In the good books

BANK OF QUEENSLAND LIMITED (BOQ) Upgrade to Hold from Lighten by Ord Minnett B/H/S: 1/6/1

First half earnings underwhelmed Ord Minnett but are believed to be a low point in the earnings trajectory, with improved prospects for margins, volumes and costs.

The broker expects the bank to look for further cost savings with FY17 result and now believes the risk/reward balance is more appropriate.

Ord Minnett raises its recommendation to Hold from Lighten. Target is $11.00.

[1]

[1]

WESTERN AREAS NL (WSA) Upgrade to Neutral from Sell by UBS B/H/S: 1/5/1

UBS updates its valuation to include the Odysseus pre-feasibility study. The broker notes potential for mine life to be extended towards 10 or more years.

The broker believes the market has previously provided no value for this project and, given how short the market is on the stock, there is growing risk to the upside.

UBS upgrades to Neutral from Sell, believing the risk/reward is more balanced. Target is raised to $2.58 from $2.38.

In the not-so-good books

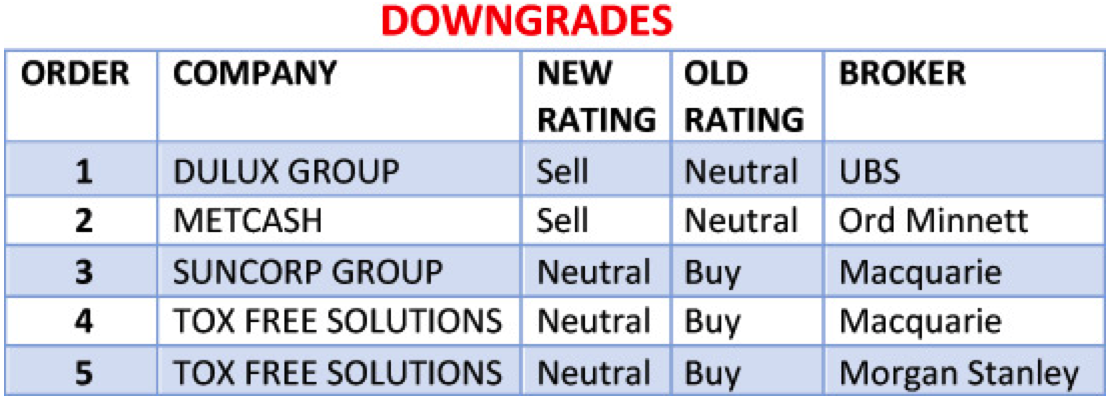

DULUX GROUP LIMITED (DLX) Downgrade to Sell from Neutral by UBS B/H/S: 0/4/4

There’s no doubting Dulux’ superiority and solid market share in paint, and as such the stock deserves a premium multiple, UBS suggests. But the non-paint business continues to show subdued prospects and a turnaround seems some way off.

A cooling in the housing market also suggests paint earnings may have seen a peak. On 7% outperformance against the index in the past month, UBS downgrades to Sell, retaining a $6.10 target.

Earnings per share forecasts are modestly raised and the target lifted to $2.10 from $2.00. Nevertheless, the broker believes the risk-reward equation is not attractive, post the recent share price performance.

[2]

[2]

SUNCORP GROUP LIMITED (SUN) Downgrade to Neutral from Outperform by Macquarie B/H/S: 4/3/1

Macquarie assesses that premium rate increases across the insurance market are being led by claims cost inflation. As insurers get costs under control price rises should again moderate across of market, in the broker’s view.

The broker downgrades expectations for Suncorp’s gross written premium growth based on its analysis. Rating is downgraded to Neutral from Outperform. Target is reduced to $13.60 from $14.33.

Earnings forecast

[3]

[3]

Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.