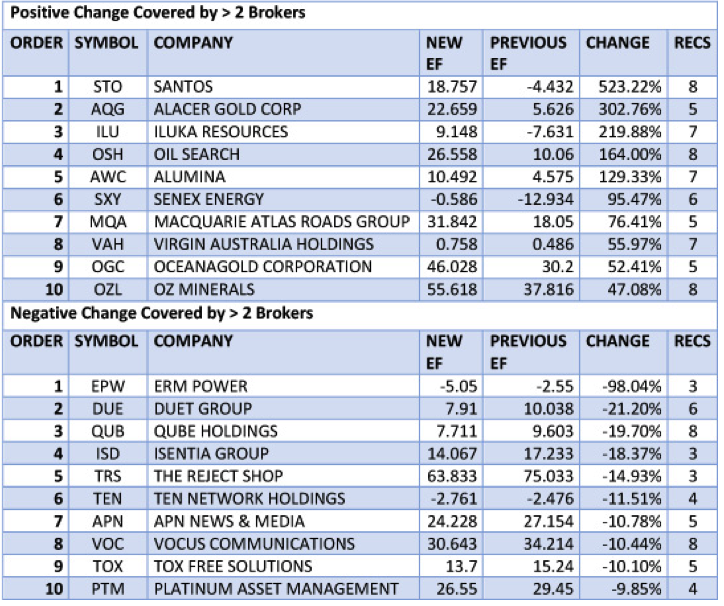

The chart below shows the buy recommendations of brokers. Companies are only displayed in this table if at least 5 of the above mentioned brokers have a current position on the stock. A broker sentiment value of +1 means all brokers have a buy recommendation. The target price upside/downside is relative to the price at the time the table was updated.

The stocks with the largest target price upside this week are Domino’s Pizza Enterprises with 30.01% and APN News and Media with 27.65%.

[table “260” not found /]

In the good books

3P LEARNING LIMITED (3PL) Upgrade to Outperform from Neutral by Macquarie B/H/S: 2/0/0

3P’s first half result was ahead of the broker’s expectations. No specific guidance was provided, but the company reiterated it is on track to deliver a $2m annualised cost saving relative to the second half of FY16, and expects to deliver revenue growth ahead of cost growth.

Macquarie has raised FY17 earnings forecast by 3.8%, reflecting the improved operational outlook.

The broker upgrades the stock to Outperform from Neutral and raises the target price to $1.25 from $1.00.

[1]

[1]ASALEO CARE LIMITED (AHY) Upgrade to Outperform from Neutral by Credit Suisse B/H/S: 2/1/0

2016 results were ahead of forecasts. Credit Suisse notes some of the growth was in channels that are not readily observed such as 14% growth in the Pacific islands and high single digit growth in Australian industry tissue.

Credit Suisse upgrades 2017 estimates by 10%. Rating is upgraded to Outperform from Neutral. Target is raised to $1.75 from $1.50.

ALTIUM LIMITED (ALU) Upgrade to Outperform from Neutral by Credit Suisse B/H/S: 2/1/0

First half results were ahead of expectations and the company has reiterated its target for long-term revenue of US$200m by FY20. Credit Suisse believes targets are within reach.

The broker acknowledges the stock is not cheap but believes this should be viewed in the context of over 20% growth in earnings per share, and multiple avenues for further incremental growth. Rating is upgraded to Outperform from Neutral. Target is raised to $9.50 from $9.00.

APA GROUP (APA) Upgrade to Buy from Accumulate by Ord Minnett B/H/S: 2/2/3

First half operating earnings beat forecasts. Ord Minnett remains positive on the stock, believing the regulatory headwinds that have affected it in the past are now behind.

The broker upgrades to Buy from Accumulate Target is raised to $10.90 from $10.30.

APN NEWS & MEDIA LIMITED (APN) Upgrade to Buy from Neutral by UBS B/H/S: 5/0/0

APN’s result beat UBS, with a weaker performance from radio offset by a strong performance from Adshel. The dividend was reinstated for the first time since 2012.

UBS expects Adshel to be the main earnings driver in the second half. Factoring in higher contributions from Adshel, and a better net debt balance, the broker’s valuation now suggests an upgrade to Buy, despite tax and re-contracting risk. Target rises to $3.30 from $3.00.

APN OUTDOOR GROUP LIMITED (APO) Upgrade to Add from Hold by Morgans B/H/S: 4/1/0

The company’s 2016 results were in line with the broker’s estimates. Digital screens grew by 31 in the second half, providing strong revenue uplift potential.

Regardless of the outcome of the ACCC ruling on the proposed merger with oOh! media (OML), the broker still considers the stock looks cheap relative to its growth profile.

Morgans upgrades to Add from Hold and the target price rises to $6.37 from $5.66.

CLEANAWAY WASTE MANAGEMENT LIMITED (CWY) Upgrade to Add from Hold by Morgans B/H/S: 2/3/0

First half EBITDA beat forecasts. Morgans notes the turnaround continues, with growth in revenue combined with cost control.

The broker expects bolt-on acquisitions to be an ongoing theme for the company.

Target lifts to $1.22 from $1.19 and the rating is upgraded to Add from Hold, given the total potential return of 10%.

See also CWY downgrade.

FLIGHT CENTRE LIMITED (FLT) Upgrade to Outperform from Neutral by Credit Suisse B/H/S: 2/4/2

Credit Suisse attributes most of the deterioration in first half profit to cyclically low air fare prices and finds enough justification to move to an Outperform rating from Neutral.

While a slow structural decline in share is expected to continue the broker believes the company is likely to witness a positive impact on revenue and profit from a cyclical recovery in air fares in FY18. Target is reduced to $34.90 from $36.49.

HUON AQUACULTURE GROUP LIMITED (HUO) Upgrade to Accumulate from Hold by Ord Minnett B/H/S: 2/0/0

Huon’s earnings result beat Ord Minnett by 22% on higher salmon prices and lower than expected costs. Management described conditions as near perfect. The broker materially upgrades forecasts on production cost guidance.

While assuming a decline ahead in wholesale prices, the broker upgrades to Accumulate from Hold noting price upside risk. Target rises to $5.31 from $4.17.

INSURANCE AUSTRALIA GROUP LIMITED (IAG) Upgrade to Neutral from Underperform by Credit Suisse B/H/S: 0/7/1

First half net profit was ahead of forecasts. Credit Suisse upgrades to Neutral from Underperform following the underperformance of the share price and an expectation that reserve releases will continue in the near term.

The broker suspects original FY17 guidance was too optimistic and the softer underlying margin in the first half is more in line with expectations. The deterioration in the underlying margin is expected to slow or even turn around from the first half level. Target is raised to $6.05 from $5.75.

See also IAG downgrade.

IRESS MARKET TECHNOLOGY LIMITED (IRE) Upgrade to Accumulate from Hold by Ord Minnett B/H/S: 3/1/0

Iress’ result missed Ord Minnett and consensus at the headline, and the broker expects earnings downgrades will follow, but underlying organic trends in the second half were a positive, the broker suggests. The Canadian and UK businesses appear to have bottomed.

Given conservative accounting compared to other IT stocks and very strong cash flow conversion, the broker is more confident now in medium term growth. Upgrade to Accumulate from Hold. Target rises to $12.50 from $11.00

MCMILLAN SHAKESPEARE LIMITED (MMS) Upgrade to Outperform from Neutral by Macquarie and Upgrade to Buy from Neutral by Citi B/H/S: 3/0/1

First half results were just below the broker’s expectations. No FY17 guidance was forthcoming, other than management’s statement that early performance on the QLD contract was solid.

Macquarie has raised FY17 and FY18 earnings estimates by 0.2% and 0.6% respectively.

The broker has upgraded the stock to Outperform from Neutral and raised the target price to $13.20 from $13.17.

Upgrade to Buy as Citi analysts have become a lot more comfortable with the risks surrounding the QLD government contract, while momentum is seen building.

The analysts see clearly defined organic growth opportunities with Government clients while valuation is still at a considerable discount vis-a-vis other small industrials.

Despite small reductions in core profit estimates, target price jumps by 19% to $14.33 as the 15% risk discount (QLD contract) is removed.

MYOB LIMITED (MYO) Upgrade to Neutral from Underperform by Credit Suisse B/H/S: 3/3/0

2016 results were in line with expectations. The company has guided to double digit revenue growth in 2017. Paycorp, with which MYOB already collaborates, will be acquired for $48m.

Credit Suisse rolls forward valuation and upgrades to Neutral from Underperform. Target is raised to $3.50 from $3.20. The broker continues to envisage downside risk to the company’s market position from intense competition in the SME accounting software space.

NIB HOLDINGS LIMITED (NHF) Upgrade to Neutral from Underperform by Credit Suisse B/H/S: 2/5/0

Nib’s profit result beat Credit Suisse by 22% driven by record net margins. The broker considers upgraded FY guidance to be conservative.

The broker’s prior negative stance was premised on the government addressing the exorbitant profits being made by insurers at the expense of policyholders. This result, and Nib’s increased premiums, suggest this is not going to happen anytime soon. Upgrade to Neutral. Target rises to $5.50 from $4.55.

PLATINUM ASSET MANAGEMENT LIMITED (PTM) Upgrade to Hold from Sell by Ord Minnett B/H/S: 0/2/2

The company’s strong first half result surprised the broker, with both management fee margins and costs beating forecasts.

Ord Minnett believes the balance sheet is well positioned, with net cash of $365m, and while the company has a buy-back program it has so far not bought back a single share despite the price having dipped below $4.80.

As a result, the broker has removed the buy-back from its estimates, preferring instead to see Platinum returning cash to shareholders via higher dividends.

Upgrade to Hold from Sell and target rises to $4.93 from $4.69.

SMARTGROUP CORPORATION LTD (SIQ) Upgrade to Neutral from Sell by Citi B/H/S: 3/2/0

Citi analysts saw the company reporting a strong result, but they remain of the view that future growth will be a challenge, including via acquisitions. The interim report did surprise and thus estimates have gone up by double-digits.

Stronger organic growth pushes up the target price by 13% to $6.61. Upgrade to Neutral from Sell. Catalysts to watch out for include the outcomes from the WA Salary Packaging panel, new client wins and client churn rates post acquisitions, point out the analysts.

SOMNOMED LIMITED (SOM) Upgrade to Add from Hold by Morgans B/H/S: 1/0/0

Morgans found the underlying first half results positive. FY17 guidance is reiterated. A further 10 centres will be rolled out by the end of FY18.

Rating is upgraded to Add from Hold. The target price falls to $4.05 from $4.11. The main risk on the downside the broker envisages is slower-than-expected growth in the key markets of North America and Europe.

TASSAL GROUP LIMITED (TGR) Upgrade to Outperform from Neutral by Credit Suisse B/H/S: 3/1/0

First half margins were better than Credit Suisse expected and, given the first half is likely to represent the toughest point in terms of operating conditions, earnings are expected to improve.

The broker expects the market to focus on increasing momentum and FY18 growth. Rating is upgraded to Outperform from Neutral. Target is raised to $5.20 from $4.50.

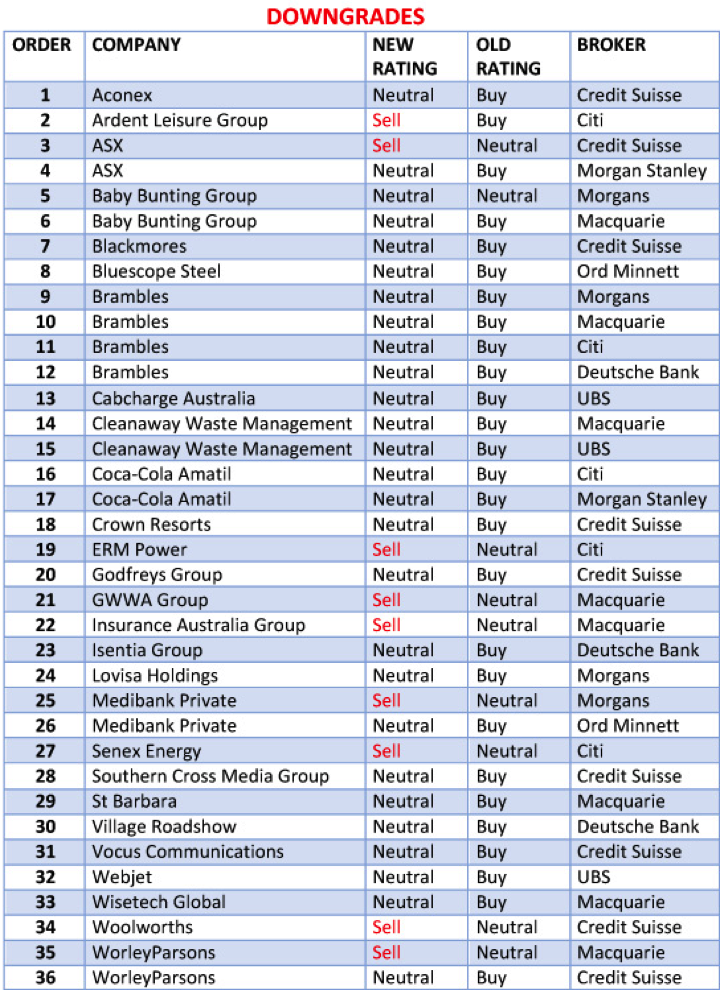

In the not-so-good books

ARDENT LEISURE GROUP (AAD) Downgrade to Sell from Buy by Citi B/H/S: 1/5/1

The deterioration in like-for-like sales at Main Event has Citi analysts worried. As the analysts have come to the conclusion the situation is unlikely to improve short term, they downgrade to Sell from Buy (that’s a double notch downgrade).

The deterioration in momentum is especially concerning, point out the analysts, given Main Event is cycling an undemanding 3Q16 growth comparison. Clearly, the initiatives announced at FY16 results have not successfully improved sales. Is competition starting to impact?

Earnings estimates have been culled by -17% to -29% for FY17-FY19. Target Price crashes by -42% to $1.55.

[2]

[2]BLACKMORES LIMITED (BKL) Downgrade to Neutral from Outperform by Credit Suisse B/H/S: 1/2/0

First half underlying EBITDA missed expectations. While Credit Suisse believes the worst is behind the company the road ahead is not smooth.

March/June quarter revenue could be flat sequentially, with weaker seasonality in China, while cost savings continue to be re-invested in price.

The company appears to the broker to be behind competitors in building up its China presence. Rating is downgraded to Neutral from Outperform. Target is reduced to $110 from $125.

COCA-COLA AMATIL LIMITED (CCL) Downgrade to Neutral from Buy by Citi and Downgrade to Equal-weight from Overweight by Morgan Stanley B/H/S: 0/7/0

2016 results signal to Citi the company remains on message. Cost savings drove earnings and more is expected in Australia.

The broker upgrades forecasts for earnings per share by less than 2% and expects growth of 7% in 2017, helped by the share buy-back.

Citi downgrades to Neutral from Buy, given the rise in the share price and caution surrounding the upcoming container deposit scheme in NSW. Target is raised to $11.00 from $10.80.

2016 results revealed strong cash generation and the buy-back surprised Morgan Stanley although it shows the company is going well. The broker continues to like the stock and envisages little earnings risk.

Now the risk/reward is more balanced the rating is downgraded to Equal-weight from Overweight. Target is $10.50. In-Line sector view.

CROWN RESORTS LIMITED (CWN) Downgrade to Neutral from Outperform by Credit Suisse B/H/S: 3/2/1

First half results were in line. Credit Suisse expects Crown to fully exit the MPEL and Las Vegas joint ventures and return further capital to shareholders. Once paid out the broker suggests the stock should return to an appropriate trading multiple of 9 times FY19 EBITDA, or $10.50.

The broker upgrades FY17 EBITDA 6-9% to incorporate the company’s signals on cost reductions and the target is raised to $13.00 from $12.50. Rating is downgraded to Neutral from Outperform, given the rally in the share price.

CLEANAWAY WASTE MANAGEMENT LIMITED (CWY) Downgrade to Neutral from Buy by UBS and Downgrade to Neutral from Outperform by Macquarie B/H/S: 2/3/0

An in-line result from Cleanaway implies a significant improvement in core operations, UBS suggests. Unchanged FY guidance also meets expectation.

Management is now free to pursue operational improvements and cost-outs, the broker suggests, and a modestly better looking macro-economic backdrop may signal the start of a multi-year upgrade cycle. But given the stock is trading in line with international peers, UBS sees limited share price upside.

Downgrade to Neutral. Target rises to $1.16 from $1.15.

Cleanaway’s first half results were in line with the broker’s expectations. FY17 guidance is for little change in economic conditions but for both divisions to grow earnings.

Collections are expected to increase earnings as recent cost, volume and pricing initiatives take effect. Industrials are also expected to increase earnings, largely due to cost out.

Macquarie has cut FY17 EPS forecast by -3.5% and FY18 EPS forecast by -3.7%. The broker downgrades the stock to Neutral from Outperform and $1.14 target retained.

See also CWY upgrade.

ERM POWER LIMITED (EPW) Downgrade to Sell from Neutral by Citi B/H/S: 0/0/3

US margins disappointed and this means the financial result overall missed expectations, even before adjusting for the -$2.9m loss moved into discontinued operations, comment the analysts.

Citi analysts acknowledge the operational leverage to any future improvements is huge, but they’ve nevertheless decided to downgrade to Sell from Neutral. Target price dives by -20% to $1.05.

Earnings estimates have received a double-digit haircut for the years ahead. Citi doesn’t think the market is accurately pricing in this prospect.

GODFREYS GROUP LIMITED (GFY) Downgrade to Neutral from Outperform by Credit Suisse B/H/S: 0/1/0

First half results disappointed Credit Suisse, although marginally ahead of subdued expectations. Until the company can demonstrate a sustainable return to positive like-for-like growth the broker does not envisage a material re-rating emerging.

While more favourable FX should benefit margins the broker remains cautious and downgrades to Neutral from Outperform. Target is reduced to 95c from $1.35.

INSURANCE AUSTRALIA GROUP LIMITED (IAG) Downgrade to Underperform from Neutral by Macquarie B/H/S: 0/7/1

IAG’s first half results were better than Macquarie’s forecasts. FY17 outlook is for better premium growth, largely driven by claims inflation, offset by softer margins.

The broker has cut FY17 earnings forecasts by -0.9%, FY18 by -7.7% and FY19 by -3.3%.

Macquarie downgraded the stock to Underperform from Neutral and price target drops to $5.70 from $5.80.

See also IAG upgrade.

ISENTIA GROUP LIMITED (ISD) Downgrade to Hold from Buy by Deutsche Bank B/H/S: 1/2/0

First half results missed expectations. Margins declined to 25.4%, reflecting losses in King Content and higher publishing costs in the core business.

Deutsche Bank observes the core Australasian business has reached a limit in its ability to harvest returns through price increases. King Content disappointed the broker, reinforcing concerns around the quality of the business and execution.

Recent trends suggest to the broker that a turnaround will be difficult, increasing the likelihood of further disappointment. Rating is downgraded to Hold from Buy. Target is reduced to $2.10 from $2.90.

LOVISA HOLDINGS LIMITED (LOV) Downgrade to Hold from Add by Morgans B/H/S: 1/2/0

First half results were ahead of forecasts and Morgans found little to fault. Management continues to expect gross margin trends will moderate in the second half as the exit of a competitor is cycled.

The half year was a strong period for execution and Morgans downgrades to Hold from Add. Target is raised to $4.37 from $4.30.

ST BARBARA LIMITED (SBM) Downgrade to Neutral from Outperform by Macquarie B/H/S: 2/1/0

St Barbara’s first half results were in line with the broker’s expectations. The company retired $172m of debt and moved to a net cash position. The final US$20m of senior notes will be retired this quarter, leaving the company debt free.

Macquarie has raised FY17 earnings forecast by 7% while cutting longer term forecasts by 7% to 8%.

The broker downgrades the stock to Neutral from Outperform and target rises to $3.00 from $2.90.

SOUTHERN CROSS MEDIA GROUP (SXL) Downgrade to Neutral from Outperform by Credit Suisse B/H/S: 0/4/1

First half results were in line with expectations but the full-year outlook is disappointing for Credit Suisse. Regional TV ad revenue grew 29% in the first half, below the 30-35% flagged for the full year back in August.

Credit Suisse believes corporate activity is a potential catalyst. With lower earning forecasts, the rating is downgraded to Neutral from Outperform on valuation grounds. Target is reduced to $1.40 from $1.50.

VOCUS COMMUNICATIONS LIMITED (VOC) Downgrade to Neutral from Outperform by Credit Suisse B/H/S: 5/3/0

First half results were in line with forecasts. Credit Suisse notes cash conversion was weak although the company is mindful of this and intent on making improvements.

The broker retains FY17 EBITDA forecasts at the lower end of the $430-450m range. Rating is downgraded to Neutral from Outperform and the target to $5.00 from $5.70.

WEBJET LIMITED (WEB) Downgrade to Neutral from Buy by UBS B/H/S: 2/3/0

Webjet’s result beat UBS forecasts across all divisions. FY guidance has been increased and the balance sheet is in good shape.

Messy cash flows and working capital adjustments nevertheless reduced the quality of the beat, the broker suggests. UBS believes there’s still plenty of momentum in the business but this is priced in, to the point of near perfection. Forecasts increased but rating pulled back to Neutral. Target rises to $11.50 from $10.72.

WOOLWORTHS LIMITED (WOW) Downgrade to Underperform from Neutral by Credit Suisse B/H/S: 3/1/3

First half earnings were broadly in line with forecasts. Credit Suisse increases forecast food EBIT on the back of improvements in key operating metrics and envisages trend total sales growth at 3-4% as realistic.

The balance sheet was helped by a significant slowing in property investment, payments for the divestment of home improvement assets and property disposals.

Credit Suisse downgrades to Underperform from Neutral. Competitive risks are not abating and the stock appears a little expensive to the broker. Target is raised to $24.50 from $24.30.

WISETECH GLOBAL LIMITED (WTC) Downgrade to Neutral from Outperform by Macquarie B/H/S: 2/2/0

Wisetech Global’s first half result was better than the broker had expected. Macquarie believes the company is well on track to meet the reaffirmed FY17 guidance.

The broker has raised FY17 forecasts by 15% and FY18 forecasts by 12%. Macquarie downgrades the stock to Neutral from Outperform and target is raised to $5.80 from $5.30.

Earnings forecast

[3]

[3]Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regards to your circumstances.