For the week ending Friday, 5 October 2018, FNArena registered an evenly balanced seven upgrades and seven downgrades for individual ASX-listed stocks. Carsales was the only recipient of more than one recommendation change with two upgrades, both to Buy.

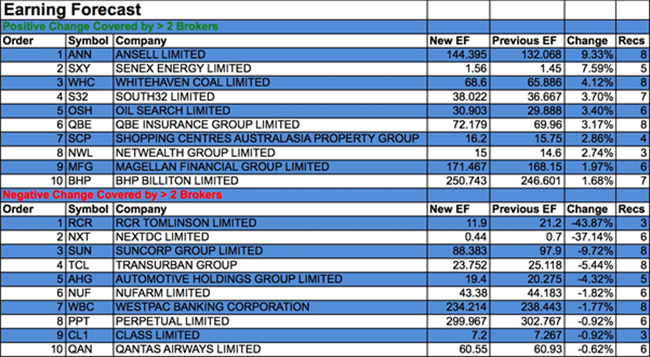

The week’s table for positive revisions to earnings estimates shows some meaty adjustments, with Ansell on top of the ranking (+9%), followed by Senex Energy, Whitehaven Coal, South32, Oil Search and QBE Insurance. Negative revisions contain a number of hefty cuts, with RCR Tomlinson the week’s biggest loser, followed by NextDC, Suncorp, Transurban and Automotive Holdings.

In the good books

BANK OF QUEENSLAND LIMITED (BOQ) was upgraded to Hold from Lighten by Ord Minnett. B/H/S: 3/2/3. FY18 results were stronger than Ord Minnett expected, driven by one-offs. The broker found some evidence the bank is becoming better at gathering deposits but the forecast return-on-equity profile remains anaemic. Ord Minnett upgrades to Hold from Lighten and raises the target to $10.60 from $10.30.

[1]

[1]CARSALES.COM LIMITED (CAR) was upgraded to Outperform from Neutral by Credit Suisse and to Buy from Sell by Citi. B/H/S: 4/3/0. Credit Suisse expects higher pricing and penetration of depth products to drive revenue growth in FY19. Associated yield improvements should contribute to a forecast 7.5% increase in core private revenue and an 8.5% increase in dealer segment revenue over FY19. Target is raised to $16 from $15. Further in-depth research has now convinced Citi analysts Carsales will enjoy acceleration in car dealer depth penetration, combined with continued volume growth. Price target lifts 19% to $16.65. Earnings estimates have been upgraded, with Citi’s forecasts now anticipating 3-year EPS CAGR of 12%.

MAGELLAN FINANCIAL GROUP LIMITED (MFG) was upgraded to Outperform from Neutral by Credit Suisse. B/H/S: 4/1/1. Credit Suisse upgrades earnings estimates because of a strong fund performance as the company benefits from performance fees. Credit Suisse estimates that, if fund performance is maintained until December, performance fees in the first half should be over $30 million. Forecasts are upgraded by 9% for FY19 and 6% for FY20 and the rating is upgraded to Outperform from Neutral. Target is raised to $31 from $29.

SHOPPING CENTRES AUSTRALASIA PROPERTY GROUP (SCP) was upgraded to Accumulate from Hold by Ord Minnett. B/H/S: 1/2/1. The company has acquired a 10-asset portfolio of regional shopping centres from Vicinity Centres. The $573 million acquisition reflects a 7.1% capitalisation rate and a 7.25% passing yield. Ord Minnett envisages the company has more stable shopper patterns, superior sales growth and more predictable income growth versus the majority of its peers. Target is raised to $2.70 from $2.52.

SEEK LIMITED (SEK) was upgraded to Neutral from Underperform by Credit Suisse. B/H/S: 2/3/2. Credit Suisse considers a slowdown in volume growth in domestic job advertisements at the beginning of FY19 is primarily driven by tough comparables, as domestic labour market fundamentals remain robust. Mid single digit volume growth is expected for the Australasian employment business in the remainder of the financial year. The broker upgrades to Neutral, from Underperform, as the stock is trading close to the new target, raised to $19.10 from $17.50.

In the not-so-good books

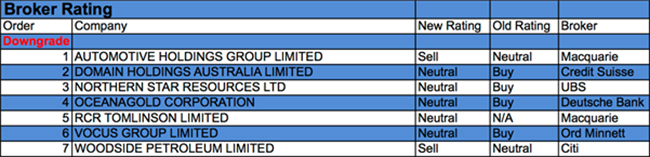

AUTOMOTIVE HOLDINGS GROUP LIMITED (AHG) was downgraded to Underperform from Neutral by Macquarie. B/H/S: 1/3/1. Australian new vehicle sales fell 4.9% in the September quarter and the numbers have been negative in all of the last six months, Macquarie reports. SUVs were the only bright spot, rising 4.2% in the quarter, but the broker notes a 10.6% decline in private sector demand is of most concern. Macquarie believes challenging conditions suggest downside risk to consensus earnings forecasts for Auto Group Holdings and lowers its own forecasts and its target to $2.00 from $2.50.

[2]

[2]DOMAIN HOLDINGS AUSTRALIA LIMITED (DHG) was downgraded to Neutral from Outperform by Credit Suisse. B/H/S: 2/2/2. Credit Suisse considers the decline in new listing volumes at the start of FY19 a headwind for the business but entirely consistent with expectations. Analysis suggests 2018 volumes are at the low point of the range seen over the last five years and therefore downside risk is limited beyond 2018. As the stock is now trading close to the target the rating is downgraded to Neutral from Outperform. Target is $3.50.

NORTHERN STAR RESOURCES LTD (NST) was downgraded to Neutral from Buy by UBS. B/H/S: 3/1/2. UBS continues to believe Northern Star has the potential to beat production guidance in FY19. However, the share price is now factoring in most of the exploration success and the ability to revitalise the recently-acquired Pogo asset. Target is raised to $9 from $8.

RCR TOMLINSON LIMITED (RCR) was downgraded to Neutral from Outperform by Macquarie. B/H/S: 0/2/0. Macquarie is back from restriction, having advised on RCR’s capital raising, which it notes, in the wake of issues at the Daydream and Hayman solar farms, strengthens the balance sheet to allow ongoing delivery on engineering, construction and maintenance. It will take time to stabilise the business and deliver sustainable profit growth. Sector consolidation should provide valuation support but for the meantime Macquarie pulls back to Neutral from Outperform. Target is $1.20.

VOCUS GROUP LIMITED (VOC) was downgraded to Hold from Accumulate by Ord Minnett. B/H/S: 1/4/1. Ord Minnett expects it will take some time for the company’s new management to settle in and implement strategies. Potential upside exists in three areas, which could lead the broker to increase earnings forecasts. These include the $90 million transformation target, the full selling through of Australia-Singapore cable capacity and accelerated market share gains in enterprise and consumer segments. As the stock is now trading in line with the target of $3.30 the rating is downgraded to Hold from Accumulate and the broker awaits signs of improved execution.

Earnings forecast

Listed below are the companies that have had their forecast current year earnings raised or lowered by the brokers last week. The qualification is that the stock must be covered by at least two brokers. The table shows the previous forecast on an earnings per share basis, the new forecast, and the percentage change.

[3]

[3]Important: This content has been prepared without taking account of the objectives, financial situation or needs of any particular individual. It does not constitute formal advice. Consider the appropriateness of the information in regard to your circumstances.