In the good books

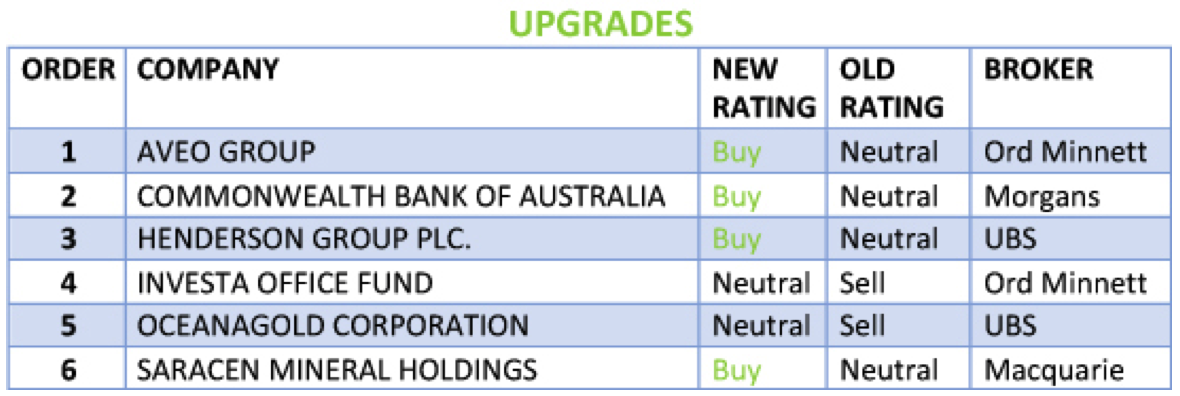

AVEO GROUP (AOG) Upgrade to Accumulate from Hold by Ord Minnett B/H/S: 4/0/0

Ord Minnett is more positive about the company’s prospects after an investor briefing. Earnings forecasts are lifted because of higher assumed development completions. The broker now has greater confidence in delivery and increased margins.

Ord Minnett assumes 10.7% growth in earnings per share in FY17 and 8.4% for FY18. Rating is raised to Accumulate from Hold. Target rises to $3.70 from $3.40.

[1]

[1]OCEANAGOLD CORPORATION (OGC) Upgrade to Neutral from Sell by UBS B/H/S: 4/2/0

UBS believes the appointment of a new mining minister in the Philippines has materially reduced the risk of the suspension order on Didipio from being enforced.

This should allow the market to re-focus on growth opportunities at Haile and at NZ operations.

The broker upgrades to Neutral from Sell. Target is raised to $4.35 from $3.41.

SARACEN MINERAL HOLDINGS LIMITED (SAR) Upgrade to Outperform from Neutral by Macquarie B/H/S: 2/0/0

Macquarie reviews production forecasts in the light of recent exploration successes. The broker now expects production to exceed 300,000 ounces per annum over the next five years.

The broker believes mid-grade, high-tonnage, shallow underground mines can be highly profitable to run. The success at Karari underpins this mode of operation for the company.

Rating is upgraded to Outperform from Neutral. Target is raised to $1.30 from $1.00.

In the not-so-good books

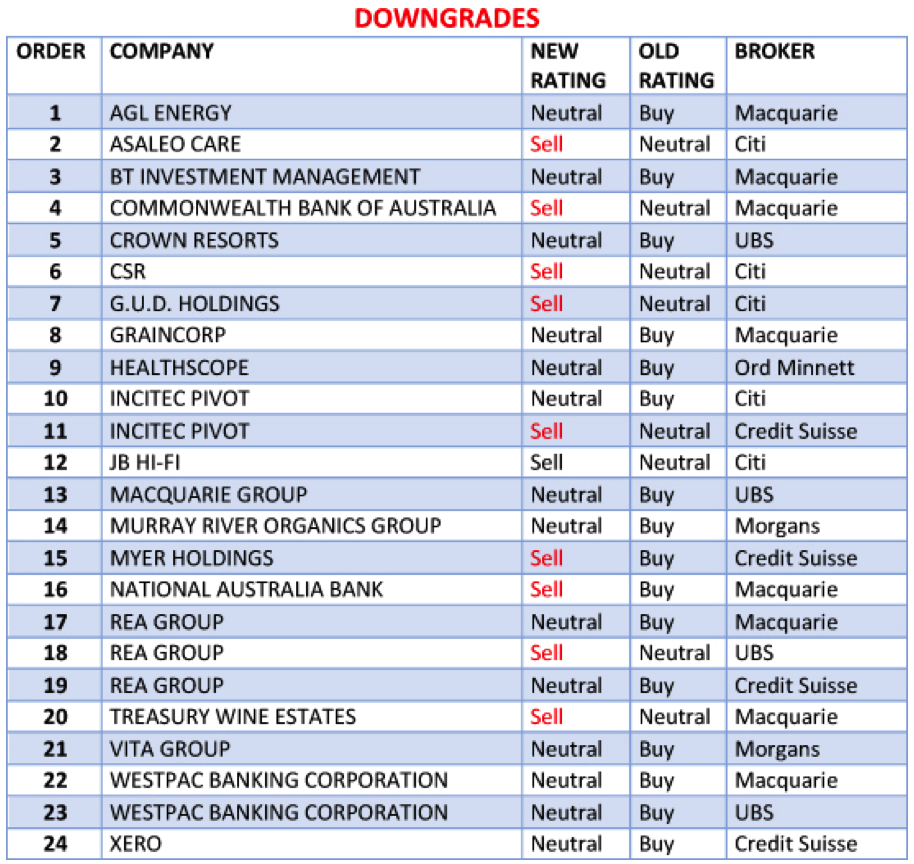

BT INVESTMENT MANAGEMENT LIMITED (BTT) Downgrade to Neutral from Outperform by Macquarie B/H/S: 1/5/0

First half results beat Macquarie’s forecasts but were in line with expectations after adjusting for one-off items. The company’s key operating metrics are meeting the broker’s fund manager investment criteria.

Rating is downgraded to Neutral from Outperform following recent share price performance. The stock is trading at more than 20x FY17 and FY18 earnings forecasts and is the highest-rated fund manager under the broker’s coverage.

The downgrade comes despite the broker’s acknowledgement of the company’s capacity and demonstrated ability to deliver net inflows. Target is reduced to $11.70 from $11.92.

[2]

[2]GRAINCORP LIMITED (GNC) Downgrade to Neutral from Outperform by Macquarie B/H/S: 0/5/0

First half results beat Macquarie’s expectations with a strong performance from the upstream businesses.

The company has flagged higher gas and electricity costs in FY18 and beyond, relevant for its oil processing & malt businesses. Macquarie factors in a -$7-9m impact to EBIT in FY18 and beyond.

The broker downgrades to Neutral from Outperform and reduces the target to $10.00 from $10.50.

HEALTHSCOPE LIMITED (HSO) Downgrade to Hold from Accumulate by Ord Minnett B/H/S: 2/5/0

Ord Minnett raises concerns about the NSW decision to reduce the number of public beds along with a requirement that Healthscope meet private conversion targets from patients entering the new Northern Beaches Hospital.

This may prove challenging, in the broker’s opinion, especially in light of the downgrading of private health cover and increased consumer sensitivity to out-of-pocket health costs. The broker reduces FY17 forecast by -1.5% to reflect the likely impact of the Easter/Anzac Day holidays on volumes.

Target is reduced to $2.45 from $2.70. The broker believes investment risk has risen and reduces its rating to Hold from Accumulate.

VITA GROUP LIMITED (VTG) Downgrade to Hold from Add by Morgans B/H/S: 0/1/0

Vita has suspended its plan to expand its store count until negotiations with Telstra (TLS) on remuneration are finalised, at a time as yet unknown. The company has issued revised FY17 guidance -6% below Morgan’s prior forecast, representing a -16% fall in the second half from the first.

As the terms of Vita’s future agreement with Telstra are uncertain, FY18 earnings uncertainty is very high, Morgans notes. Downgrade to Hold for now. Target falls to $1.67 from $3.49.

XERO LIMITED (XRO) Downgrade to Neutral from Outperform by Credit Suisse B/H/S: 2/4/0

Credit Suisse observes Australasia remains strong, with no sign subscriber additions have peaked. Meanwhile, UK growth has stepped up and gross margins rebounded.

The broker suspects further margin expansion is likely thanks to the AWS platform, while the challenge to build scale in North America remains the key uncertainty.

With the stock having gained 33% in six months, Credit Suisse downgrades to Neutral from Outperform. Target rises to NZ$23.50 from NZ$21.00.

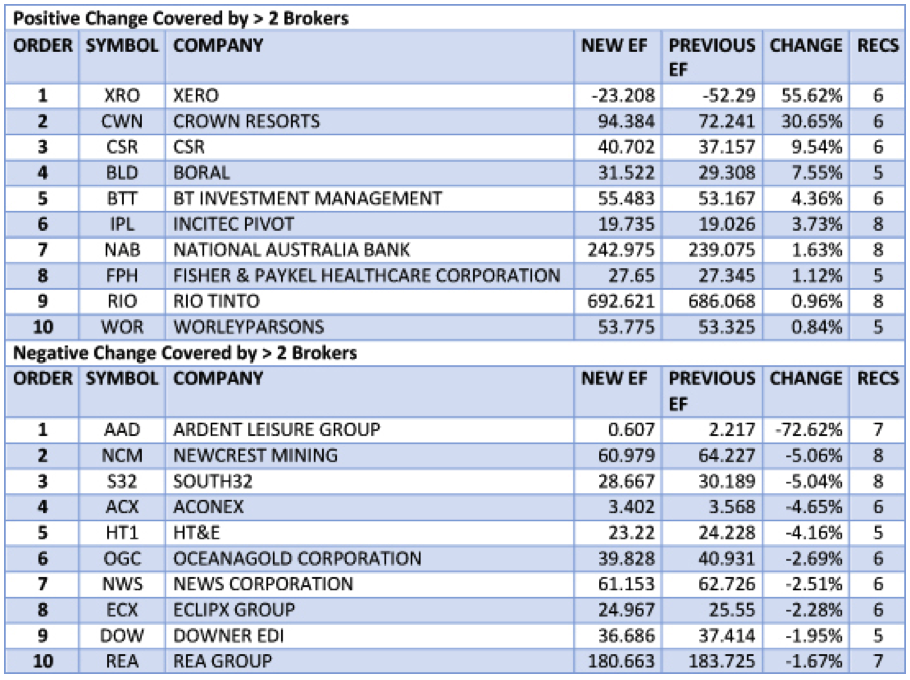

Earnings forecast

[3]

[3]Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.