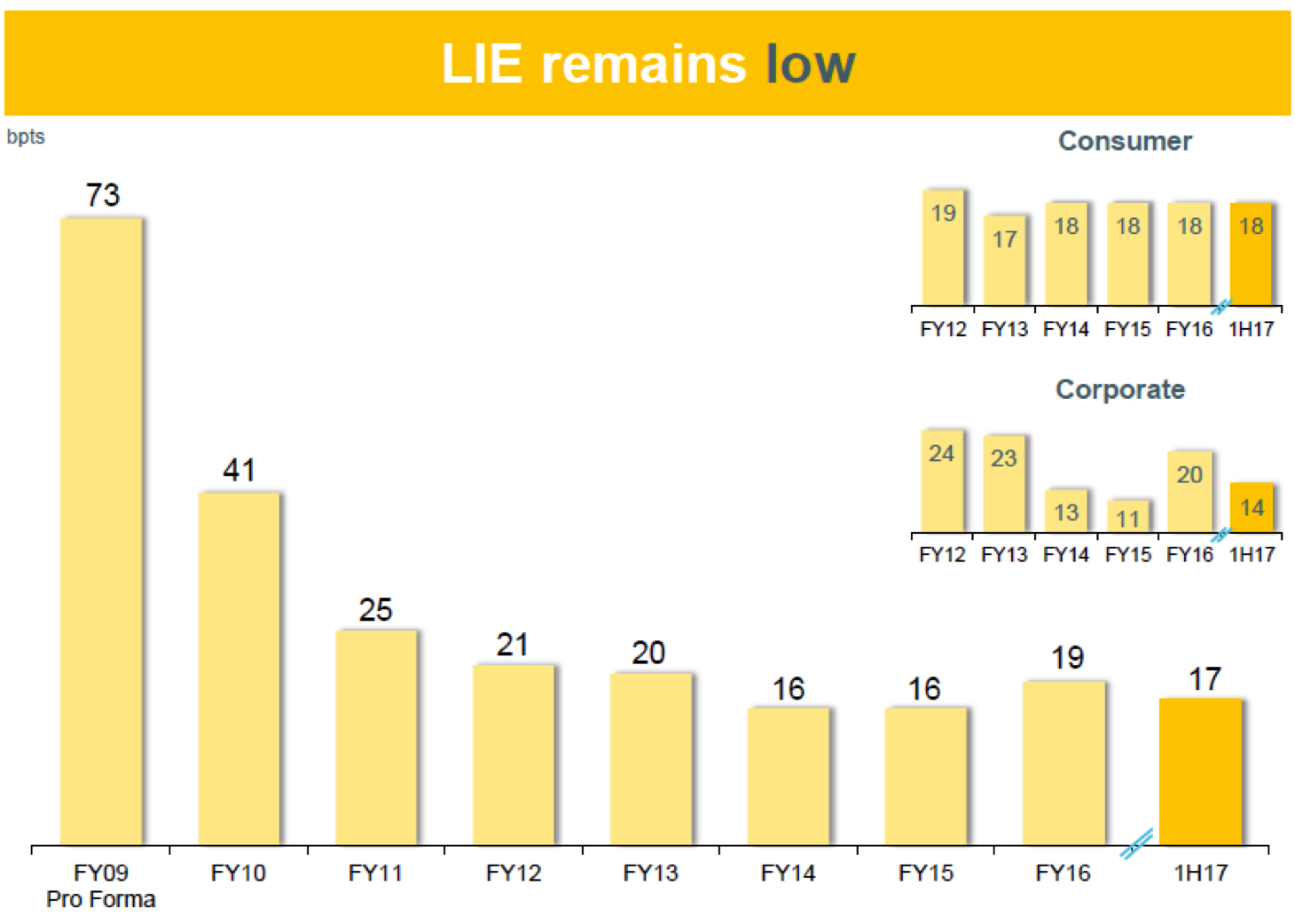

Loan impairment expense remains low at 0.17% of group assets (17 basis points). The forward indicators on consumer arrears are at historically low levels, despite some elevation in WA.

[2]

[2]Highlights of the result included:

- Market leading return on equity (ROE) of 16.0%, up from the June half of 15.6%;

- Capital ratio (CET1) of 9.9%;

- A group cost to income ratio of 41.5%, with the retail bank at a staggering 30.8%;

- Market share gains in home loans and in NZ;

- Very strong profit performance by the retail bank, contributing 50% of group profit; and

- An improved performance from the institutional bank, mainly due to trading income and continued restraint in corporate lending.

The wealth management division saw cash profit fall by 34% to $249m. While this was an improvement on the June half, the cost of advice remediation, margin pressure in funds management and insurance claims in wealth protection weighed on this division.

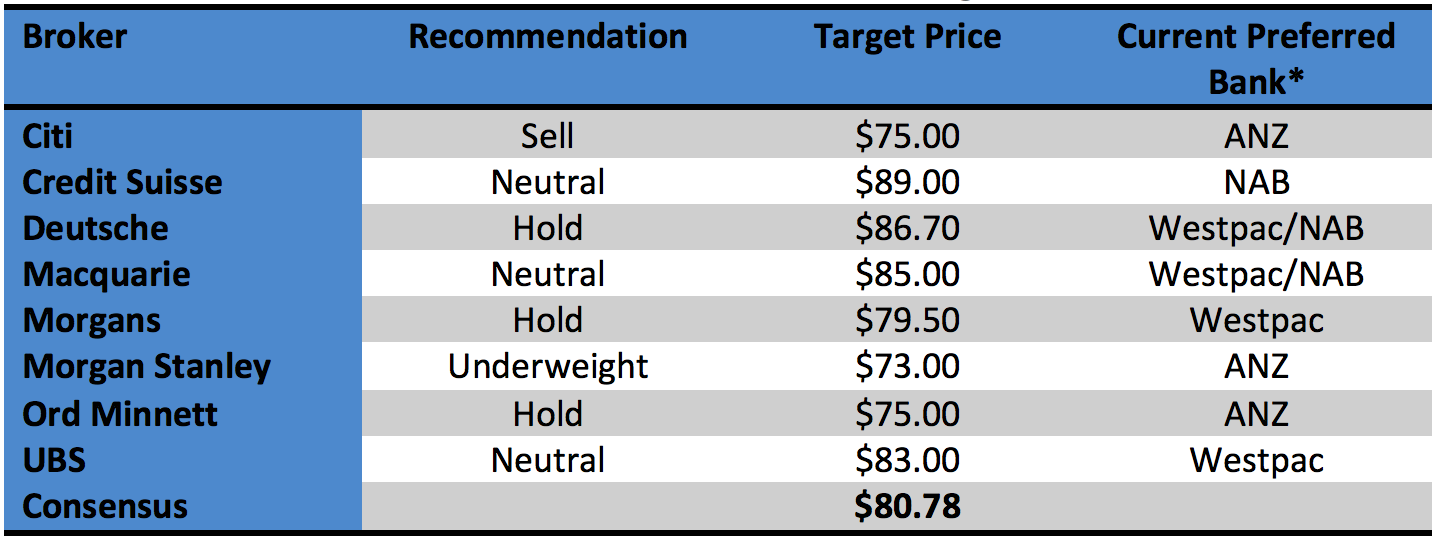

What the brokers say

The Bank’s result beat broker consensus and was seen as reasonably strong, with few faults. Most of the brokers raised their price target, but there were no upgrades.

Overall, the broker’s acknowledge that while CBA is the premium bank with the best technology and leading market shares, it also trades at a premium price, and the differences are not that material. Accordingly, they see CBA as being marginally over-valued and ascribe a neutral rating on the stock.

Individual broker recommendations are shown in the following table.

[3]

[3]* Source FN Arena. Based on highest recommendation

According to FN Arena, CBA is trading on a multiple of 15.4 times FY17 earnings and 15.0 times FY18 earnings. The forecast dividend yield is 5.0%.

What I say

I draw two main conclusions. Firstly and most importantly, I think that the banks are getting close to “unquestionably strong” and fears about capital raisings/dividend cuts are likely to recede. While there will be ongoing pressure on NIM and revenue growth will remain challenging, there are no signs to suggest that the credit cycle is deteriorating and banks still have enormous opportunities through productivity initiatives and branch closures to attack their cost bases.

If the stock market is to power through 6000, it will be driven by the leading stocks – so it will need the major miners and the major banks to fire. I am not sure that I want to be overweight the major banks, but I can’t see any real reasons to be underweight. When I add in the security of the dividend yield and the prospect of higher interest rates later this year (which in the short term will boost margin), I am more inclined to be positive on the sector.

Secondly, CBA should be a core stock in your portfolio. Although it is the most expensive bank (based on forward earnings multiples, it is trading at a premium of 15% to the ANZ and NAB and approximately 7% to Westpac), this is not out of the ordinary compared to the last five years.

[4]

[4]* Source FN Arena, using closing price on 17 February 2017

Over this period, the premium has ranged from around 8% to as high as 35%. While there is no doubt that the competitive differences between the banks have narrowed and that they are largely pursuing the same strategy, CBA still comfortably leads in technology, product market shares and balance sheet strength and has been able to translate this into the leading ROE.

I am not making the case that CBA is necessarily the best bank to own. But with an index weight of 9.5%, it is too big to ignore, and if you own two or three major banks, then CBA has to be in the mix.

For dividend chasers, CBA goes ex-dividend on Wednesday (so you can purchase CBA up to the close of business on Tuesday and still get the dividend).

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.